As you all know, the crisis hit the region in stages. First, there were the spillovers from the financial stress in countries at the epicenter of the crisis. International bank flows to Asia turned negative as a result of sudden deleveraging among major banks.

External bond issuance came to a halt.

Equity markets and local currencies—with the exception of the yen—recorded large losses as capital flowed out.

And, shortages in dollar funding briefly spilled over into domestic money markets. The reversal of private flows was followed by a collapse in exports, which contracted by around 30 percent in many Asian countries, and more than 40 percent in Japan. Finally, the external shock fed through to domestic demand with sharp contractions in investment and, in some instances, consumption.

The rebound in Asian economic activity has again taken many observers by surprise. Indeed, Asia is leading the global recovery. Industrial production in export-dependent Asia has regained most of the ground lost since September 2008, even returning to pre-crisis levels in a few countries, including Korea..

This rebound seems to have been driven by an equally sharp rebound in export volumes.

Domestic demand has also been playing a part in Asia’s rebound.

Meanwhile, global financial conditions have eased, providing a further boost to Asia’s recovery: Corporate credit spreads have narrowed, net equity inflows have picked up.

II. Lessons for financial regulation and supervision

Let me now turn to the first of my three policy questions: what has the crisis taught us about financial regulation and supervision. There has been multitude of lessons learned, but I will focus here on those most relevant for East Asia.

The crisis has laid bare major shortcomings in regulatory frameworks for bank capital. In response to this, the Basel Committee and the G20 at their Pittsburg summit have now agreed on a set of corrective actions.

- First, common shares and retained earnings are likely to become the predominant form of tier 1 capital. This could have implications in particular for Japanese banks who hold much of their tier 1 capital in the form of hybrid bonds and preferred shares.

- Second, the capital adequacy ratio which is based on risk weighted assets will be complemented by a leverage ratio which is likely to be based on simple assets. This could again have implications for Japanese and Indian banks which hold large amounts of government paper. Government paper has a zero risk weight under Basel II, but would enter the leverage ratio at face value.

- Third, counter-cyclical capital buffers will be introduced above minimum capital requirements. This so-called macro-prudential regulation would oblige banks to build up capital buffers based on a set of variables that vary over the business cycle, such as credit growth or bank earnings.

The crisis has also revealed shortcomings in the regulation and supervision of liquidity management. In response to this, the Basel Committee and the G20 plan to introduce a longer-term structural liquidity ratio. As you know, the excessive reliance on wholesale funding has also been an issue in some Asian countries, particularly in Korea, Australia, and New Zealand. And, New Zealand has already introduced a core funding rule that reduces banks’ reliance on short-term financing.

The crisis has starkly illuminated the interconnectedness of financial stability and lender-of-last-resort facilities, which in many countries are handled by different agencies. In some countries, it has reignited the debate over whether the central bank should be in charge of financial supervision and regulation. How can the central bank be expected to provide exceptional financing during a crisis if it is not in charge of crisis prevention? And, how will it obtain the required information to fulfill its lender-of-last-resort function? These arguments can not be easily dismissed. In fact, in some countries, including Korea, they have led to the setting up of more formal frameworks to facilitate policy coordination and information exchange between the government, the regulator, and the central bank. However, there are also strong arguments against a financial stability mandate for the central bank. Most importantly, it could jeopardize central bank independence and undermine the credibility of the inflation targeting regime.

This brings me to my next point. The crisis has also led to a reassessment of the connection between financial stability and monetary policy. Most believe that lax monetary policy had a role, if not the predominant one, in creating the current credit bubble. And, few believe any longer that it is easier to clean up after a bubble has burst. So, should central banks be in the business of preventing the formation of asset bubbles? Again, putting central banks explicitly in charge of financial stability or, more directly, asset price stability may lead to confusion about commitment to inflation fighting. Also, monetary policy is a rather blunt tool and the first line of defense should always be prudential regulation. That said, prudential regulation may not always prove effective in containing asset bubbles and central banks may need to be more willing than in the past to use traditional monetary policy tools to lean against unsustainable increases in credit and indebtedness.

Another cause for the crisis has been an insufficient regulatory perimeter. In particular, banks’ leverage turned out to be much larger than assumed given their exposure to off-balance sheet entities, which had proliferated beyond the watch of financial regulators. This holds important lessons for Korea. The country has embarked on a wide-ranging deregulation of its financial sector with the enactment of the Financial Investment Services & Capital Markets Act this February. The act removes restrictions that separated financial service providers and introduces a negative list for new financial products. In principle, this is a welcome development that should foster greater access to financial intermediation, particularly for new and dynamic sectors of the economy. However, this has to go hand in hand with the ability of supervisors to ensure that regulatory arbitrage does not emerge. In this context, regulatory and supervisory capacity needs to keep pace with market growth and rapid innovation.

III. Sustainability of the current upswing and exit policies

I turn now to my second question, which deals with the sustainability of the Asian rebound and its implications for exit policies.

A. Sustainability of the current upswing

Many, including the Fund, had predicted that an Asian recovery could not precede a recovery in Europe and the U.S. Have these pundits and forecasters been proven wrong by the striking rebound in Asian economic activity? To be sure, the strength of activity has taken many observers by surprise. But, as I will argue in what follows, the current recovery is unlikely to maintain the momentum of recent months and growth may not return to pre-crisis levels so soon. This has important implications for the design and implementation of exit strategies.

The current rebound is to a considerable extent driven by a restocking of global inventories. At the peak of the current crisis, production fell more than final demand, partly because of the disruptions in trade and other financing. As a result, inventories reached historical lows in many parts of the world. Some of the economic activity we are seeing today is the rebuilding of stocks and, therefore, not sustainable. Put differently, production is partly making up for its earlier undershooting, but will remain weak over the medium-term, unless final demand recovers.

Asia’s economies are also being supported by large fiscal stimulus measures, both abroad and in the region. In fact, Asia’s fiscal response has been larger than in the average G20 country. Exports and industrial production have benefited from car scrapping schemes and fiscal stimulus packages abroad. However, car scrapping schemes have only brought forward sales and may in fact lead to lower than normal sales in 2010. Fiscal stimulus can not go on for long in the major advanced economies where debt levels are projected to rise to 115 percent of GDP by 2014.

Steep exchange rate devaluations have also supported the recovery in some countries, but are not likely to last. Korea is a case in point: strong exports reflect partly a gain in market share rather than an increase in global demand. With the return of the exchange rate nearer to its medium-term equilibrium level, net exports are likely to contribute much less to growth.

Asia remains very dependent on demand from U.S. consumers. While it is undeniable that intra-regional trade has risen markedly over recent years, this largely reflects a reorganization of the production chain. China has become the assembly hub, but western countries remain the final destination. Using input-output tables, we find that Asia’s dependence on demand from outside the region has not changed markedly since the 1990s, and has even increased in a few instances. That said, the dependence of Korea and Taiwan POC on final demand from China has increased steeply and now rivals their exposure to the U.S.

Demand in advanced economies remains important but is projected to remain weak for some time. Advanced economies are growing below potential, implying a rise in unemployment well into 2010. This bodes ill for a sharp rebound in consumer demand. In addition, Western consumers need to repair overextended balance sheets. Even if demand in advanced economies bounced back quickly, potential growth could be lower for some time, given major dislocations in financial systems.

To summarize our outlook, the IMF currently projects world output to contract by 1.1 percent in 2009 and grow by just over three percent in 2010. That is a far cry from the 5 percent growth recorded in 2007. Asia is projected to grow by 5¾ percent in 2010, with China recording 9 percent, India 6.4 percent, Korea 3.6 percent, and Japan 1.7 percent.

B. Exit policies

This brings me to exit policies.

Timing exit policies correctly is challenging, because it is difficult to tell a policy-driven rebound from a genuine turning point in economic activity where the private sector is back to a self-sustaining expansion. In the Fund’s view, the risk of premature exit from monetary easing far outweighs the risk of sustained monetary accommodation. With output gaps projected to remain large and negative, the risk of inflation is negligible. Asset prices do not seem out of line with fundamentals and can as a first line of defense be contained through prudential regulation as done, for example in China and Korea. Letting exchange rates appreciate would also help contain asset bubbles.

It also seems too early to exit from accommodative fiscal policies. In Asia there is substantial scope for fiscal stimulus in many countries, in contrast to many advanced economies outside the region. Also, postponing the fiscal adjustment to a time when the recovery has firmly taken hold does not mean inaction. Governments can signal commitment to fiscal sustainability without necessarily undermining demand—for example, by announcing medium-term fiscal consolidation plans and by reforming pension entitlements.

International coordination of exit strategies will be key to a successful exit process. The synchronicity of the crisis facilitated coordination in the introduction of unprecedented policy measures. However, the recovery may be less synchronized. In particular, the leakage from fiscal policies could lead to free-rider problems and sub-optimal provision. But, also spillovers from monetary policies require careful coordination at the international level.

To ensure consistency of national policies, G20 leaders have agreed in Pittsburg on a process of mutual assessment. As part of this process the IMF is asked to report regularly to the G20 on global economic developments, patterns on growth, and suggested policy adjustments, building on its existing bilateral and multilateral surveillance analysis.

IV. Medium-term sources of growth and reserve accumulation:

Turning to my third question, let me now share some thoughts on East Asia’s sources of growth over the medium term. Closely related is the question of reserve accumulation, which I will also touch upon.

A. Medium-term sources of growth

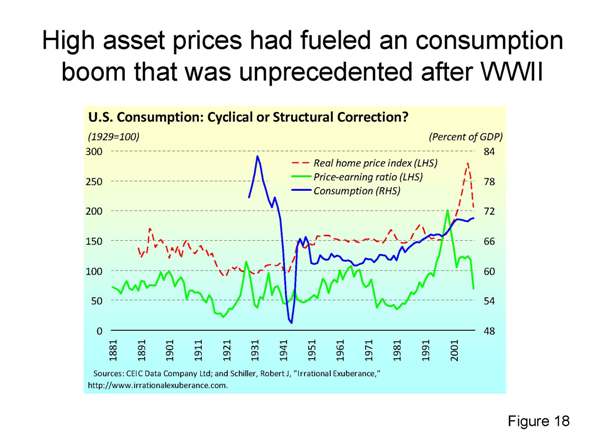

Over the past years, global and Asian growth has been powered by U.S. consumers. These had reduced their savings rates in a dramatic fashion since high house and stock prices made them consume more against the nominal value of their assets. With the burst of the housing bubble, Western consumers need to repair their balance sheets. In fact, they have already started doing this: the U.S. ratio of household saving to disposable income has increased to over 5 percent, from close to zero in 2007. Even if financial wealth returned to pre-crises levels—which seems unlikely in the near future—U.S. consumers would still probably save more. The reason is that the crisis has made them more conscious of vulnerabilities of their balance sheets.

Who then will replace the U.S. consumer going forward? Asia—and other emerging market—have so far relied successfully on an export-led growth strategy. However, this strategy may be less successful in the years to come. It is simply not possible for all economies to boost their current account balances at the same time. Hence, Asia may have to rely more on domestic sources of growth.

In China, there is scope to raise domestic demand. Better social insurance and improved access to credit would reduce precautionary saving and boost household consumption. And, addressing governance issues at state-owned firms would lead them to retain less earnings. Letting the exchange rate appreciate would also help by shifting economic activity from the capital intensive export sector to the labor intensive nontradables sector. This, in turn, would raise the labor share of income and the contribution of consumption to GDP.

Other economies in Asia, notable Korea and Japan, have less room to increase demand. In fact, Korea’s household savings rate is already quite low. And, both countries face large demographic pressures, which are likely to reduce saving. However, in these countries the nontradables sector—neglected for decades in the context of export-led growth strategies—could become a significant source of growth. Several ingredients are key to this effort:

- First, leveling the playing field between the tradables and nontradables sector. In Korea, for example, there are various tax incentives that benefit the manufacturing sector, but not the services sector.

- Second, opening up the service sector to competition, including from abroad. Korea has taken some important steps in this direction, but the health and education sector remain largely closed to foreign competition.

- Third, boosting the productivity of small and medium-size enterprises—or so-called SMEs—which account for the lion share of service sector output. Most observers believe that this requires a curtailment of SME credit guarantee schemes. These schemes were expanded in response to the crisis, particularly in Japan and Korea, and could be rolled back as economic conditions improve.

B. Reserve Accumulation

Another problem related to rebalancing of global growth is reserve accumulation (which usually requires current account surpluses). To be sure, official reserves played a crucial role during the current crisis. And, many observers, I am sure, will take away from this crisis the lesson that countries should accumulate even more reserves. This conclusion can be questioned for a number of reasons.

Rather, I see various ways to reduce the need for self-insurance. At the country level, sound economic policies clearly can reduce the need for insurance over time as policy credibility is enhanced and confidence in currencies is strengthened. At the regional level, bilateral and multilateral swap arrangements can diversify risks and the extension of the Chiang Mai reserve pool is a welcome development in this respect. The largest degree of risk diversification could be achieved at the global level.

Indeed, in recognition of the need to strengthen systemic insurance mechanisms, G-20 leaders, at its April Summit, called for a near tripling of the IMF’s lending resources to $750 billion, with Asian countries being among the main contributors so far. Also, over the past year a number of steps have been taken to reform and expand the Fund’s lending facilities. However, the Fund’s resource base (or insurance pool) could be increased further. Even after its recent tripling, it is still smaller as a share of global GDP—and even smaller as a share of global capital flows—than it was when the Fund was created.

In addition, a top priority for the Fund’s legitimacy and effectiveness is an increase in the quota and voice of underrepresented emerging market economies. Reforms agreed in April 2008 need to be approved promptly. But, this is a just a first step in ongoing reforms. The G-20 has called for completion of the next step in improving representation for emerging and developing countries by January 2011. In Istanbul, the IMF members made a critical decision to that end. They supported a shift in quota share to dynamic emerging market and developing countries of at least five percent from over-represented countries to under-represented countries.

Concluding Remarks/Summary

In my remarks today, my goal was to focus our attention on some of the key lessons from the crisis for East Asia.

In the financial sphere, the crisis has called into question common tenets of financial sector supervision and monetary policy. I have argued that the current setup, namely the central bank focus on inflation fighting, should not be thrown overboard, but be adjusted in a pragmatic fashion. In terms of liquidity management, systemwide view, and regulatory perimeter, current international practice has clearly not been up to the mark and needs to be reformed.

In terms of global growth, it seems that the global economy has turned the corner. But, we should not forget that so far, this has been mainly due to massive policy support. And, while it is right—and in fact policy makers’ responsibility—to start formulating exit policies now, they should by no means be implemented until there are clear signs that the recovery is firmly underway.

Finally, in some likelihood the current crisis presents a structural break from the last decade, or so, when the U.S. consumer was a major source of global growth. This has important implications for Asia’s export-led growth model and for the role of international institutions including the IMF, both as a policy coordinator and provider of insurance.