Table 1. Overview of the World Economic Outlook Projections

(Percent change unless noted otherwise) |

| |

| |

Year over Year |

|

|

|

|

| |

|

|

Projections |

|

Difference from September 2011 WEO Projections |

|

Q4 over Q4 |

| |

|

|

|

Estimates |

Projections |

| |

2010 |

2011 |

2012 |

2013 |

|

2012 |

2013 |

|

2011 |

2012 |

2013 |

| |

| World Output 1 |

5.2 |

3.8 |

3.3 |

3.9 |

|

–0.7 |

–0.6 |

|

3.3 |

3.4 |

4.0 |

|

Advanced Economies |

3.2 |

1.6 |

1.2 |

1.9 |

|

–0.7 |

–0.5 |

|

1.3 |

1.3 |

2.1 |

|

United States |

3.0 |

1.8 |

1.8 |

2.2 |

|

0.0 |

–0.3 |

|

1.8 |

1.5 |

2.4 |

|

Euro Area |

1.9 |

1.6 |

–0.5 |

0.8 |

|

–1.6 |

–0.7 |

|

0.8 |

–0.2 |

1.2 |

| Germany |

3.6 |

3.0 |

0.3 |

1.5 |

|

–1.0 |

0.0 |

|

1.8 |

0.7 |

1.6 |

| France |

1.4 |

1.6 |

0.2 |

1.0 |

|

–1.2 |

–0.9 |

|

0.9 |

0.5 |

1.3 |

| Italy |

1.5 |

0.4 |

–2.2 |

–0.6 |

|

–2.5 |

–1.1 |

|

–0.1 |

–2.7 |

0.9 |

| Spain |

–0.1 |

0.7 |

–1.7 |

–0.3 |

|

–2.8 |

–2.1 |

|

0.2 |

–2.1 |

0.6 |

|

Japan |

4.4 |

–0.9 |

1.7 |

1.6 |

|

–0.6 |

–0.4 |

|

–0.9 |

1.9 |

1.5 |

|

United Kingdom |

2.1 |

0.9 |

0.6 |

2.0 |

|

–1.0 |

–0.4 |

|

0.8 |

1.0 |

2.4 |

| Canada |

3.2 |

2.3 |

1.7 |

2.0 |

|

–0.2 |

–0.5 |

|

2.1 |

1.7 |

2.0 |

| Other Advanced Economies 2 |

5.8 |

3.3 |

2.6 |

3.4 |

|

–1.1 |

–0.3 |

|

2.9 |

3.2 |

3.5 |

| Newly Industrialized Asian Economies |

8.4 |

4.2 |

3.3 |

4.1 |

|

–1.2 |

–0.3 |

|

3.8 |

4.3 |

3.8 |

| Emerging and Developing Economies 3 |

7.3 |

6.2 |

5.4 |

5.9 |

|

–0.7 |

–0.6 |

|

5.9 |

6.0 |

6.3 |

| Central and Eastern Europe |

4.5 |

5.1 |

1.1 |

2.4 |

|

–1.6 |

–1.1 |

|

3.4 |

1.4 |

3.0 |

| Commonwealth of Independent States |

4.6 |

4.5 |

3.7 |

3.8 |

|

–0.7 |

–0.6 |

|

3.2 |

3.5 |

3.7 |

| Russia |

4.0 |

4.1 |

3.3 |

3.5 |

|

–0.8 |

–0.5 |

|

3.5 |

2.8 |

4.0 |

| Excluding Russia |

6.0 |

5.5 |

4.4 |

4.7 |

|

–0.7 |

–0.4 |

|

. . . |

. . . |

. . . |

| Developing Asia |

9.5 |

7.9 |

7.3 |

7.8 |

|

–0.7 |

–0.6 |

|

7.4 |

7.9 |

7.6 |

| China |

10.4 |

9.2 |

8.2 |

8.8 |

|

–0.8 |

–0.7 |

|

8.7 |

8.5 |

8.4 |

| India |

9.9 |

7.4 |

7.0 |

7.3 |

|

–0.5 |

–0.8 |

|

6.7 |

6.9 |

7.2 |

| ASEAN-5 4 |

6.9 |

4.8 |

5.2 |

5.6 |

|

–0.4 |

–0.2 |

|

3.7 |

7.4 |

5.0 |

| Latin America and the Caribbean |

6.1 |

4.6 |

3.6 |

3.9 |

|

–0.4 |

–0.2 |

|

3.9 |

3.3 |

5.0 |

| Brazil |

7.5 |

2.9 |

3.0 |

4.0 |

|

–0.6 |

–0.2 |

|

2.1 |

3.8 |

4.1 |

| Mexico |

5.4 |

4.1 |

3.5 |

3.5 |

|

–0.1 |

–0.2 |

|

4.1 |

3.1 |

3.6 |

| Middle East and North Africa (MENA) 5 |

4.3 |

3.1 |

3.2 |

3.6 |

|

. . . |

. . . |

|

. . . |

. . . |

. . . |

| Sub-Saharan Africa |

5.3 |

4.9 |

5.5 |

5.3 |

|

–0.3 |

–0.2 |

|

. . . |

. . . |

. . . |

| South Africa |

2.9 |

3.1 |

2.5 |

3.4 |

|

–1.1 |

–0.6 |

|

2.4 |

3.0 |

3.7 |

| Memorandum |

|

|

|

|

|

|

|

|

|

|

|

| European Union |

2.0 |

1.6 |

–0.1 |

1.2 |

|

–1.5 |

–0.7 |

|

0.8 |

0.3 |

1.7 |

| World Growth Based on Market Exchange Rates |

4.1 |

2.8 |

2.5 |

3.2 |

|

–0.7 |

–0.4 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

| World Trade Volume (goods and services) |

12.7 |

6.9 |

3.8 |

5.4 |

|

–2.0 |

–1.0 |

|

. . . |

. . . |

. . . |

| Imports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

11.5 |

4.8 |

2.0 |

3.9 |

|

–2.0 |

–0.8 |

|

. . . |

. . . |

. . . |

| Emerging and Developing Economies |

15.0 |

11.3 |

7.1 |

7.7 |

|

–1.0 |

–1.0 |

|

. . . |

. . . |

. . . |

| Exports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

12.2 |

5.5 |

2.4 |

4.7 |

|

–2.8 |

–0.8 |

|

. . . |

. . . |

. . . |

| Emerging and Developing Economies |

13.8 |

9.0 |

6.1 |

7.0 |

|

–1.7 |

–1.6 |

|

. . . |

. . . |

. . . |

| Commodity Prices (U.S. dollars) |

|

|

|

|

|

|

|

|

|

|

|

| Oil 6 |

27.9 |

31.9 |

–4.9 |

–3.6 |

|

–1.8 |

–3.1 |

|

. . . |

. . . |

. . . |

| Nonfuel (average based on world commodity export weights) |

26.3 |

17.7 |

–14.0 |

–1.7 |

|

–9.3 |

2.2 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

| Consumer Prices |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

1.6 |

2.7 |

1.6 |

1.3 |

|

0.2 |

–0.1 |

|

2.9 |

1.2 |

1.3 |

| Emerging and Developing Economies 3 |

6.1 |

7.2 |

6.2 |

5.5 |

|

0.3 |

0.4 |

|

6.5 |

5.6 |

4.8 |

| London Interbank Offered Rate (percent) 7 |

|

|

|

|

|

|

|

|

|

|

|

| On U.S. Dollar Deposits |

0.5 |

0.5 |

0.9 |

0.9 |

|

0.4 |

0.3 |

|

. . . |

. . . |

. . . |

| On Euro Deposits |

0.8 |

1.4 |

1.1 |

1.2 |

|

–0.1 |

–0.4 |

|

. . . |

. . . |

. . . |

| On Japanese Yen Deposits |

0.4 |

0.4 |

0.5 |

0.2 |

|

0.2 |

0.0 |

|

. . . |

. . . |

. . . |

| |

|

Note: Real effective exchange rates are assumed to remain constant at the levels prevailing during November 14–December 12, 2011. When economies are not listed alphabetically, they are ordered on the basis of economic size. The aggregated quarterly data are seasonally adjusted. |

|

1The quarterly estimates and projections account for 90 percent of the world purchasing-power-parity weights. |

|

2Excludes the G7 and euro area countries. |

|

3The quarterly estimates and projections account for approximately 80 percent of the emerging and developing economies. |

|

4Indonesia, Malaysia, Philippines, Thailand, and Vietnam. |

|

5The September 2011 WEO projections did not include Libya due to the uncertain political situation, but Libya is included in these aggregate WEO calculations. Excluding Libya, MENA growth projections for 2012 and 2013 are lower by –1.6 and –1.2 percentage points, respectively, than in the September 2011 WEO. Note that the World and Emerging and Developing Economies aggregates are also not directly comparable with those in the September 2011 WEO because of Libya’s inclusion, but Libya’s weight in these aggregates is much lower. |

|

6Simple average of prices of U.K. Brent, Dubai, and West Texas Intermediate crude oil. The average price of oil in U.S. dollars a barrel was $104.23 in 2011; the assumed price based on futures markets is $99.09 in 2012 and $95.55 in 2013. |

|

7Six-month rate for the United States and Japan. Three-month rate for the euro area. |

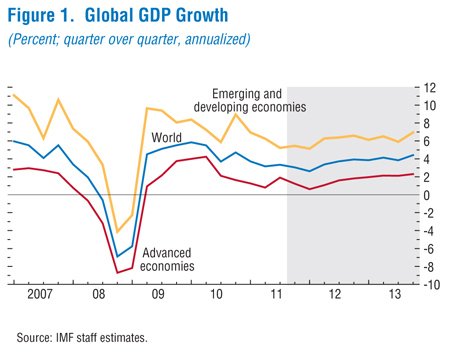

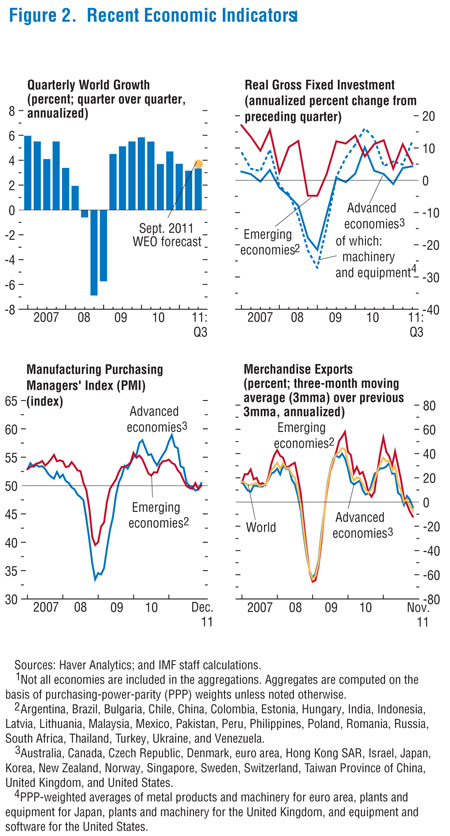

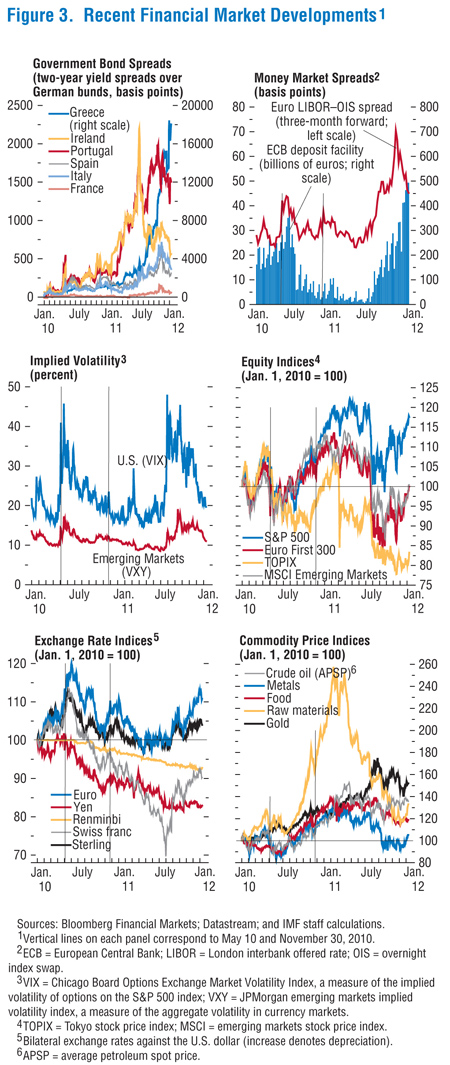

Lately, the near-term outlook has noticeably deteriorated, as evidenced by worsening high-frequency indicators in the last quarter of 2011 (Figure 2: CSV|PDF). The main reason is the escalating euro area crisis, which is interacting with financial fragilities elsewhere (Figure 3: CSV|PDF). Specifically, concerns about banking sector losses and fiscal sustainability widened sovereign spreads for many euro area countries, which reached highs not seen since the launch of the Economic and Monetary Union. Bank funding all but dried up in the euro area, prompting the European Central Bank (ECB) to offer a three-year Long-Term Refinancing Operation (LTRO). Bank lending conditions moved sideways or deteriorated across a number of advanced economies. Capital flows to emerging economies fell sharply. Currency markets were volatile, as the Japanese yen appreciated and many emerging market currencies depreciated significantly.

The recovery is expected to stall in many economies

The updated WEO projections see global activity decelerating but not collapsing. Most advanced economies avoid falling back into a recession, while activity in emerging and developing economies slows from a high pace. However, this is predicated on the assumption that in the euro area, policymakers intensify efforts to address the crisis. As a result, sovereign bond premiums stabilize near current levels and start to normalize in early 2013. Also, policies succeed in limiting deleveraging by euro area banks. Credit and investment in the euro area contract only modestly, with limited financial and trade spillovers to other regions.

Overall, activity in the advanced economies is now projected to expand by 1½ percent on average during 2012–13. Given the depth of the 2009 recession, these growth rates are too sluggish to make a major dent in very high unemployment. Moreover, the 2012 growth projection is a downward revision of ¾ percentage points relative to the September 2011 WEO.

• The euro area economy is now expected to go into a mild recession in 2012—consistent with what was presented as a downside scenario in the January 2011 WEO Update. The significant downward revision (1½ percentage points) since the September 2011 WEO is due to the rise in sovereign yields, the effects of bank deleveraging on the real economy, and the impact of additional fiscal consolidation announced by euro area governments.

• With only limited policy room, growth in most other advanced economies is also lower, mainly due to adverse spillovers from the euro area via trade and financial channels that exacerbate the effects of existing weaknesses. For the United States, the growth impact of such spillovers is broadly offset by stronger underlying domestic demand dynamics in 2012. Nonetheless, activity slows from the pace reached during the second half of 2011, as higher risk aversion tightens financial conditions and fiscal policy turns more contractionary.

During 2012–13, growth in emerging and developing economies is expected to average 5¾ percent—a significant slowdown from the 6¾ percent growth registered during 2010–11 and about ½ percentage point lower than projected in the September 2011 WEO. This reflects the deterioration in the external environment, as well as the slowdown in domestic demand in key emerging economies. Despite a substantial downward revision of ¾ percentage point, developing Asia is still projected to grow most rapidly at 7½ percent on average during 2012–13. Economic activity in the Middle East and North Africa is expected to accelerate in 2012-13, driven mainly by the recovery in Libya and the continued strong performance of other oil exporters. But most oil-importing countries in the region face muted growth prospects due to longer-than-expected political transitions and an adverse external environment. The impact of the global slowdown on sub-Saharan Africa has to date been limited to a few countries—most notably, South Africa—and the region's output is expected to expand by around 5½ percent in 2012. The adverse spillover effects are expected to be largest for central and eastern Europe, given the region’s strong trade and financial linkages with the euro area economies. The impact on other regions is expected to be relatively mild, as macroeconomic policy easing is expected to largely offset the effects of slowing demand from advanced economies and rising global risk aversion. For many emerging and developing economies, the strength of the forecasts also reflects relatively high commodity prices (see below).

Commodity prices and consumer price inflation recede, but risks remain

Commodity prices generally declined in 2011, in response to weaker global demand. Oil prices, however, have held up in recent months, largely because of supply developments. Moreover, geopolitical risks to oil prices have risen again. These risks are expected to remain elevated for some time, and oil prices will ease only marginally in 2012 despite less favorable prospects for global activity. As a result, the IMF’s baseline petroleum price projection for 2012 is broadly unchanged since the September 2011 WEO ($99 a barrel compared with $100). For non-oil commodities, improving supply conditions and slowing global demand are expected to cause further price declines. Non-oil commodity prices are projected to fall by 14 percent in 2012. In the near term, the risks to prices are to the downside for most of these commodities.

Global consumer price inflation is projected to ease as demand softens and commodity prices stabilize or recede. In advanced economies, ample economic slack and well-anchored inflation expectations will keep inflation pressures subdued, as the effects of last year’s higher commodity prices wane. Inflation is projected to fall to about 1½ percent in the course of this year, down from a peak of about 2¾ percent in 2011. In emerging and developing economies, pressures are also expected to drop, as both growth and food price inflation slow. However, inflation is expected to remain persistent in some regions. Overall, consumer prices in these economies are projected to decelerate, with inflation around 6¼ percent during 2012, down from over

7¼ percent in 2011.

Downside risks have risen sharply

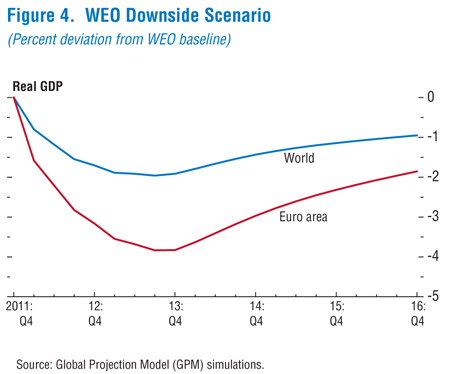

Downside risks stem from several sources. The most immediate risk is intensification of the adverse feedback loops between sovereign and bank funding pressures in the euro area, resulting in much larger and more protracted bank deleveraging and sizable contractions in credit and output. Figure 4 (CSV|PDF) presents such a downside scenario. It assumes that sovereign spreads temporarily rise. Increased concerns about fiscal sustainability force a more front-loaded fiscal consolidation, which depresses near-term demand and growth. Bank asset quality deteriorates by more than in the baseline, owing to higher losses on sovereign debt holdings and on loans to the private sector. Private investment contracts by additional 1¾ percentage points of GDP (relative to WEO projections). As a result, euro area output is reduced by about 4 percent relative to the WEO forecast. Assuming that financial contagion to the rest of the world is more intense than in the baseline (but weaker than following the collapse of Lehman Brothers in 2008) and taking into consideration spillovers via international trade, global output will be lower than the WEO projections by about 2 percent.

Another downside risk arises from insufficient progress in developing medium-term fiscal consolidation plans in the United States and Japan. In the short term, this risk might be mitigated as the turbulence in the euro area makes government debt of these economies more attractive to investors. However, as long as public debt levels are projected to rise over the medium term, and in the absence of well-defined and credible fiscal consolidation strategies, there is the possibility of turmoil in global bond and currency markets. A more immediate risk is that an accident-prone political economy will lead to excessive fiscal tightening in the near term in the United States.

In key emerging economies, risks relate to the possibility of a hard landing, especially in the context of uncertain (possibly slowing) potential output. In recent years, a number of major emerging economies experienced buoyant credit and asset price growth as well as rising financial vulnerabilities. This has buoyed demand and may have led to overestimation of the trend growth rates in these economies. Should the dynamics of real estate and credit markets unwind—triggered by losses in confidence and a paring back of expectations at home or by falling demand from abroad—the impact on economic activity could be very damaging.

Moreover, concerns about geopolitical oil supply risks are increasing again. The oil market impact of intensified concerns about an Iran-related oil supply shock (or an actual disruption) would be large, given limited inventory and spare capacity buffers, as well as the still-tight physical market conditions expected throughout 2012.

Decisive and consistent policy action is urgently needed

The current environment—characterized by fragile financial systems, high public deficits and debt, and interest rates close to the zero bound—provides fertile ground for self-perpetuating pessimism and the propagation of adverse shocks, the most critical of which is a worsening of the crisis in the euro area. In this setting, there are three requirements for a more resilient recovery: sustained but gradual adjustment; ample liquidity and easy monetary policy, mainly in advanced economies; and restored confidence in policymakers’ ability to act. Importantly, not all countries should adjust in the same way, to the same extent, or at the same time, lest their efforts become self-defeating. Countries with relatively strong fiscal and external positions, for example, should not adjust to the same extent as countries lacking those strengths or facing market pressures. Through mutually consistent actions, policymakers can help anchor expectations and reestablish confidence.

• Fiscal adjustment. In the near term, sufficient fiscal adjustment is in motion in most advanced economies. Countries should let automatic stabilizers operate freely for as long as they can readily finance higher deficits. Among those countries, those with very low interest rates or other factors that create adequate fiscal space, including some in the euro area, should reconsider the pace of near-term fiscal consolidation. Overdoing fiscal adjustment in the short term to counter cyclical revenue losses will further undercut activity, diminish popular support for adjustment, and undermine market confidence. Among the major economies, a specific concern is that political paralysis in the United States will lead to an excessively rapid unwinding of stimulus spending. Regarding the medium term, the United States and Japan should push ahead in formulating and implementing credible medium-term consolidation plans, because neither country can take for granted its status as a safe haven. Measures could include reforms to slow the growth of health care and pension spending, caps on discretionary spending, and tax system reforms to boost fiscal revenue. Putting in place credible medium-term plans also will create policy room to support balance sheet repair, growth, and job creation. Fiscal policies are discussed in more detail in the January 2012 Fiscal Monitor Update.

• Liquidity. While fiscal consolidation proceeds in the advanced economies, monetary policy should continue to support growth, as long as inflation expectations remain anchored and unemployment stays high. If downside risks to growth materialize, further monetary stimulus—including through quantitative easing—may well be necessary. In this regard, targeted programs to help ease credit constraints on businesses and households would be useful in economies where monetary transmission is impaired. In the euro area, it is critical to break the adverse feedback loops between subpar growth, deteriorating fiscal positions, and weakening bank balance sheets, which may very well lead to a prolonged period of asset and consumer price deflation. Addressing this requires action on several fronts. First, additional and timely monetary easing by the ECB will be important, consistent with its mandate to ensure stable prices. Also, the ECB should continue to provide liquidity and stay fully engaged in securities purchases to help maintain confidence in the euro. And sufficient funding must be made available through the European Financial Stability Facility (EFSF) and the European Stability Mechanism (ESM) to countries facing severe funding constraints.

• Bank deleveraging. To break the adverse loops between weak growth and deteriorating bank balance sheets, more capital needs to be injected into the euro area banks (including from public sources) and supervisors must do whatever possible to avoid excessively fast deleveraging that could lead to a devastating credit crunch (see the January 2012 Global Financial Stability Report Update). Individual countries under pressure may well require recourse to euro-wide resources to facilitate bank recapitalization.

• Financial adjustment. Easy funding in the short-term must be coupled with continued progress to repair and reform financial systems. This is a critical element of normalizing credit conditions and would help reduce the burden on monetary and fiscal policy of supporting the recovery. Financial sector policies are discussed in more detail in the January 2012 Global Financial Stability Report Update.

Restoring confidence in the viability of the euro area hinges on deepening financial and fiscal integration over time and on implementing structural reforms to help resolve internal imbalances. On the financial front, moving toward a model of common supervision, resolution, and deposit insurance will strengthen and unify the euro area financial system and break the adverse feedback loops between banks and sovereigns. In the near term, a pan-euro area facility that has the capacity to take direct stakes in banks will also help break these loops. Further fiscal integration is also essential and must include more risk sharing across euro area members, alongside stronger fiscal discipline or centralization. The EFSF and ESM are major steps in this direction. But adding substantial real resources to what is currently available, by folding the EFSF into the ESM and increasing the size of the ESM, would help greatly. In the medium term, reforms to labor and product markets will help address underlying internal imbalances and competitiveness problems, which are the root causes of the travails; in the short term, they may help anchor market expectations.

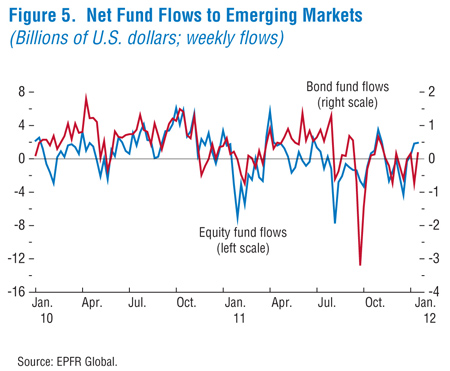

In emerging and developing economies, the near-term focus should be on responding to moderating domestic demand and slowing external demand from advanced economies, while dealing with volatile capital flows. The specific conditions facing these economies and the policy room available to them vary widely, and so will the appropriate policy response. In general, inflation pressures have eased, credit growth has peaked, and capital inflows have diminished (Figure 5: CSV|PDF). Economies where inflation is under control, public debt is not high, and external surpluses are appreciable (including China and selected emerging economies in Asia) can afford to deploy additional social spending to support poorer households in the face of weakening external demand. Economies with diminishing inflation pressure but weaker fiscal fundamentals (including various economies in Latin America) can afford to stop tightening or to ease monetary policy, provided they manage to control lending to overheating sectors (such as real estate) through macroprudential measures. Those that suffer from both relatively high inflation and public debt (including India and various economies in the Middle East) may need to take a more cautious stance on any policy easing.

Collective action can help set the global economy on a more robust growth trajectory by fostering global demand rebalancing. In many advanced economies, notably those with external deficits, the deleveraging of households is set to continue for some time. Structural reforms to boost potential output—including measures to reform labor and product markets and strengthen economies’ resilience to population aging—can lower but not obviate the need for deleveraging. Achieving more resilient global growth in this setting will require that economies with strong household balance sheets and external positions eliminate distortions that weigh on domestic demand. Depending on the precise challenges facing these economies, actions could usefully focus on building more market-oriented exchange systems, improving social safety nets and pension, health care, and education systems; strengthening financial sectors; and improving the business environment for private investment.