Recent strains at some banks in the United States and Europe are a powerful reminder of pockets of elevated financial vulnerabilities built over years of low rates, compressed volatility, and ample liquidity.

Such risks could intensify in coming months amid the continued tightening of monetary policy globally, making it especially important to understand and safeguard this broad swath of the financial sector that comprises an array of institutions beyond banks. Nonbank financial intermediaries, including pension funds, insurers, and hedge funds, also play a key role in the global financial system by providing financial services and credit and thus supporting economic growth.

The growth of the NBFI sector accelerated after the global financial crisis, accounting now for nearly 50 percent of global financial assets. As such, the smooth functioning of the nonbank sector is vital for financial stability.

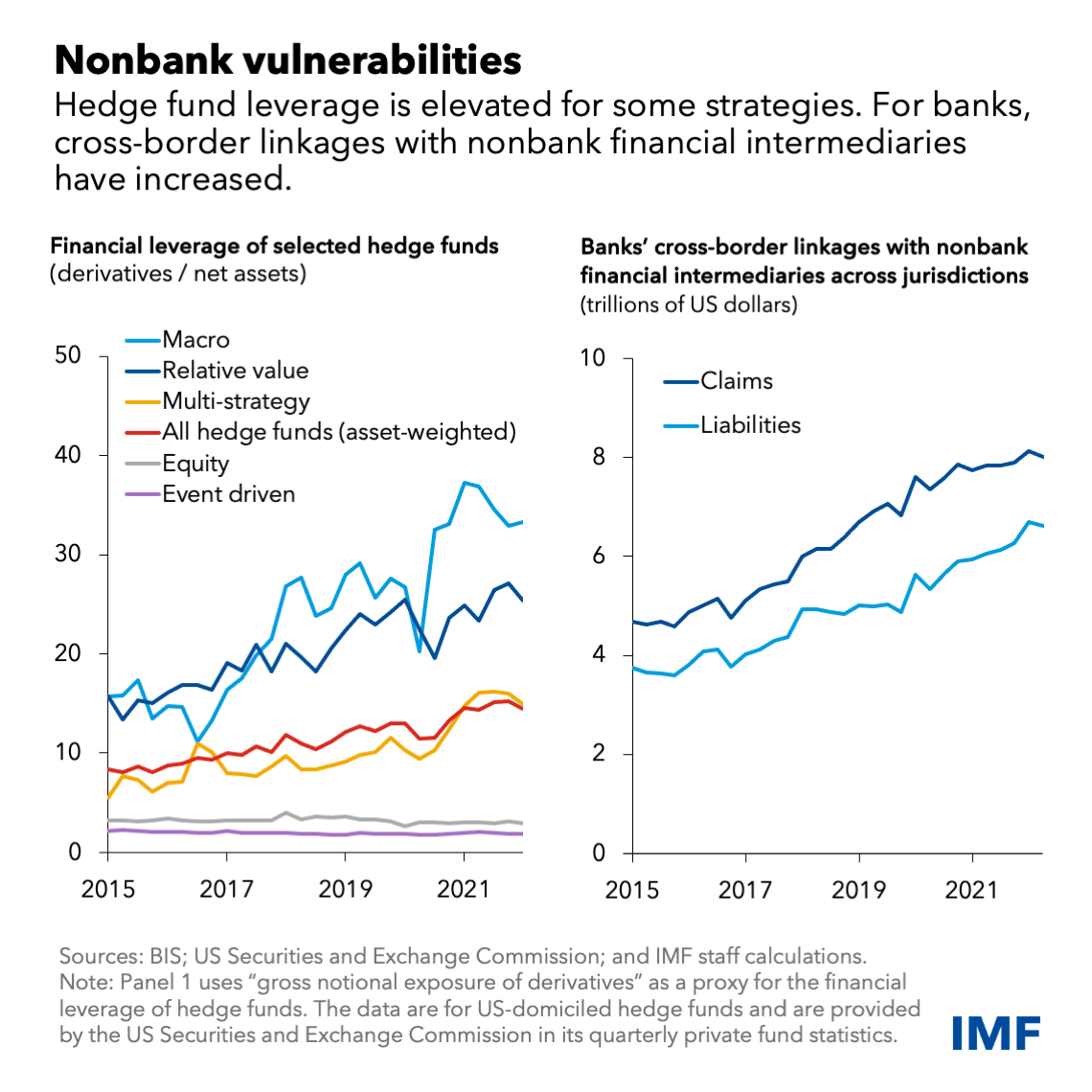

However, NBFI vulnerabilities appear to have increased in the past decade. As we show in an analytical chapter of the latest Global Financial Stability Report, NBFI stress tends to emerge alongside elevated leverage, for example borrowing money to finance their investments or boost returns, or using financial instruments, like derivatives.

Stress is also brought on by liquidity mismatches, where an institution is unable to generate sufficient cash either through liquidation of assets, such as bonds or equities, or use of credit lines to satisfy investor redemption requests.

Finally, high levels of interconnectedness among NBFIs and with

traditional banks can also become a crucial amplification channel of

financial stress.

Last year’s UK pension fund and liability-driven investment strategies

episode underscores the perilous interplay of leverage, liquidity risk, and

interconnectedness.

Concerns about the country’s fiscal outlook led to a sharp rise in UK

sovereign bond yields that, in turn, led to large losses in

defined-benefit pension fund investments that borrowed against such

collateral, causing margin and collateral calls. To meet these calls, pension funds were forced to sell government bonds,

pushing their yields even higher.

It is useful to take a step back and look at the current environment in which NBFIs find themselves. With the fastest inflation in decades, and with price stability at the core of most central bank mandates, injecting central bank liquidity for financial stability purposes could complicate the fight against inflation. In a low-inflation environment, central banks can respond to financial stress by easing policy such as cutting interest rates or purchasing assets to restore market functioning.

Amid high inflation, however, challenging tradeoffs may emerge for central banks between fostering financial stability and achieving price stability during periods of stress that may threaten the health of the financial system.

Policymakers need appropriate tools to tackle turmoil in the NBFI sector that may adversely affect financial stability. Robust surveillance, regulation, and supervision are essential pre-requisites. Policymakers must also narrow or eliminate gaps in regulatory reporting of key data, including how much risk firms are taking with their borrowing or use of derivatives.

Policies are also needed to ensure NBFIs better manage risks, and this might be accomplished through timely and granular public data disclosures and governance requirements. These improvements in private sector risk management must be supported by appropriate prudential standards, including capital and liquidity requirements, alongside better resourced and stricter supervision.

This would help steer the business decisions of the NBFIs themselves away from excessive risk taking by removing both the incentive and opportunity to take on too much risk. It would also likely reduce the need for and frequency of central bank intervention to provide liquidity support during systemic stress events.

If central bank intervention is needed, they can consider three broad types of support:

-

Discretionary market-wide intervention

should be temporary and targeted to those NBFI segments posing risk to

financial stability. The timing is also critical—a framework should be

in place where data-driven metrics trigger a potential intervention,

while policymakers ultimately retain the discretion to intervene.

-

Lender-of-last-resort intervention

should be available when a systemically important nonbank institution

comes under stress. Such lending should be at the discretion of the

central bank, at a higher interest rate, fully collateralized, and

accompanied by greater supervisory oversight. A clear timeline should

be established for restoring the NBFI’s liquidity and return to market

finance.

- Access to standing lending facilities could be granted to specific NBFI entities to reduce spillovers to the financial system, although the bar for such access should be very high to avoid moral hazard. Access should not be granted without the appropriate regulatory and supervisory regimes for the different types of NBFIs.

Clear communication is critical, so that liquidity support is not perceived to be working at cross-purposes with monetary policy. For example, purchasing assets to restore financial stability while continuing with quantitative tightening to bring inflation back to target may cloud intent and complicate communication. Announcements of central bank liquidity support should clearly explain the financial stability objectives, program parameters and timing.

At the same time, cooperation between domestic policy makers and international coordination between national authorities is essential. This helps better identify risks and manage crises. Specifically, internationally coordinated reforms can reduce the risks of cross-border spillovers, regulatory arbitrage, and market fragmentation.

Given the growing size and intermediation capacity of the NBFI sector globally, the development of the right toolbox for access to central bank liquidity, along with the appropriate guardrails limiting the need for its use, is a priority. The need to do so is all that much greater given that financial sector vulnerabilities could be poised to grow amid the continued tightening of monetary policy.

—This blog is based on Chapter 2 of the April 2023 Global Financial Stability Report, “Nonbank Financial Intermediaries: Vulnerabilities Amid Tighter Financial Conditions.”