Students in Ancash, Peru: improving education can support long-term growth in the region (photo: Mariana Bazo/Reuters/Newscom)

Latin America and the Caribbean: Bouncing Back from Recession

May 19, 2017

Latin America and the Caribbean is expected to gradually emerge from recession in 2017, but to secure strong and inclusive growth going forward the region needs to address gaps in infrastructure, improve education outcomes, strengthen the business environment, and tackle corruption, the IMF said in its latest Regional Economic Outlook for the Western Hemisphere.

Related Links

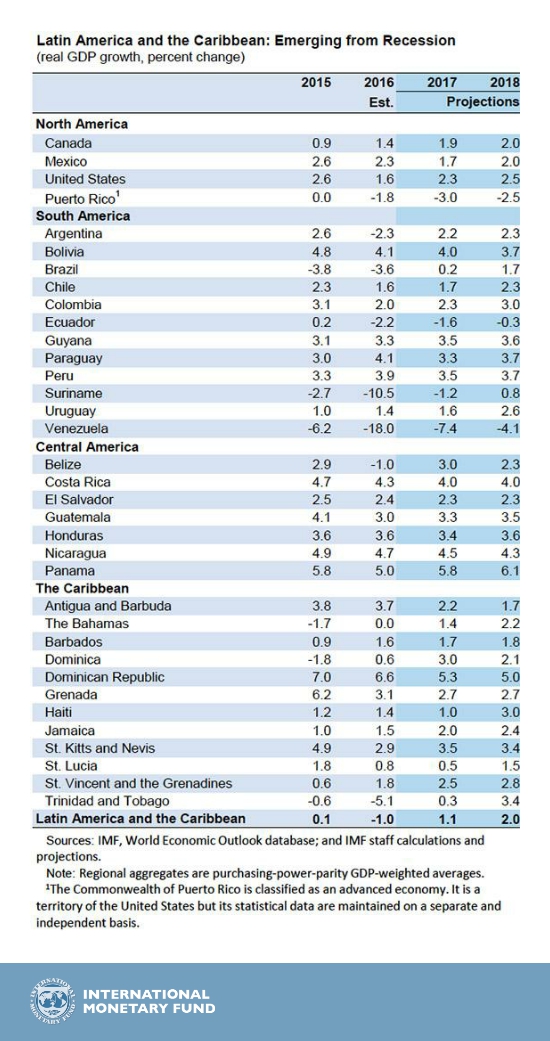

Economic growth in Latin America and the Caribbean in 2016 was the third-lowest in 30 years—contracting by 1 percent after stagnating in 2015. Growth was held back by weak domestic demand from lower commodity prices, ongoing fiscal and external adjustment in some countries, and other country-specific domestic factors.

The IMF forecasts growth to expand by 1.1 percent this year and 2 percent in 2018. Over the medium term, growth is expected to remain subdued at 2.6 percent.

According to the report, this outlook is shaped by key shifts in the global economic and policy landscape, including a modest rebound in commodity prices and partner country demand, and higher global policy uncertainty. Domestic developments will continue to play a significant role in determining growth in many economies.

“With heightened policy uncertainty at the global level but low market volatility, countries in our region should focus on insuring against downside risks, while targeting strong, sustainable, and inclusive growth,” Alejandro Werner, Director of the IMF’s Western Hemisphere Department, told a press conference in São Paulo, Brazil.

External and domestic forces

In this challenging external environment, the report pointed out that many countries in the region should advance fiscal and external adjustments to preserve or rebuild policy buffers (for example, by improving primary balances to stabilize rising public debt).

Charting a course toward higher, sustainable, and more equitable growth will also require domestic reforms. These vary by country, and include closing infrastructure gaps; improving the business environment, governance, and education outcomes; deepening regional trade integration; and encouraging female labor force participation to boost medium-term growth and foster income convergence. These policies would help raise future growth by increasing contributions from labor, capital, and productivity.

Regional roundup

Growth prospects in South America are shaped by a combination of key domestic developments and shifts in the global landscape.

In Argentina, the recovery is under way. Growth is expected to grow 2¼ percent in 2017, driven by a rebound of private consumption, stronger public capital spending, and a pickup in exports.

In Brazil, after two years of recession, growth is expected to return to positive territory—estimated at 0.2 percent in 2017—thanks to a bumper soybean crop, one-time boost to consumption, a faster-than-expected decline in inflation, and higher iron ore prices.

In Venezuela, the economy is expected to remain in a deep recession and on a path to hyperinflation. Because there is no sign of a shift in economic policies, real GDP is expected to fall by 7.4 percent in 2017.

For other commodity exporters, the modest recovery in commodity prices will provide some relief. Despite slightly better external conditions, the outlook for Chile remains subdued, reflecting lingering domestic weaknesses. As a result, growth in 2017 is projected at 1.7 percent.

In Colombia, the orderly economic slowdown continued last year as domestic demand has been adjusting to a permanent shock to national income. While one-off factors led to a weaker-than anticipated growth in 2016, a mild rebound is expected in 2017.

Peru ’s economy grew at a rapid pace in 2016. But investment continues to lag and domestic headwinds related to a political bribery probe in connection with the Brazilian company Odebrecht, along with the worst flooding and landslides in decades, may put a drag on 2017 investment and growth.

The outlook and risks for Central America and Mexico are being influenced by their exposure to the United States through trade, migration, and foreign direct investment. Mexico’s real GDP growth is expected to decelerate to 1.7 percent in 2017. Uncertainty about future trade relations with the United States and higher borrowing costs are expected to more than offset the positive effect from stronger U.S. growth.

Growth in Central America, Panama, and the Dominican Republic is expected to remain broadly unchanged from last year in 2017. Strong U.S. growth will help support exports and remittances.

Prospects for the Caribbean region are improving, with growth in both tourism-dependent economies and commodity exporters projected to be in the 1.5-3 percent range for 2017 and 2018.