The Global Economy and Financial Markets: Where Next?

Speech by John LipskyFirst Deputy Managing Director, International Monetary Fund

At the Lowy Institute, Sydney, Australia,

July 31, 2007

| Presentation |

{kind=link}

Good afternoon, ladies and gentlemen. It is a pleasure to be here in Sydney. I'd like to thank the Lowy Institute for inviting me to address this distinguished gathering. Little did we know when we set the topic for today's meeting that it would seem so relevant. Although the answer to the question "Where Next?" is inherently uncertain, I am happy to have the chance to exchange views.

For the global economy, the last decade has represented a period of impressive progress, interspersed with episodes that were challenging, and even threatening at times. The latest financial market volatility has ushered in a moment of anxiety and concern. At the very least, it is apparent that global markets are re-pricing credit risk.

In this era of financial globalization, markets have become increasingly integrated. Thus, the latest bout of market volatility has been experienced globally, at least to some degree. Distant events can have sharp impacts, even on local institutions.

My principal messages today are straightforward: A strongly symbiotic relationship evolved in recent years between global economic growth, financial innovation, and financial globalization. Increased financial integration has been a natural counterparty to the increasing trade openness that has been developing over the past two decades, and that has been a key driver of sustained rapid global growth.

After an exceptionally benign period of virtually universal advances in economic performance—that helped to carry many financial markets into uncharted territory—investors have suddenly become more cautious. Thus, financial market participants appear to be re-assessing their assumptions about the global economic outlook, while trying to find more solid grounds on which to price credit risk.

This search for new market ranges may take some time, and it is likely to involve additional volatility. However, the degree of recent market turbulence should not be exaggerated. The fundamental underpinnings of the current global expansion appear to be reasonably solid. If so, the current market strains most likely will help set the stage for both financial and fundamental adjustments. These, in turn, will help set the stage for a new leg of the global expansion.

However, the risks of a less favorable outcome cannot be ignored. What can be taken for granted is that financial market participants will be responding to the latest developments. Policymakers need to take stock of whether new actions are needed to reduce financial market risks.

In the balance of my remarks today, I will flesh out these points—focusing on financial market developments. But most of all, I look forward to having a chance to discuss these topics with you following my presentation.

Slide 2: The Favorable Global Backdrop

{kind=link}

What makes the recent turmoil in global financial markets particularly noteworthy is that it comes at a time when global macroeconomic performance appears to be favorable. Not only has the global economy performed strongly over the last few years, most macroeconomic data still point towards a continuation of this trend.

Slide 3: The Global Expansion Has Been Strong

{kind=link}

The global economy continues to grow strongly, while inflation appears to be well-controlled, despite higher energy and commodity prices. Thus, the IMF's baseline global forecast is that 2007/2008 growth will register at an annual rate of just over 5%. Moreover, virtually universal growth is envisaged to continue.

Domestic demand growth in Japan and the euro area economies has strengthened in recent quarters, hopefully adding to the expansion's resilience. The contributions of China, India, Russia, and Brazil to global growth have also been strong, whether measured by market exchange rates or by purchasing power parity weights. In fact, China's contribution this year to global GDP in dollars, measured at market exchange rates, is quite likely to exceed that of the United States. Our global forecast for this year and next anticipates that over half of global growth will be accounted for by emerging market economies. However, this does not diminish the importance of the US economy for the world outlook—a sharp US growth slowdown would likely test growth outcomes elsewhere.

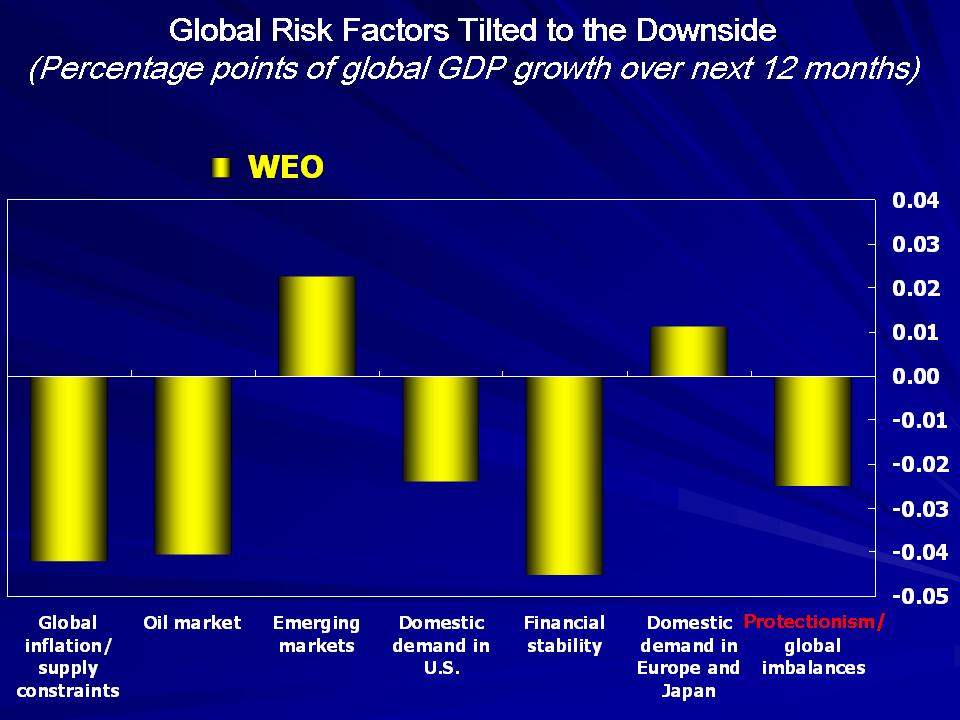

Slide 4: Global Risk Factors Tilted to the Downside

{kind=link}

Despite this favorable outlook, my IMF colleagues and I judge that the risks to this baseline forecast are tilted to the downside, reflecting several factors. These include inflation pressures that could arise either from capacity constraints or rising energy prices. They also include risks that could arise from heightened financial market instability, from the troubling signs of rising protectionism and from the still-present possibility of a disorderly unwinding of global payments imbalances. At the same time, stronger than expected growth in emerging markets, and a stronger than expected recovery in the euro area and Japan constitute upside risks to the IMF forecast. Of course, the downside risks could be inter-related. That is, there is no guarantee that these risks would materialize in an isolated fashion.

{kind=link}

The current period of financial innovation and globalization is characterized by three hallmarks:

The first is securitization, or the progressive replacement of bank credit to the household and corporate sectors by instruments that are tradable in public or private markets.

The second is the development of new risk transfer instruments. These have allowed financial market participants to break out risk embedded in traditional financial instruments and trade them separately. This trend began more than 20 years ago with the development of the interest rate swap market. In the past few years, the pace of financial innovation has accelerated, encompassing the establishment of an increasingly liquid market for credit default swaps (or CDS), and other new derivative contracts that have assumed increasingly important roles.

The securitization of corporate debt has been greatly aided by the maturing of the CDS market, permitting investors to take positions with regard to corporate credit quality without having to enter the underlying "cash" market. This factor has facilitated corporate financing, presumably boosting the sector's resilience and efficiency.

The third hallmark of this period of financial innovation and globalization is the effect that these developments in financial engineering have had on asset management. Financial institutions like hedge funds and private equity have been at the forefront of financial innovation, and have made extensive use of new instruments.

This focus on innovation helps to explain why the relative importance of these new institutions has exceeded their relative share of assets under management. For example, hedge funds at present account for between 2% and 5% of global assets under management. However, they account for a far larger share of turnover in markets because they typically follow active management strategies, facilitated by the new risk transfer instruments. As a result, they at times play the role marginal price setter. In fact, the newer the market—such as those for credit default swaps and structured credit products such as collateralized debt or loan obligations (CDOs and CLOs) —the greater their relative role.

Slide 6: The Effects - Record Cross-Border Flows

{kind=link}

Partly driven by financial innovation, there has been a massive surge in cross-border capital flows. In particular, cross-border capital flows as a share of world GDP have doubled since the beginning of this decade, and they are more than triple the share of the early 1990s. Of course, this dramatic growth has reflected more than financial innovation alone: Favorable macroeconomic developments have played an important role, as well. The demand for external financial assets has risen in some cases either because of a decline in domestic investment rates, or because domestic financial markets are relatively rudimentary. The result has been a tide of financial flows that have so far been relatively unhampered during the past two years or so by the monetary policy tightening in advanced economies.

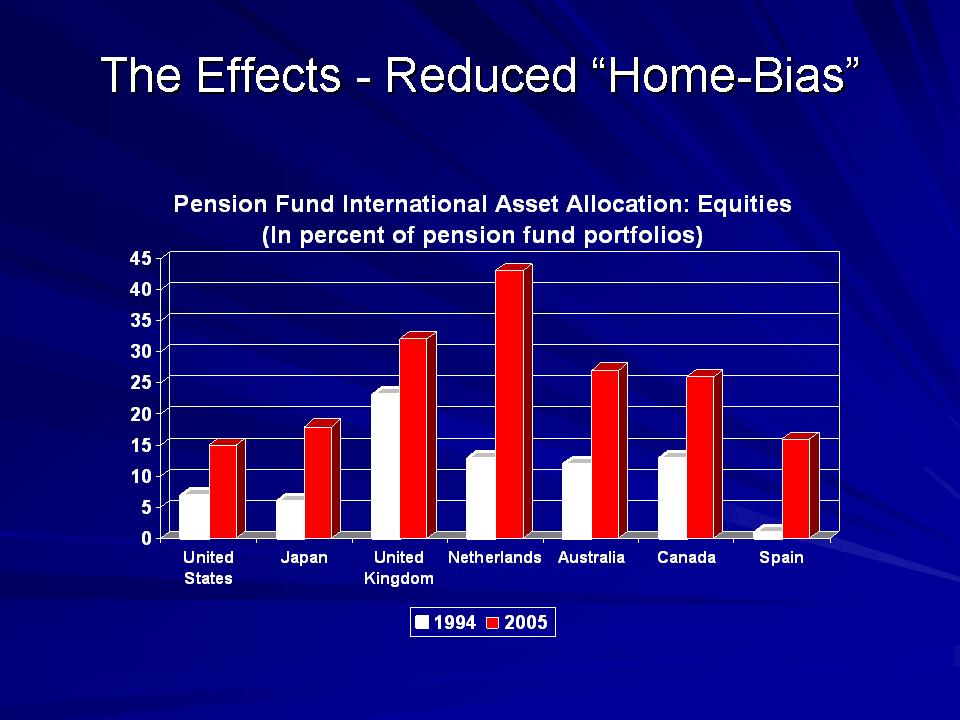

Slide 7:The Effects—Reduced Home Bias

{kind=link}

It should come as no surprise that such a surge in global capital flows has been accompanied by a reduction in so-called "home bias" in the investment choices of asset managers. For example, the average share of international equities in developed economy pension fund portfolios grew anywhere from two to sixteen-fold between 1990 and 2005. Moreover, pension funds are relatively conservative institutions—so the loss of home-bias likely would be even more striking if data availability allowed the inclusion of mutual funds, hedge funds, sovereign wealth funds, and other classes of asset managers

Slide 8: The Latest Challenge—The Re-Pricing of Credit Risk

{kind=link}

Examining the symbiotic interplay between the post-2002 global growth surge with financial innovation and globalization has laid the groundwork for taking a closer look at the latest financial market developments, and the challenge they are posing to this relationship.

Slide 9: US Sub-Prime Market Credit Quality Deterioration

{kind=link}

The epicenter of the recent increased financial market volatility has been the US sub-prime mortgage market. Of course, this is a relatively new market, facilitated by the use of new financial risk transfer instruments. After a steady improvement in delinquency rates on those sub-prime adjustable rate mortgages belonging to the 2000 and 2003 vintages, the subsequent rapid growth in the overall market size was accompanied by a notable deterioration in the delinquency rate. By the 2006 vintage, the deterioration had become extreme.

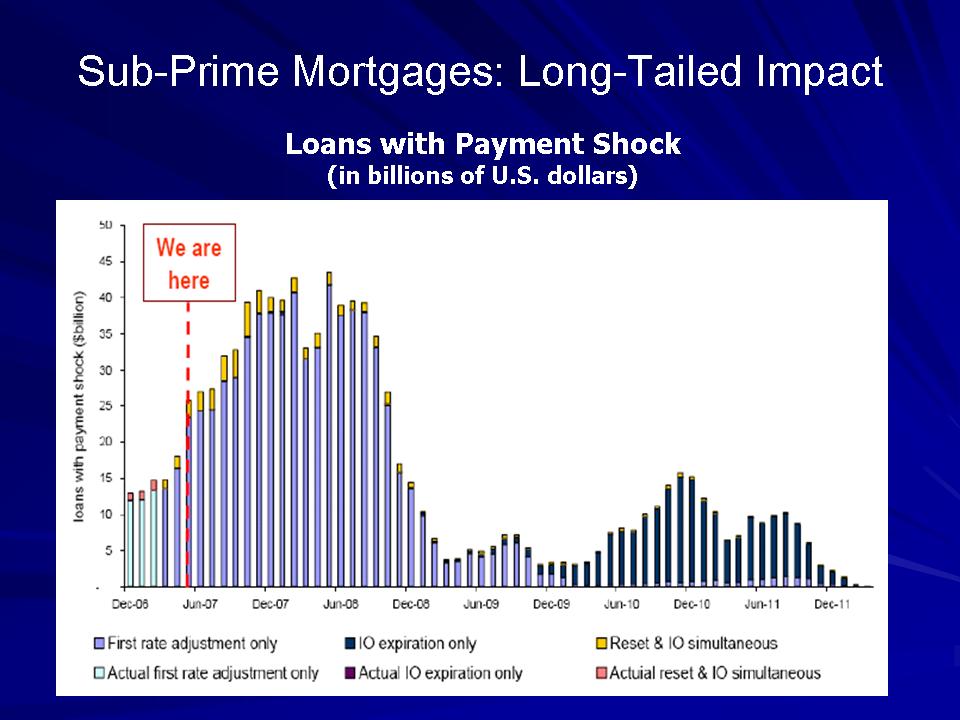

Slide 10: Sub-Prime Mortgages: Long Tailed Impact

{kind=link}

Moreover, an examination of the characteristics of the existing stock of sub-prime adjustable rate mortgages (ARMs) indicates that the current turmoil is not likely to be short-lived. This is because the calendar of scheduled resets on existing sub-prime ARMs is still increasing, and will not subside for some time to come.

While it is natural to ask "What went wrong?", the characteristics of market discipline being imposed on this new and rapidly growing sector are classic: Market discipline is uncertain in terms of timing, uneven in terms of impact, and messy in application. But, in the end, it tends to be effective.

So long as actual credit woes are by and large confined to the sub—prime ARM sector—a relatively small proportion of the overall mortgage market—the impact on the broader economy likely will be limited. Nonetheless, the problems in this sector are likely to extend for a longer span than anticipated originally by most market participants.

Slide 11: Discipline weakening in Corporate Credit Markets

{kind=link}

Of course, the recent tightening of credit terms in US securities markets has encompassed debt issuance associated with Leveraged Buy Out (or LBO) activity. From 2003 onwards, the net terms of such leveraged loans had favored borrowers. This trend has reversed abruptly.

The post-2003 weakening of credit discipline in the corporate sector also was indicated by a very marked dilution in the covenants placed on corporate sector loans. So-called "covenant-lite" loans totaled around $110 billion during the first half of this year, up from about $30 billion last year and less than $10 billion the year before. This trend has also been reversed—at least for now.

The overall impression created by these developments is that financial market participants had become overly optimistic, and now market discipline is catching up, as it does inevitably.

One likely result, is a possible slowdown in leveraged buy out activity, just as the sub-prime market is likely to dampen housing activity for some time.

{kind=link}

The growth of the market for Collateralized Debt Obligations (or CDOs) played a crucial role in providing capital for the sub-prime mortgage market. The total volume of CDOs outstanding from US-based issuers is estimated to be about $900 billion. Of this, about 17 percent has been created out of sub-prime ARM mortgages, with an average credit quality of BBB. Another 30 percent has been created out of leveraged loans in the form of collateralized loan obligations, or CLOs.

While $ 900 billion in securities isn't insignificant, CDOs do not comprise a very large share of the aggregate value of marketable US financial assets of about $ 46 trillion.

Slide 13: Riskiest Positions Are Held By a Wide Variety of Investors

{kind=link}

In addition to the overall size of the CDO market, their ownership is another relevant issue. It appears that hedge funds own only a relatively small percentage of the CDOs outstanding. However, it is likely that their holdings are relatively concentrated in the riskier "equity" tranches of these securities, and that they comprise a much larger share of hedge fund portfolios than they do of overall securities markets. In fact, one recent market estimate is that about 50 percent of hedge funds' structured credit holdings are in the riskiest equity tranches. While banks and insurance companies hold a larger share of the overall CDO market than do leveraged investors such as hedge funds, the share of such instruments in their overall portfolio remains small.

To sum things up, it appears that hedge funds own a surprisingly low share of CDOs outstanding, but have concentrated a significant proportion of their portfolios in such instruments. The reverse is true for other financial institutions—they have relatively larger shares of the outstanding amount, but such holdings represent a very small share of their overall portfolios, and are much less likely to reflect holdings of the riskier tranches.

The stability implications of this pattern of holdings are obviously mixed. While hedge funds may have small shares of such assets under management, they may account for a larger share of the turnover, and are more at risk. In contrast, traditional investors may be able to absorb any losses in this sector more easily given that these instruments constitute relatively small shares of their portfolios, and are concentrated in the less risky tranches.

Slide 14: CDO Spreads Have Widened

{kind=link}

Reflecting the latest developments in the sub-prime CDO market, some hedge funds appear to have sustained significant losses, in some cases requiring substantial loss provisions by their "parent" companies. Since June 15, when the highly-publicized difficulties of certain hedge funds first became known, spreads have more than doubled on CDOs backed by collateral with an average quality of BBB,

{kind=link}

Taken together, the latest developments carry implications for financial markets, for economic fundamentals, and for government policies.

For markets, the immediate issue to consider is whether the heightened market discipline will be effective or destructive.

While the impact has so far been relatively contained, spillovers to broader markets cannot be ruled out. Two possible channels come to mind: First, investors who relied on the credit ratings on CDOs and CLOs when making investment decisions may question the value of ratings in other markets. Second, the backup in the CLO market is very likely to slow down—if not temporarily halt—leveraged buy-out (LBO) activity. While this could cause worries about equity valuations, such concerns should eventually recede, so long as corporate profitability remains strong. After all, second quarter US corporate profit data once again exceeded consensus expectations.

Another important issue involves the outlook for emerging markets. One potentially positive outcome from the recent surge in cross-border capital flows has been the apparent overcoming of so-called "original sin" in many key emerging markets. For those not acquainted with the term, it was coined not too long ago to symbolize the (allegedly) permanent inability of emerging market countries to have their local currency denominated debt accepted by international investors. Contrary to these earlier claims, international investors increasingly have purchased not only the sovereign debt of numerous emerging market issuers, but that of leading corporate entities, as well. This development has the potential to mitigate an important source of financial and economic instability. After all, the 1997/98 Asian crisis was exacerbated by the large stock of foreign currency denominated debt.

Thus, a pending issue is whether the favorable performance of emerging markets will weather the current strains in credit markets. While the risks should not be ignored, it seems likely that the overcoming of "original sin" reflected improving fundamental developments, and not just a "rising (credit) tide lifting all the boats". Thus, if good policies are maintained, the favorable credit trends should survive the current difficulties.

The so-called "carry trade" has been a source of financial inflows to this region—to New Zealand, most notably, and to a lesser extent, to Australia. It is appropriate to ask whether the latest credit market reversals could cause an abrupt unwinding of these trades. While there have been some signs of this, so long as the global outlook—and the situations in the countries whose currencies tend to be the funding currencies for these trades—remain more or less stable, the fundamental impetus behind these "carry trade" flows will remain in place.

Thus, while it is far too early to reach definitive conclusions regarding the potential impact of the latest market developments on economic fundamentals, the IMF baseline forecast remains favorable, as I indicated at the outset.

Turning to the implications of the latest market developments for economic policy, the recent market gyrations underscore the need to pay close attention to the evolution of new markets. If the application of heightened market discipline has been uneven, it is natural to ask if policy-makers can help these markets function more smoothly. In choosing potential courses of action, however, policy-makers should be careful to work with, rather than against the grain of markets. Policies should not stifle the process of financial innovation, given the very constructive role recent innovations have played in this unprecedented global economic expansion.

Of course, the positive global environment of the past five years has coexisted with record current account imbalances. Policy makers should be vigilant for any signs that a global rebalancing does not take place in a disorderly fashion. Such an outcome would have strong repercussions for both economic growth and for financial markets. As credit markets in the US have started to become unsettled, policy-makers should be reminded of the need to implement measures that bolster global confidence. These include both credible medium-term measures to gradually reduce current account imbalances, and a successful completion of the Doha round of trade talks.

On global imbalances, the IMF is acting with some energy. Beginning last year, we convened a Multilateral Consultation on Global Imbalances. This initiative brought together five principal economies—including China, the euro area, Japan, Saudi Arabia, and the United States—for a series of candid discussions. The goal was to construct a set of medium-term policies that would meet two objectives: To significantly reduce imbalances, while keeping global growth strong. The results to date of this Multilateral Consultation were announced at the IMF's recent Spring Meetings. The five participants agreed that reducing global imbalances is a shared responsibility, and they each volunteered to implement a set of macroeconomic and structural policies that are designed to these objectives. These statements are available on the IMF website, and their implementation will be followed up in regular IMF bilateral and multilateral surveillance.

The IMF also is active in other relevant areas.

We have stepped up our analysis of financial markets and are integrating this more explicitly into our regular macroeconomic analyses. Besides this, we conduct Financial Sector Assessment Programs (FSAPs) of member countries, that focus on the financial sector and its soundness.

We conduct reviews of member countries' relevant standards and codes through our formal reviews (known as ROSCs) to help assess the institutions in our member countries that are at the center of macroeconomic policy management.

The IMF has undertaken new initiatives following the 1997/98 international market and economic strains to enhance transparency through improving the quality and completeness of economic and financial data, and to encourage more complete and prompt disclosure. The Special Data Dissemination Standards (SDDS) established by the Fund has played a key role in improving country reporting standards.

In the interest of strengthening our crisis prevention capabilities, we are developing new liquidity instruments to augment our existing lending facilities. With the global economy performing exceptionally well, and with many countries holding record international reserves, it is an ideal time to improve our defenses against more trying times.

To help keep our governance structure contemporary, we are engaged in a significant effort to make the Fund's membership shares more representative of the on-going changes in the global economy. We are in the process of rebalancing quotas to reflect the changes in the relative economic weights of our member countries. Among other shifts, this will boost the role of the most dynamic economies, and will raise the overall voting share of emerging market countries.

In short, we are actively seeking to sustain the benefits of financial globalization, to preserve a macroeconomic environment of rapid growth and low inflation, and to help ensure that the multilateral financial system continues to contribute to the betterment of all.

Thank you for your attention, and I look forward to your comments and questions.