Loading component...

Challenges and Opportunities from Financial Globalization for Fund Managers and Policy Makers in the Asia-Pacific Region, Remarks by Takatoshi Kato, Deputy Managing Director, IMF

December 12, 2007

As Prepared for Delivery

First, I wish to thank the organizers of this conference for inviting me to participate in this very interesting and important discussion. [Slide 1] We at the IMF have been heavily engaged on issues related to financial globalization, and the increased importance of non-bank market participants and investors has been given considerable prominence in our Global Financial Stability Report. So it is especially gratifying to have the opportunity to share our views with you today.

Against this background, I thought I would focus my remarks today on the cyclical and structural issues that are likely to be directly relevant to fund managers and policy makers in the Asia-Pacific region. [Slide 2] First, I would like to discuss some of the factors that we in the IMF see as important for the continued and successful growth of the asset management industry and financial markets in the region. Second, I would like to discuss the lessons and challenges that the recent financial market turmoil offers to the region.

So let me now turn to my first topic, the significant growth of fund management vehicles in the Asia-Pacific region. [Slide 3] The growth of pension fund assets in the Asia-Pacific region has generally been particularly impressive. In Australia, partly reflecting the mandatory contributions to superannuation funds, fund assets have grown at a 20 percent annual rate during the past five years, reaching about 85 percent of GDP, a level close to that in the United States. Pension funds have also grown significantly in Taiwan Province of China, Hong Kong, Korea, Malaysia, and Singapore, with assets there exceeding 30 percent of GDP in each case. The growth in emerging Asia is undoubtedly linked to rapid economic expansion, high saving rates, as well as mandatory schemes and aging populations. No doubt too, asset growth has reflected the stock market boom that most countries in the region have enjoyed. But with economic growth expected to remain robust in the region, the total assets managed by fund managers are likely to continue to increase at healthy rates.

And with the increase in assets under management, another important trend that we see in the region is a decline in home bias, albeit still with a regional bias. Investors and fund managers are increasingly looking abroad to invest as limits on investment abroad are eased, seeking diversification and reduced portfolio volatility by placing funds in new markets and new asset classes.

And we can observe that, for even the largest pension funds and mutual funds, these initial steps into new markets are often via hedge funds or private equity firms, what are often termed alternative investment vehicles. For example, in Australia, the allocation by pension funds into alternative investments funds has reportedly grown to as much as a quarter of total pension assets. In Japan, allocations to alternative investment funds have also increased with the share of private pension assets reaching about 10-12 percent. 1

As you know there is considerable debate internationally about the extent to which hedge funds and private equity funds should be subject to stricter regulatory and supervisory requirements. This debate has been triggered by a growing recognition of the increased and potentially systemic importance of these entities worldwide. As a consequence, the IMF and others have supported calls for greater transparency for hedge fund investors, their counterparties, and other newer investor groups. Greater transparency would bring several benefits, including improvements in investor protection, and enhanced ability of supervisors to monitor funds to assure financial stability.

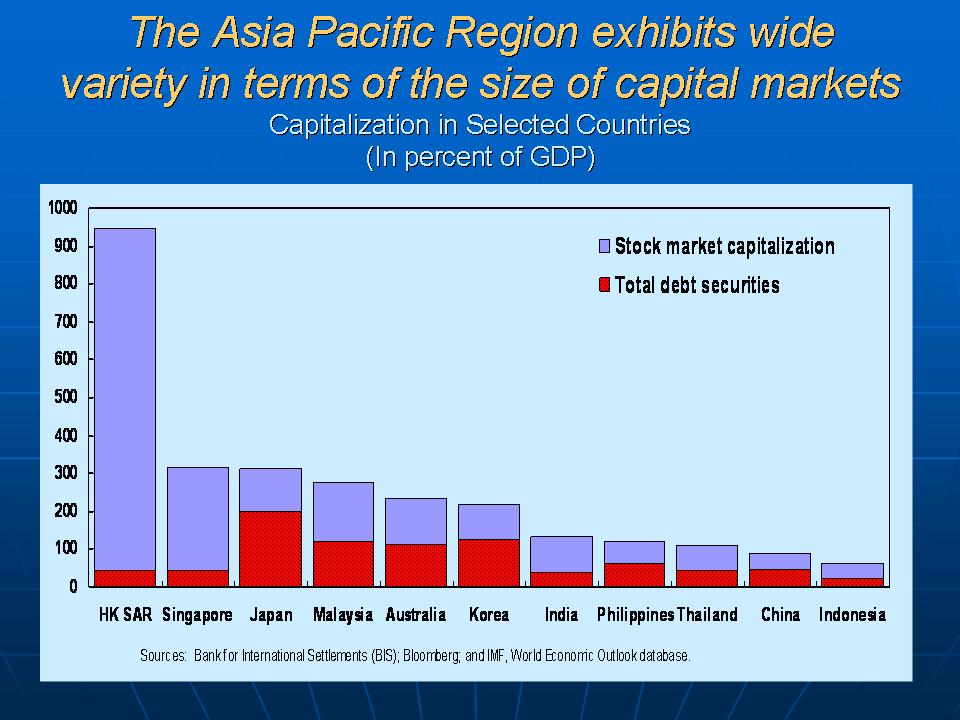

The international portfolio diversification by pension and other funds is linked to the development of capital markets across the region. [Slide 4] There is no doubt that the Asia-Pacific region contains countries that vary widely in terms of the level of depth, liquidity, and sophistication of their capital markets. Australia, Singapore, Hong Kong, and Japan already have advanced markets. But what is impressive is capital markets in Korea, Malaysia, China, Indonesia, the Philippines, and Thailand are also developing very rapidly as these countries reap the benefits of institutional capacity building and other structural reforms and international portfolio diversification.

We at the IMF view as particularly important the efforts that countries in this region have made in improving their investment climate. There is considerable evidence (including as presented in our recent Global Financial Stability Report) to demonstrate that international capital flows are stronger and more stable for countries that clarify and strengthen creditors' rights, corporate governance, investor education, and accounting standards. And there are concomitant benefits that come from improving the financial infrastructure, such as the clearing and settlement process, as well as the supervisory and prudential framework.

We also believe that liberalizing investment limits applicable to domestic institutions, as well as the relaxation or removal of restrictions on foreign investor participation, also improve the stability of investment flows. Of course, an important pre-condition is the establishment of a robust regulatory and supervisory framework, as well as strong risk management capacity within both the private and public sectors. [Slide 5] But once these are in place, and diversification occurs, important benefits accrue, since an expanded and broader investor base helps promote market efficiency, through improved liquidity and price discovery and by providing more stable funding for governments, corporates, and banks. And by attracting more stable capital flows and so-called "real money" investors, emerging and developing economies become less vulnerable to sharp swings capital flows.

Notwithstanding many of the improvements I just cited, I note that the region, like many others, still has further to go in fostering foreign investor participation in local capital markets. These markets still appear to remain relatively under-developed and illiquid, and they can be made more attractive to foreign investors by taking measures to address weaknesses in the informational infrastructure, high trading costs, and limited hedging instruments. [Slide 6] And those countries in the region that are seeking to develop their local bond markets further could draw useful lessons from the experience of the Australian capital markets. The growth and vibrancy of these markets owes much to their openness and the participation of foreign issuers and foreign investors, as well as to the existence of easy access to instruments to allow investors to hedge their foreign exchange and interest-rate risk.

But having extolled the benefits of opening financial markets to foreign investment, I also need to underscore that we are very mindful of the difficulties that this can bring. Indeed, our host country today, Australia, has received heavy capital inflows in recent years, reflecting the effects of carry trade activity, the robustness of its economic growth, and the global commodity boom, and this has resulted in sustained upward pressure on the Australian dollar. [Slide 7] We also see a number of developing and emerging market economies in the region are experiencing a surge in private investment inflows that has been difficult to manage. And in many cases, (e.g. India, Hong Kong SAR, and Vietnam,) these inflows may have outstripped the availability of investible domestic financial assets, leading to sharp increases in asset prices, rapid credit growth, and pressures for currency appreciation.

Of course, policymakers in the Asia-Pacific region—having experienced a financial crisis only 10 years ago—are well aware of the risks and vulnerabilities that stem from potentially volatile global capital flows. [Slide 8] And it is against this background that many developing economies in the Asia-Pacific region have been pragmatic in allowing for a combination of currency appreciation, sterilized intervention (to smooth market volatility), and liberalizing outflows where conditions warrant—as well as pursuing policies designed over the medium term to enhance capacity and infrastructure in their capital markets.

But as we emphasized in our most recent World Economic Outlook, strong trade surpluses and capital inflows are likely to complicate macroeconomic policy implementation. And some countries will also need to be careful in unduly resisting exchange rate adjustments, since exchange rate inflexibility places an even greater burden on policymakers to stem demand and inflation pressures, and adds to the risk of financial and macroeconomic instability.

The growth of pension and other fund management vehicles in the Asia-Pacific region has increased financial sector linkages within and outside the region. These linkages have come to the fore with the recent turmoil in the U.S. sub-prime mortgage market, and it is against this background that I now turn to my second topic today, the lessons for and challenges to world financial markets posed by the recent market turmoil.

This recent episode, which came to the fore last July, has given a clear illustration of how interlinked national and regional financial markets have become. The triggers were relatively localized—a series of ratings downgrades in the US non-prime mortgage market and losses at certain leveraged credit funds. However, their impact has been much wider ranging.

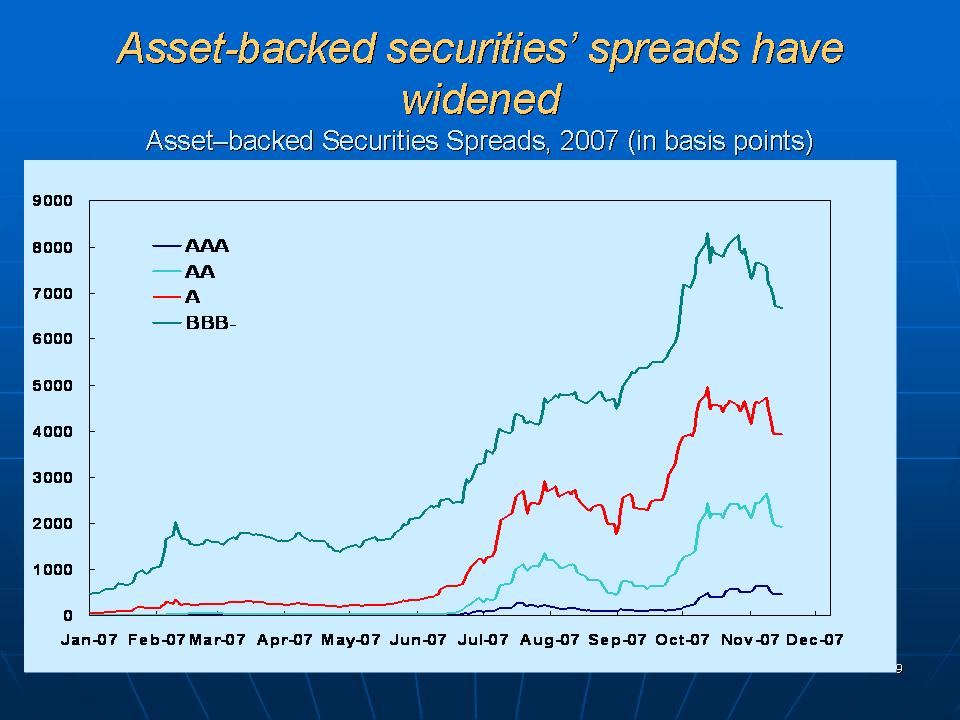

As most of you are already aware, rising U.S. mortgage delinquencies have severely undermined confidence in asset-backed mortgage securities and associated collateralized debt obligations, and this crisis of confidence has spilled over to other types of asset-backed securities. [Slide 9] This lack of confidence has been exacerbated by the illiquidity of these instruments, and the fact that many of them were hard to value and were held off-balance sheet in structured investment vehicles and conduits. The result has been a withdrawal of support for asset-backed commercial paper and curtailed access by banks to interbank markets, as well as a sharp increase in borrowing costs that has forced unprecedented action by central banks to provide liquidity.

The triggers for these events, in most cases, have not been a complete surprise. Many commentators, including the IMF in its Global Financial Stability Report, had long cautioned about the excesses in housing markets, the deterioration in credit discipline, understanding of possible ratings downgrades, and the vulnerability of leveraged instruments to a disruption in liquidity.

But most of us were surprised by the extent to which the effects were transmitted across borders, the degree to which risks remained with banks instead of having been dispersed more broadly, and how badly the shock affected liquidity, including in interbank markets. [Slide 10]

The effects of the turmoil are likely to be protracted and have caused most forecasters—including the IMF—to downgrade their growth projections. I am encouraged, however, by the seeming resilience of most of Asia in the face of this turmoil. To be sure, credit market conditions across the Asia-Pacific region have tightened since the start of the recent market turmoil, and credit spreads have remained higher for longer maturities in jurisdictions like Taiwan and Hong Kong, where banks have typically been heavy investors in U.S. dollar securities. However, local interbank rates in most Asian economies seem to have returned to more normal levels, helped by the willingness of central banks to provide liquidity if needed, especially in Japan and Australia.

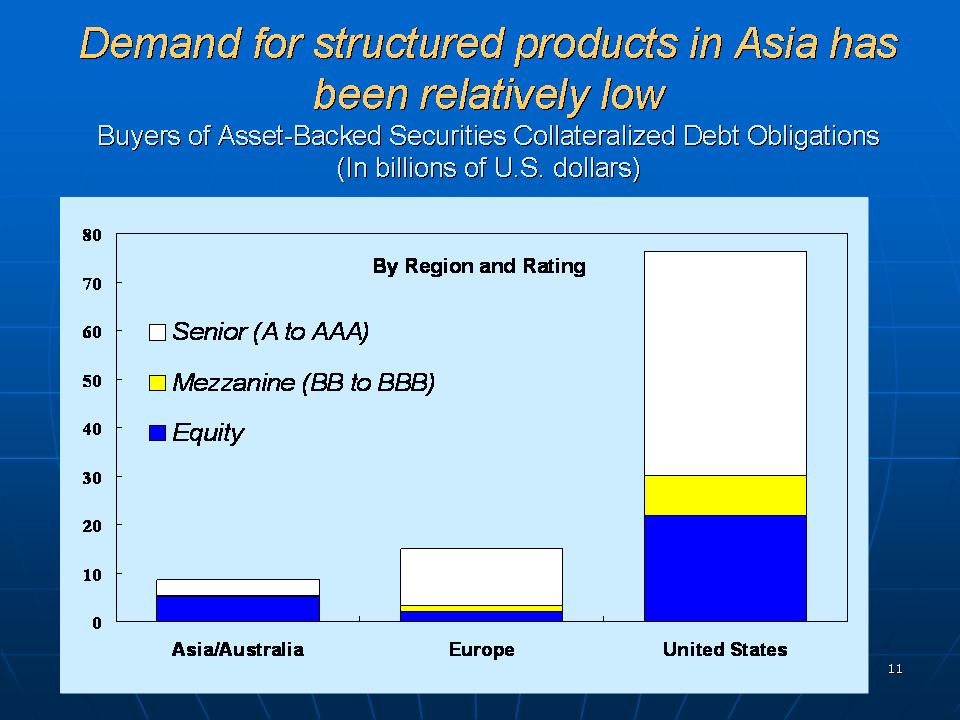

Financial institutions in the Asia-Pacific region also appear to have weathered this recent market turmoil without damaging losses. [Slide 11] Information provided to date by financial institutions in the region points to limited direct losses from the U.S. subprime market and structured debt products.2 However, as experience elsewhere has shown, losses related to recent market turmoil are not always immediately apparent, and supervisors will need to be particularly vigilant in the coming months and be ready to deal with any further turmoil.

Indeed, as we outlined in the IMF's recent Regional Economic Outlook for the Asia-Pacific region, there are a number of macroeconomic and other risks that policy makers will need to watch for. [Slide 12] First, persistent financial market turbulence could lead to a much sharper-than-expected slowdown in both the United States and Europe. And notwithstanding the trade diversification of recent years, it would be pre-mature to suggest that the region has de-coupled, since trade and financial linkages remain significant channels for the transmission of shocks. Second, sustained risk aversion could lead to lower or more selective capital flows to Asia, which will have a negative impact on those countries—in particular where macroeconomic fundamentals and policies are less strong. Finally, oil prices remain very elevated and with capacity still stretched prices remain vulnerable to further spikes, which could dampen activity while posing inflationary pressures.

We believe that this episode offers important lessons, including for the development and management of markets for structured credit products. [Slide 13] There is no doubt that securitization and collateralization of debt has brought tremendous benefits in terms of increasing borrowers' access to credit, and in terms of improving the ability of lenders to manage their risks. However, the rapid development of these new instruments and markets seems to have led to a breakdown in credit discipline and that many participants did not have the appropriate incentives to monitor and manage the risks underlying these instruments.

So what lessons has the IMF drawn from the recent turmoil? I think we need to be humble and recognize that there may not be easy answers. And we also may need to resist the temptation to think that new regulations are necessarily the answer. But even so, we at the IMF believe that national supervisors and regulators need to pay increased attention in several areas:

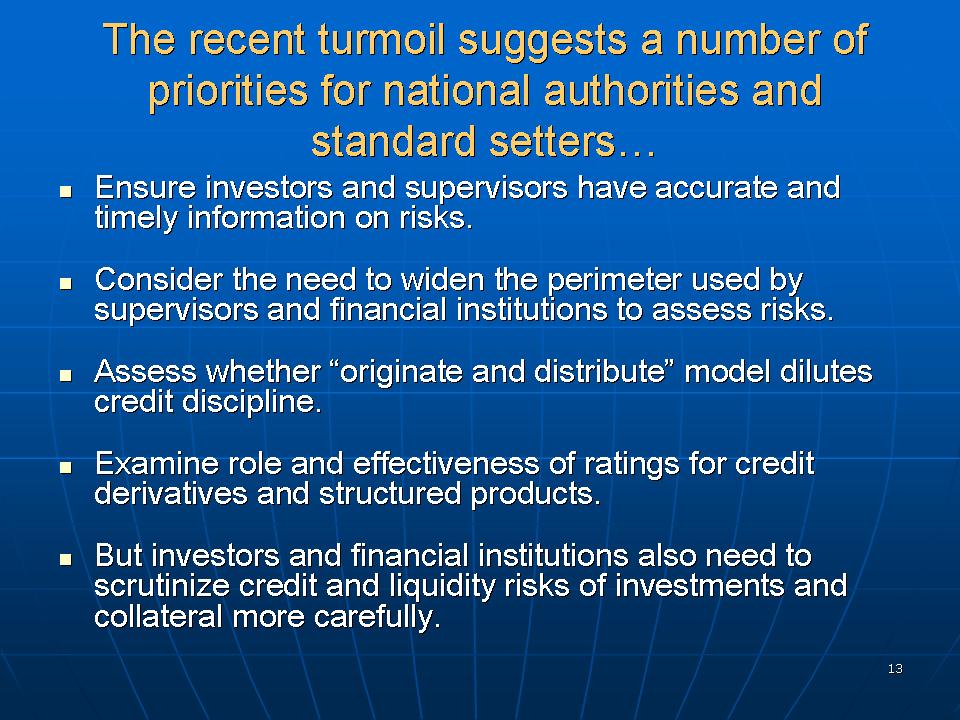

• First, steps are needed to ensure that investors and supervisors have accurate and timely information on the underlying risks to which financial institutions are exposed. Greater transparency is needed of the on- and off-balance sheet exposures of financial institutions, as well as of the interrelationships between asset managers, conduits, and special purpose vehicles.

• This year's experience has shown that the relevant perimeter—for supervisors to consider in gauging systemic risk and for financial institutions' own risk management—may have widened beyond the so-called "core" financial system that is covered by supervisory and regulatory norms. For example, we have seen that reputational risk that forces banks to stand by legally independent entities in the event of their failure. And banks and other regulated entities have sought to use new instruments or independent structures to avoid meeting regulatory capital and other requirements. This widening of the risk perimeter will require greater scrutiny by both supervisors and regulators.

• While securitization and financial innovation have made markets more efficient through enhanced risk distribution, there is a need to assess whether the incentive structure of the "originate and distribute" model may have diluted credit discipline. The experience of the past few years suggests that the checks and balances in the supply chain of structured credit may also need to be re-thought.

• Risk analysis of credit derivatives and structured products by ratings agencies needs to be examined. The rapid downgrades of ratings of these products in recent months have raised questions about the reliability of ratings; whether rating agencies—given their fee structures—are sufficiently independent from originators, and whether different scales need to be applied to structured instruments—given their vulnerability to other risks besides default risk.

• But of course, an important responsibility also lies with investors to exercise appropriate due diligence, and to scrutinize credit and liquidity risks in the instruments they buy, especially for complex products. Financial institutions holding such securities as collateral need robust funding strategies to manage liquidity in stressful conditions. And while regulators need to be mindful of the benefits of financial innovation, every effort is needed to ensure, particularly in fast evolving markets, that investors to maintain high credit and risk management standards.

So against this background what do we see for the Asia-Pacific region in the period ahead? At the most general level, while Asian financial systems are still bank-dominated and relatively conservative, nonbank financial institutions are playing an increasingly important role as financial sectors grow in size and the diversity and complexity of financial instruments increase. As recent events revealed, central banks and supervisory agencies in Asia and elsewhere initially had an incomplete picture of how complex and deep the market for structured debt had become and the vulnerabilities that they implied. And while it may take time to fully appreciate the implications of the recent episode, I do believe that policy makers and market participants, including in the Asia-Pacific region, can already draw some important lessons, some of which I hope I have laid out for you today.

At the IMF, our work has evolved to allow us to better understand these developments and financial interlinkages and to be better able to assist our member countries in meeting the related challenges ahead, in coordination with other standard setters and the Financial Stability Forum. In this regard, we recently improved our monitoring of economic and financial conditions in our member countries to include more in-depth analysis of global financial markets and multilateral surveillance to assure economic and financial stability. Better monitoring, together with our work on local capital market development, has become a key priority for the IMF, and we are seeking to assist our members in these efforts.

Thank you again for inviting me to participate in this conference and for allowing me to share some of our thoughts regarding the challenges and opportunities for fund managers and policy makers in today's global financial markets.

1 Asian hedge funds generally fared well in recent years, given a tendency to invest in the region, and have continued to perform well even in the face of the recent market turbulence. The recent favorable performance reportedly reflects less complex trading strategies, movement toward cash positions as a precautionary measure, and lower leverage levels. The fact that Asian hedge funds have mostly been operating from Hong Kong and Singapore also means that they have benefited from the strength of their regulatory and supervisory systems.

2 This limited exposure may reflect that many Asian financial institutions are traditionally more conservative compared with their counterparts in other parts of the world, and therefore, less likely to purchase these products. Also, the relatively high domestic yields in some countries in the region may have lessened the need to search for better yields through investments elsewhere.

| Public Affairs | Media Relations | |||

|---|---|---|---|---|

| E-mail: | publicaffairs@imf.org | E-mail: | media@imf.org | |

| Fax: | 202-623-6220 | Phone: | 202-623-7100 | |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}