Loading component...

The Role of Policies to Foster Oil Sector Investment in a Global Context, Remarks by John Lipsky, First Deputy Managing Director, IMF

April 21, 2008

As Prepared for Delivery

| Download the presentation (820 kb PDF) |

1. Good afternoon. It is a great pleasure to participate in this forum. My remarks today will focus on ways in which the international community can foster investment in the oil sector-an issue that has taken on new urgency in light of the increasingly adverse impact of rapidly rising commodity prices.

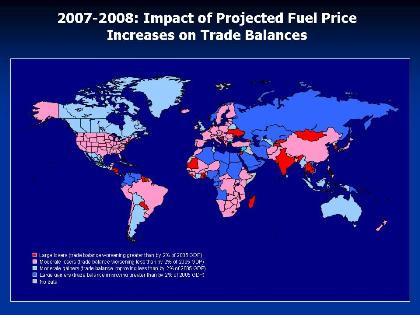

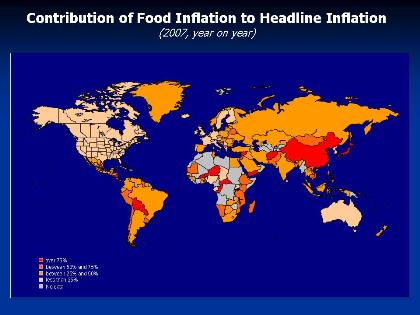

2. Let me begin by discussing the macroeconomic implications of the broad-based commodity price boom that is currently underway. To put this into context, oil prices have increased by about $40 per barrel from their 2007 average, which, according to IMF estimates, would by itself reduce annual global growth in 2008 by between ½ and 1 percentage point if the increase were sustained during the remainder of the year. More broadly, surging commodity prices are affecting budgets, trade balances, headline inflation, and, of course, standards of living almost everywhere.

3. Overall, commodity prices, especially those for foods and energy, have now reached levels where they risk becoming a destabilizing force in the global economy. This is a global problem that requires a globally coherent response. National policy decisions must be viewed in a multilateral context. Two examples of the unfortunate international consequences of actions directed at domestic markets are the price spillovers that have resulted from the recent tightening of export restrictions by major rice exporters and from subsidies and protectionist barriers aimed at stimulating the production of biofuels.

4. Another important dimension is the need to achieve a stronger supply response to rising prices. This brings me to the topic of this session-how to foster investment in the oil sector. Policies aimed at improving investment in the oil sector have taken on new urgency. Oil is a critical input at every stage of the production and distribution of goods and other commodities. Thus, measures to increase the supply of oil and improve stability in oil markets should have a salutary effect on other commodity prices as well as the global economy more broadly.

Current Conditions in Oil Markets

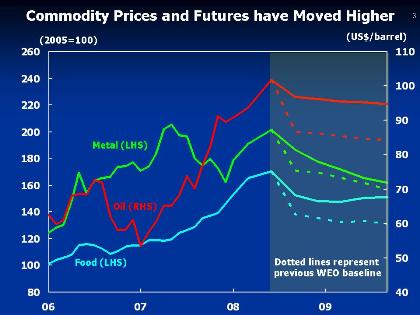

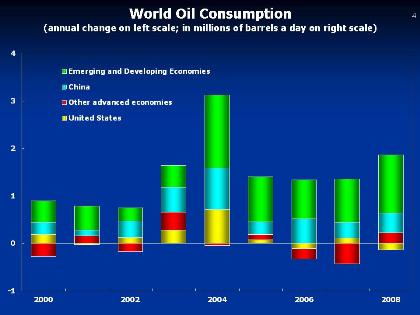

5. The sharp surge in oil prices since the beginning of 2007, on top of substantial increases since 2002, has been a wake-up call for public officials and market participants. With global growth slowing, markets expected oil prices to decline below $80 per barrel as late as October of last year. Instead, prices have continued to surge to over $115 per barrel, as after almost two decades of substantial spare capacity, demand has fully caught up with production capacity. While advanced economies are now slowing, emerging market economies have been the main drivers of demand growth, with China, India, and the Middle East alone accounting for almost two thirds of the growth in oil consumption over much of the past decade. So even as the global economy slows by over one percentage point in 2008, we expect oil demand from emerging markets to continue growing at a robust pace.

6. While oil demand has remained robust, the supply side response to rising prices has been disappointing. Supply projections have routinely been revised downward in recent years, particularly for non-OPEC oil producers, including Mexico, Russia, and the United Kingdom. As buffers have dwindled, the oil market has become highly sensitive to news of supply disruptions or geopolitical events.

7. This year, financial factors also appear to have boosted oil prices. The combination of U.S. dollar depreciation, falling short-term interest rates, and disruptions in global credit markets have further strengthened already growing investor interest in oil and other commodities as an alternative asset class. Indeed, inflows into commodity funds and assets have risen markedly in the first quarter of 2008, in a classic investor response, as investors typically buy assets whose price is rising.

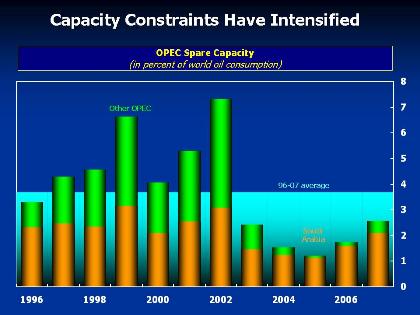

8. Looking forward, we expect oil prices to ease modestly as the global economy slows. But the expected declines would only partially reverse the significant cumulative price increases we have seen over the past few years and oil prices would remain around $95 per barrel in 2009. Fundamentally, oil prices are likely to stay at high levels because market conditions are likely to remain tight. In fact, OPEC spare capacity is now about half of its 1996-2007 average level and about one-quarter of its 2002 level and is expected to remain limited for some time.

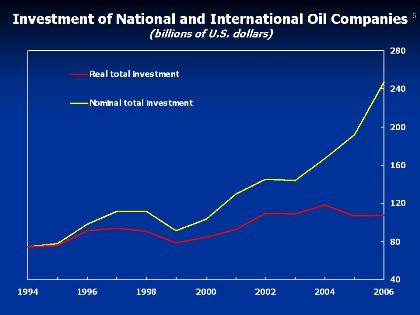

9. Against this background, increased investment in the oil sector has a crucial role to play in improving the supply-demand balance and bringing greater stability to the market. In recent years, capital expenditures have begun to rise more rapidly, as one would have expected, given price developments. However, research by IMF staff shows that this has translated into only modest increases in capacity. Specifically, while nominal oil investment grew by about 60 percent during 2002-06, in real terms investment remained broadly unchanged over this period.

Explaining the Sluggish Investment Response

10. What explains the sluggish real investment response? In short, investment has been constrained by a confluence of cyclical, technological, geological, and policy factors. Turning first to cyclical factors, exploration and development costs have skyrocketed, reflecting in part sector-specific capacity constraints in oil services and other inputs after a 15 to 20-year period of low net investment and stagnating capacity. General capacity constraints associated with the exceptionally strong global expansion and broad-based commodity boom of the past few years have only added to cost pressures. Higher costs imply that less of the higher capital expenditure in current dollars translate in actual capacity additions.

11. Other cost increases are related to technology and geology. As the U.S. National Petroleum Council has noted, new oil fields are smaller in size and involve greater technological and geological challenges, while the decline rates of existing fields in key regions may be higher than earlier estimated. This means development and exploration costs per barrel in new fields are higher in constant dollar terms than they were when older fields were developed-market estimates suggest that average field exploration and development costs have doubled, from $5 a barrel in 2000 to $10 a barrel in 2007, while these costs for marginal fields are now closer to $20 a barrel. Moreover, a greater share of overall investment goes into maintaining production in maturing fields, and the share adding to overall capacity is smaller.

12. Recent IMF studies on oil investment also highlight some policy factors behind the sluggish investment response.

Policy Challenges

13. This brings me to the policy challenges related to oil investment. As in other commodity markets, a fundamental policy objective must be to foster sustainable supply-demand balances by strengthening the frameworks needed for market forces to operate properly. In this regard, it will be essential to allow oil prices to play their signaling role to influence both supply and demand. I believe there are four central lessons from our analysis.

Concluding Remarks

14. Let me conclude by emphasizing the urgency of policy actions in the area of oil investment, not only for stability in oil markets, but also for stability in the global economy. Oil markets are linked to most industries, and affect all households and all countries. Oil market conditions and policies-as well as those for other commodities-must therefore be considered in a global context. The supply response can be enhanced by improving the stability and predictability of investment regimes, encouraging greater cooperation between national and international oil companies, and increasing transparency through better oil market data. For consumers, policies should aim to achieve full pass-through of international oil prices to domestic prices and to signal environmental costs. Actions are most likely to be successful if undertaken in a multilateral context where everyone does their share to improve the supply-demand balance in oil markets, which in turn would make these markets less vulnerable to shocks and therefore more stable. A more stable oil market is critical to attaining a more stable global economy.

| Public Affairs | Media Relations | |||

|---|---|---|---|---|

| E-mail: | publicaffairs@imf.org | E-mail: | media@imf.org | |

| Fax: | 202-623-6220 | Phone: | 202-623-7100 | |