Presentation to the Central Bank Governors of ASEAN, Asean+3 Meetings by Mr. Naoyuki Shinohara, Deputy Managing Director

Bali, Indonesia, April 7, 20111. Good morning. It is a real pleasure for me to address the ASEAN constituency this morning.

2. I would like to cover three broad points in my presentation [Slide 1]. After discussing briefly the global economic setting, I will focus on the outlook for ASEAN economies and major risks. Some of these risks are relatively new and difficult to quantify, as they are associated with the recent tragic events in Japan and the geopolitical tensions that have surfaced in the Middle East and North Africa. I will then offer our views on the resulting policy challenges for the region. Lastly, I will touch upon the role of the IMF in the reform and strengthening of the international monetary system.

3. Now, the global economic outlook. So far, the global economic recovery has evolved broadly as we anticipated and financial conditions have continued to improve. While we expect the emerging economies of East Asia to continue to grow at healthy rates they will have to navigate opposing risks: growing domestic overheating pressures on the one hand, and downside risks on the global economy on the other, in particular from higher oil prices, and remaining financial and fiscal vulnerabilities in advanced economies. The devastating earthquake and tsunami in Japan has also cast a pall over the regional outlook, given the close trade and financial linkages between Japan and the rest of the region. Over the longer term, the main challenge for Asian economies remains to achieve a more balanced and inclusive pattern of growth.

4. Our global economic outlook is broadly unchanged from the January World Economic Outlook or WEO update [Slide 2]. After a slowdown in the second half of 2010, economic activity has picked up again toward the end of 2010 in both advanced and emerging economies. More recently, industrial production, manufacturing PMIs and retail sales all suggest that economic activity is likely to consolidate further in several advanced economies, particularly the United States, and to remain strong in emerging economies. As a result, we see global growth reaching about 4½ percent in 2011 and 2012, with real GDP in emerging and developing economies expanding at 6½ percent, whereas growth in advanced economies would only be about 2½ percent. Asia is expected to remain the fastest-growing region in the world, and by far the single largest contributor to global growth, although after the strong rebound in 2010, the expansion will proceed at a more sustainable pace of slightly less than 7 percent.

5. Inflationary pressures are projected to broaden, but mainly in emerging and developing economies, reflecting the differences in growth patterns. Globally, headline inflation picked up to over 3½ percent in December, approaching 2 percent in advanced economies and exceeding 6 percent in emerging and developing economies. Thus far, rising inflation in emerging and developing economies mainly reflects the behavior of food and energy prices, which have a higher weight in consumer baskets in these economies. However, looking ahead, we expect core inflation in emerging economies to rise as well as excess capacity to diminish.

6. Overall, our forecasts assume that macroeconomic policies generally remain expansionary at the global level. The concerns that the global recovery might be set back by fiscal tightening in advanced economies have weakened. In fact, with fiscal deficits in advanced economies expected to remain as high as 7 percent of GDP in 2011, the withdrawal of fiscal stimulus in advanced economies now appears fairly limited, at only about ¼ percent of GDP, compared with a withdrawal of about 1 percent of GDP anticipated in the October WEO. Macroeconomic policies are also expected to remain stimulative in many emerging and developing economies, despite their cyclical positions.

7. Risks in advanced economies have receded somewhat, but remain on the downside. Many of these risks are not new [Slide 3]. Weak banks and sovereign balance sheets (particularly in some euro area economies) and still moribund real estate markets, especially in the U.S., continue to present major concerns. Fortunately, the policy response of the Spanish authorities has been strong, particularly with respect to the banking sector, and pension reforms. As a result, market pressure has eased, but spreads remain high and we are not yet out of the woods. The situation requires careful monitoring. In these circumstances, a key risk is renewed turbulence in advanced sovereign debt markets, which could be triggered by unsuccessful sovereign or bank debt rollovers, or lack of successful fiscal consolidation, and could interrupt the transition toward stronger private-led demand. Together with heightened global risk aversion, a stall in advanced economies’ recovery would quickly spread to developing and emerging economies, through both real and financial channels. Meanwhile, many emerging economies face the very different risk that the present overheating pressures could turn into boom-bust cycles in the coming years. In addition to domestic demand pressures, higher-than-anticipated petroleum prices (the WEO baseline has already been revised up from $79 per barrel in October 2010 to over $100 per barrel) would exert additional upward pressures on prices.

8. Against this global backdrop, what is our outlook for Asia and the ASEAN economies? [Slide 4] Asia entered 2011 with strong economic momentum, thanks both to domestic demand and exports. However, while we expect the pace of growth to reach about 7 percent for the region as a whole, unchanged from our October 2010 Regional Economic Outlook, we expect marked differences of economic performance across the region.

9. In Japan, growth is expected to moderate from almost 4 percent in 2010 to perhaps 1½ percent in 2011 and about 2 percent in 2012 as reconstruction spending will increasingly offset the negative impact of the disruption caused by the earthquake and tsunami. In our baseline scenario, we expect that economic spillovers from the natural disaster in Japan to the rest of the region are likely to be modest as import demand will rebound as the rebuilding process gets under way, while a drawdown of inventories and a switch to alternative suppliers should act as a buffer for temporary disruptions of Japanese supply to regional production networks.

10. In emerging Asia, growth is projected at around 8 percent in 2011 and 2012, close to our estimates of potential output and only slightly below the 8½ percent average growth rate during the five years of rapid economic expansion preceding the global financial crisis. China and India are expected to again lead the rest of the region. In China, growth is expected to moderate from 10¼ percent in 2010 to 9½ percent over 2011 to 2012, as policy tightening slows investment. In Indonesia, growth is expected to remain on an upward trend, from 6 percent in 2010 to 6½ percent in 2012 as continued robust public and private investment provides a boost to economic potential. Meanwhile, in most other emerging Asian economies, growth in 2011 and 2012 is projected to moderate from the cyclical peaks in 2010 toward potential rates that, on average, are slightly lower than pre-crisis potential growth, mainly on account of more subdued post-crisis growth in advanced economies.

11. As for developing Asia, the growth outlook also remains favorable on the back of strong commodity exports and robust investment in the energy and mining sector, as for example in Lao PDR, reflecting its expanding hydro-power and copper production, and the ongoing recovery in textile exports, as in Bangladesh, and tourism, as in Cambodia. We also see a favorable growth outlook for Vietnam, provided that the recently adopted stabilization package is implemented in a decisive and sustained way to restore policy credibility, and domestic and foreign investor confidence.

12. This favorable outlook is underpinned by continued robust exports on the back of the strong recovery in investment, and healthy demand for consumer durables both in advanced and emerging market economies [Slide 5]. Healthy corporate profits and balance sheets, coupled with easy financing conditions, have produced a sharp turnaround of the investment cycle in advanced economies. This has benefited Asia in particular, as transport and machinery equipment accounts for about 60 percent of overall Asian exports. While U.S. investment is expected to expand at a double-digit rate in the coming quarters, Asia is likely to benefit also from the strong investment cycle in emerging markets and developing economies.

13. In part related to the favorable export outlook, domestic demand should also remain robust. With firms already operating close to capacity in several regional economies, the need to maintain and add to the capital stock will sustain investment, including in Indonesia and the Philippines. Moreover, the need for building or upgrading infrastructure is likely to add to investment demand, including in many ASEAN economies, India, and, reflecting the reconstruction after the earthquake and tsunami in Japan.

14. At the same time, private consumption will be supported by the strength in employment and wages. A combination of tight labor markets, strong productivity growth and policy measures to boost household income, including in China, Indonesia, and Thailand, mean that nominal wages are likely to continue to outpace inflation, providing a further boost to real disposable income and consumption.

15. Overall, the risks to the outlook appear somewhat more balanced than they were at our last forecasting round in October 2010 [Slide 6]. Concerns about the sustainability of private domestic demand in advanced economies have moderated, and there may even be upside risks to Asia’s export dynamics from a stronger global recovery. Nevertheless, an escalation of financial tensions in the euro area would greatly affect Asia through the trade channel, given that the region’s trade exposure to Europe is at least as large as that to the United States.

16. Meanwhile, new downside risks to growth have emerged for the region. First, the turmoil in the Middle East and North Africa threatens to result in further spikes in oil prices. This in turn could intensify inflation concerns, including in many ASEAN economies, and pose risks to global growth. The direct impact of higher oil prices on growth and inflation is likely to vary across Asia. For those economies that are less dependent on oil imports, such as China or Japan, staff estimates suggest that an increase of oil prices to $150 per barrel in 2011 would shave about ½ percentage points off annual GDP growth. However, given their high dependence on external demand and manufacturing exports, most Asian economies, regardless of their level of development, could be severely affected if second round effects from higher oil prices resulted in a global slowdown, even in the case of net oil exporters, such as Malaysia.

17. Second, there is also a risk of greater-than-expected spillovers from the natural disaster in Japan [Slide 7], although financial market indicators suggest some moderation in perceived risks. To begin with, the need to replace or at least supplement nuclear power, which represents about 30 percent of Japanese energy supply, and the reconstruction could pose further upward pressure on global commodity prices. Moreover, a prolonged disruption in production and transportation facilities could have a larger impact on regional production networks than anticipated in our baseline. Staff estimates suggest that countries particularly exposed in ASEAN, due to strong outsourcing links and thus a relatively large share of intermediate inputs from Japan, include Thailand, Malaysia, and Singapore.

18. Turning to risks within emerging Asia, including a number of ASEAN economies, pressures from potential overheating in goods and asset markets are on the rise. While output gaps are expected to be closed for many regional economies this year, headline inflation has accelerated since October 2010 [Slide 8]. To a large extent this is owing to higher commodity prices and so the degree of accelerating inflation also differs widely across the region. In particular, economies with a relatively high weight of food and energy prices in the CPI index, such as Indonesia and Vietnam, are experiencing relatively higher inflation. However, higher commodity prices also appear to have spilled over to a more generalized increase in prices. Since October 2010, core inflation has risen by about ½ percentage points in Asia as whole, but increases have tended to be higher for economies operating closer to full capacity, such as Singapore and Vietnam. Inflation expectations are also on the rise in many ASEAN economies.

19. Against this background, we expect headline inflation to rise further in 2011 before moderating somewhat in 2012. Global food and energy price inflation, at about 20-30 percent under current WEO projections, will add to inflationary pressures in the region, especially where general demand pressures are already high and output gaps have closed. Accordingly, staff estimates for 2011 point to a pick-up in inflation in the Philippines, while inflation may be above or close to the upper ranges of targets in Indonesia, Korea, and Thailand. However, further oil price increases could significantly add to inflation pressures, in particular in lower income ASEAN economies, where electricity generation tends to be more reliant on fossil fuels. In addition, related items, such as food and transportation, typically make up a large share of consumption, and the ability of governments to stabilize prices through subsidies is more limited.

20. Pressures from capital inflows have generally moderated somewhat since last fall [Slide 9]. In the fourth quarter of 2010, net capital inflows to emerging Asia as a whole declined to about 1 percent of GDP, compared with the recent high of 4 percent of GDP in mid 2009. However, there is significant cross-country variation and some economies, including Indonesia, the Philippines and Thailand, have continued to experience relatively large inflows. Nevertheless, capital flow volatility remains a significant risk in a number of regional economies. With inflows closely related to global financial conditions, sovereign and banking sector risks in the euro area, or a stronger than expected recovery and earlier start of the tightening cycle in advanced economies could all cause more volatility in capital flows. Among the ASEAN economies, more volatile capital flows are a particular risk for economies with large current account deficits, such as Vietnam, or a relatively high share of foreign participation in securities markets, including in Indonesia and Malaysia.

21. As with capital flows, risks from overheating in asset markets are not generalized, but show signs of intensifying in a few regional economies. There is little evidence that equity and bond valuations are out of the ordinary, especially after some moderation since the beginning of the year, which may have been induced by concerns that a further pick-up of inflationary pressures prompts more forceful monetary tightening.

22. Nevertheless, turning to domestic intermediation, there are signs that overheating pressures are building up as credit growth has accelerated strongly in several ASEAN economies, including Indonesia and Thailand [Slide 10]. From a longer-term perspective, credit dynamics in China are particularly concerning, as the cyclical component of the credit-to-GDP ratio at the end of 2010 was substantially above its historical average –– an indication of a credit “boom”.

Policy Challenges23. Let me now turn to the policy challenges facing the region. Overall, our sense is that the need to tighten macroeconomic policies has become more pressing than it was six months ago. Many economies already began tightening in 2010, but the process has generally been slow, perhaps reflecting doubts about the strength of the global recovery and about private domestic demand in the region. Nevertheless, with the global recovery firming and supply constraints emerging in Asia, it is now time for a few economies to step up the pace and size of adjustment.

24. For those economies with generalized overheating pressures, further monetary tightening seems warranted [Slide 11]. Staff estimates of Taylor rules suggest that policy rates have increased more slowly than in the past for a number of regional economies. In particular in the cases of Indonesia and Thailand, they seem below what is indicated by these countries’ outlook for inflation and growth. Moreover, real policy rates are sill negative in a number of countries, including the Philippines and Thailand, which, if sustained, could contribute to financial instability, through deterioration in the allocation of investment capital, higher leverage and asset price bubbles.

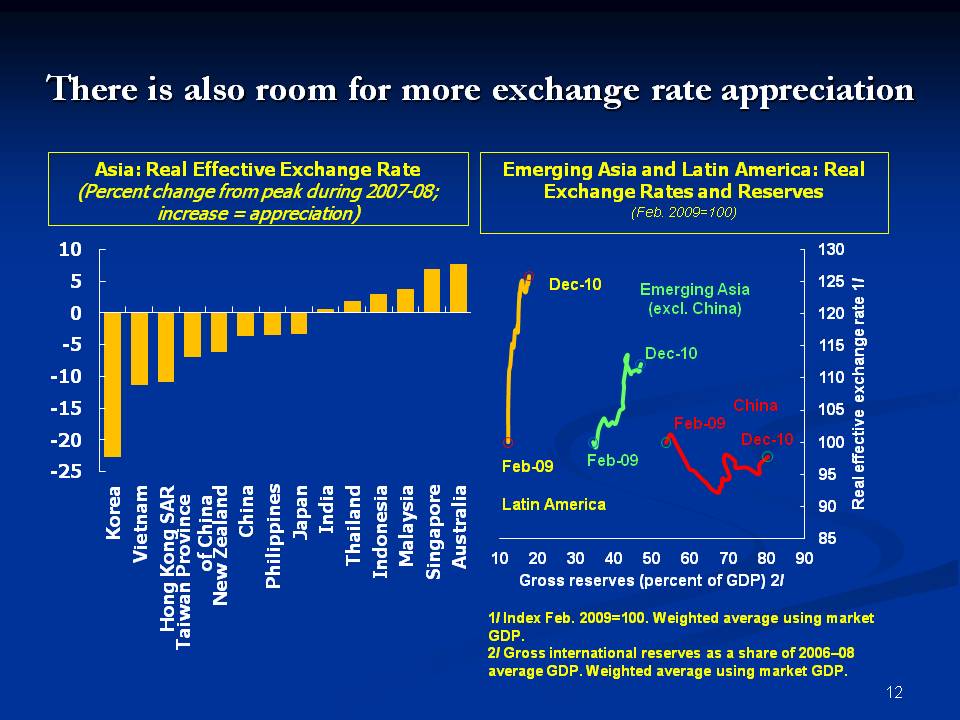

25. Further exchange rate appreciation can also play an important role to avoid overheating [Slide 12]. It could help reduce the burden otherwise to be borne by interest rate tightening. Despite the recent appreciation of regional currencies, real effective exchange rates remain close to pre-crisis levels in many emerging Asian economies, such as in Korea, China, and the Philippines. At the same time, strong current account surpluses across the region continue to be a more important source of excess demand, and reserve accumulation, than net capital inflows.

26. Let me briefly add that receding pressures from capital inflows imply greater room for monetary and exchange rate tightening. Yet, in economies where large capital inflows still threaten to complicate monetary policy tightening, macro-prudential measures can be a useful complement in addressing specific financial vulnerabilities.

27. There is also room for further fiscal tightening in the region [Slide 13]. The pace of consolidation has differed substantially across Asia, and in a few economies, such as Indonesia and Singapore, estimates suggest that fiscal policy in 2011 would even add stimulus. Generally, cyclically-adjusted fiscal balances show higher deficits or smaller surpluses relative to a five-year average preceding the crisis. However, fiscal consolidation would increase the scope for governments to respond effectively to potential future shocks. Moreover, in a number of countries, governments have adopted anti-inflation measures with significant fiscal cost to buffet the impact of higher food and oil prices which may only have a temporary impact on inflation and may delay a desirable supply and demand response to alleviate relative shortages. Fiscal consolidation is also warranted in a number of lower income ASEAN economies. However in these cases, such as Cambodia or Lao PDR, the key will be to enhance fiscal revenue as over the longer term this would also help to create fiscal space for much needed development spending.

28. Turning to medium-term challenges, we believe that the main challenge remains to achieve more balanced growth and also to make growth more equitable and inclusive [Slide 14]. As I mentioned earlier, the outlook for Asian exports is strong, and, in fact, we project gross exports to contribute more than private domestic demand to growth in 2011 and 2012. As a result, the projected evolution of current account surpluses across Asia, including the NIEs, many ASEAN economies, and China, suggest that global demand rebalancing may be slow. The persistence of these imbalances suggests that many of the distortions that characterized the pre-crisis period remain at play, including exchange rate misalignments, impediments to private investment or high precautionary savings. Implementing comprehensive policy packages, including structural reform, to strengthen domestic demand in the Asia region will thus remain important to facilitate economic rebalancing. This, I should add, is not inconsistent with the need to tighten macro-policies from a cyclical point of view in order to deal with overheating risks. Fiscal policies to strengthen social safety nets and boost private consumption or to increase public investment would certainly add to overheating pressures in the near term, but they could be offset by savings in non-priority current spending. Also, exchange rate appreciation could support both countercyclical policy tightening and rebalancing toward internal demand.

29. Before concluding, I would also like to briefly update you on the role of the Fund in bringing about a more balanced and sustained global recovery and in strengthening the international monetary system. We see four issues that must be addressed [Slide 15]. These are strengthening the global adjustment mechanism to deal with imbalances; developing a framework to deal with volatile capital flows; enhancing access to global liquidity to provide a safety net to countries and to reduce the need for self-insurance; and meeting the needs for safe global reserve assets. Since we are pursuing a continuous dialogue on these questions with all our members, including in Asia, and I have updated many of you at the recent South East Asian Central Banker’s meeting in Sri Lanka, allow me just to highlight a few areas on which work at the Fund has focused on in recent months.

30. One of the key lessons of the crisis is that strong policy coordination is important in addressing weaknesses in the global financial system. But there is a lack of clear agreement on an effective global adjustment mechanism to deal with imbalances. The initiatives of the G-20 countries are underway, namely the Mutual Adjustment Process (MAP). But this process must be continued. The agreement on “indicators” at the Ministerial meeting in February was encouraging. The next steps are to develop actual assessment guidelines and to agree to use them. This will not be easy. More generally, the IMF has to continue working to strengthen its surveillance. One of the weaknesses of the international monetary system is that, except for exchange rate policies, countries have no obligation to conduct their domestic policies in ways consistent with systemic stability. To address this, the IMF has launched experimental “spillover reports.” We expect to complete soon five pilot cases of spillover reports that analyze the international impact of policies adopted by systemically important countries or currency areas, such as the United States, Euro area, United Kingdom (as a global financial center), Japan, and China. This exercise will allow us to increase our focus on the impact of countries’ policies across their borders, and allow policymakers to voice their concerns about the impact of other countries’ policies.

31. Such spillover reports will also provide the opportunity for a more even-handed approach to multilateral surveillance. For instance, capital flows may not only be analyzed as an issue for recipient emerging market economies, but also in relation to policies in systemically important advanced economies. In addition to enhancing our multilateral surveillance toolkit, we are also strengthening bilateral surveillance through increased attention to financial issues, including by a deeper integration of financial stability assessments, or FSAPs, into our regular country surveillance reports.

32. Regarding capital flows, it should at the outset be pointed out that this is not just an issue for emerging markets. In fact, the largest capital flows are among advanced countries, so the implications of these flows are for all countries to worry about. The Fund has intensified its research on the determinants and appropriate policy responses to capital flows, and discussions are ongoing on providing member countries with a framework distilled from the recent experiences. We had the opportunity to discuss some of this work with members in the region during a recent joint Bank Indonesia IMF conference here in Bali.

33. Further, at a recent discussion of this issue at the IMF Executive Board, there was broad support for developing a framework to guide policy actions to address volatile capital flows. But our members stressed the following key points. First, a comprehensive and balanced approach to capital flows is required that takes into account both capital recipients and capital originators. Second, policy advice on managing capital flows should be even-handed and pay due regard to country-specific circumstances and the external setting. Third, flexibility is important and there is a broad spectrum of instruments in the policy toolkit to manage inflows, aside from macroeconomic policies and structural measures. So-called capital flow management measures (CFMs) encompassing prudential, administrative, and tax measures are squarely within the toolkit. While in general CFMs should not be used as a substitute for necessary macroeconomic adjustment, there are circumstances when they could be used simultaneously with macroeconomic measures. So the work is in progress on formulating a framework to help countries better cope with volatile flows.

34. Regarding global safety nets, since the onset of the global financial crisis, we have come a long way in strengthening our financial safety nets. Not only has the IMF increased the amount of resources at its disposal but we have created many new and more flexible instruments, such as the Flexible Credit Line and the Precautionary Credit Line, to support countries in times of liquidity needs. However, many countries consider that there is a need to further enhance financial safety nets. An important aspect of our work is to address gaps in the Fund’s crisis-resolution toolkit, which would meet the short-term liquidity needs during systemic crises, or including by adopting new facilities. For example, we are exploring a systemic crisis-prevention mechanism, which would specifically mitigate contagion by being deployed simultaneously to a group of Fund members. We will also explore how to strengthen partnerships with regional initiatives, such as Chiang Mai, to enhance financial safety nets.

35. Finally, as financial deepening proceeds in emerging markets and the supply of global financial assets become more diversified across countries, we should expect a more multi-polar system to emerge with several currencies playing a key role globally. Over time, there may also be a role for the SDR to contribute to the stability of the international monetary system. As a first step, adding emerging market currencies to the SDR basket could help internationalize these currencies. In the long run, we may also need to explore the scope for increasing the stock of SDRS to meet the demand for precautionary reserves, or using the SDR to price global trade and denominate financial assets, such as SDR-denominated bonds. A number of technical hurdles would, however, need to be addressed to move in this direction, including an enhancement of international policy coordination. Let me say that we should study these issues with an open mind, as the evolution of the system will necessarily be gradual and the choice of reserve assets will inevitably be a market decision.

Conclusion

36. Summing up, let me say that so far, the global economic recovery has evolved broadly as expected while global financial conditions have improved [Slide 16]. Against this, the near-term growth outlook for Asia remains quite favorable. However, new risks are on the horizon, which may be difficult to quantify, notably a potential spike in oil prices related to turmoil in the Middle East and Africa, and the uncertainty following the devastating earthquake and tsunami in Japan. Nevertheless, Asia’s rapid growth and the emergence of overheating pressures calls for further macroeconomic tightening. At the same time, complications to macroeconomic management from the surge in capital flows appear to be receding in many countries in the region. Over the longer term, the main challenge for Asian economies remains achieving a more balanced and inclusive pattern of growth.