Oil field in Baku, Azerbaijan: Countries can use this period of strong commodity prices to build up fiscal cushions (photo: David Mdzinarishvili/Reuters/Corbis)

REGIONAL ECONOMIC OUTLOOK

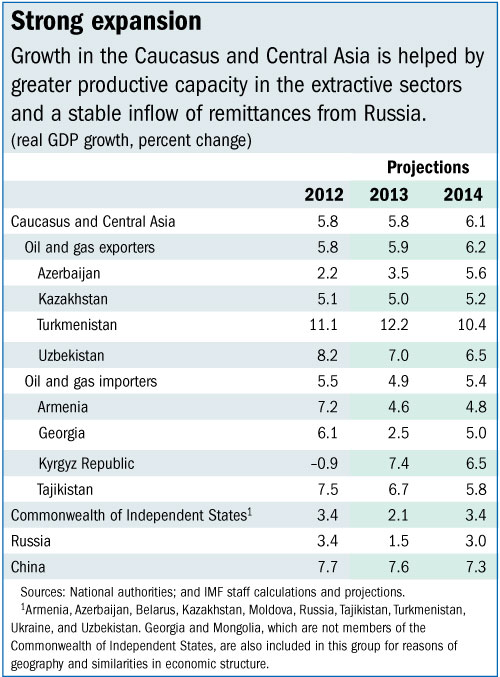

The IMF’s Regional Economic Outlook for the Caucasus and Central Asia, released October 25, projects that growth in the region will average about 6 percent in 2013-14.

This strong growth reflects the expansion of production in hydrocarbons and other extractive industries as well as firm growth in domestic demand, supported by stable remittance inflows, the report says.

“The favorable outlook presents an opportunity for the region to begin the structural transformation into dynamic emerging economies,” said Juha Kähkönen, Deputy Director of the IMF’s Middle East and Central Asia Department, who unveiled the report in Almaty, Kazakhstan.

Expansion continues…

Growth for the region’s oil- and gas-exporting countries—Azerbaijan, Kazakhstan, Turkmenistan, and Uzbekistan—is projected to pick up slightly, to about 6 percent in 2013 and 6.2 percent in 2014 (see table). This growth is driven mainly by the recovery in oil and gas production in Kazakhstan and elsewhere.

For the oil- and gas-importing countries—Armenia, Georgia, the Kyrgyz Republic, and Tajikistan—growth is set to slow to about 5 percent in 2013 before rising to about 5½ percent in 2014, if private investment and external demand pick up as expected.

…but risks remain

The report cautioned that lower-than-anticipated growth rates in emerging markets, including, among others, China and Russia, would reduce commodity prices further and cause economic activity in the region’s oil- and gas-exporting countries to weaken.

A slowdown in emerging markets could also affect the region’s oil-importing countries by dampening exports and bilateral official project lending. Russia’s slowdown, in particular, is an important source of risk for the oil importers, in light of its close linkages with the region. Remittances from migrants working in Russia have so far remained strong, but a marked slowdown in that country could reverse this situation.

The report notes that most countries in the CCA region need to consolidate their budgets to build up their fiscal cushions and ensure that fiscal positions are sustainable. These steps are particularly necessary in light of the risk of lower oil prices and, in some countries, higher expenditures and challenges in implementing tax reforms. The region’s countries should take advantage of their continued strong expansion to strengthen their fiscal cushion, the IMF report says.

For most of the region’s countries, inflation is expected to stay within central banks’ comfort zones—except in Uzbekistan, where it will remain double digits, and in Georgia, which has been experiencing deflation since early 2012.

Aiming for emerging market status

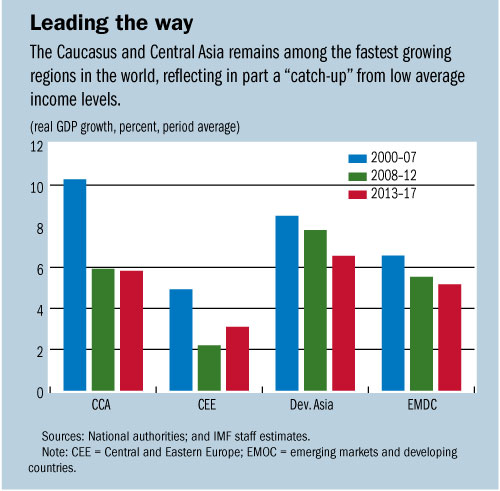

Countries of the CCA region have recorded significant economic achievements during the two decades since their independence following the breakup of the Soviet Union, the IMF report noted. In fact, the CCA remains among the fastest growing regions in the world, although growth has slowed from the rates experienced in the decade leading up to the global financial crisis (see chart). Still, there is scope for improvement, the IMF said.

“CCA countries can seize the opportunity afforded by strong commodity prices and remittance flows to pursue ambitious reforms that will allow them to reach emerging market status over the medium term,” Kähkönen said.

To help achieve its emerging market vision of high, sustainable, and inclusive growth, the IMF recommends that region’s policymakers:

• Enhance structural reforms and regional cooperation. All CCA economies need to find room for more social spending in support of inclusive growth, such as greater investment in education and enhanced social safety nets. Reforms focusing on improving governance and the business climate would deepen and sustain competitive markets, while greater regional cooperation could help drive and diversify growth.

• Strengthen fiscal frameworks. Improved fiscal frameworks could support fiscal sustainability and help rebuild the cushions needed to manage shocks and growth volatility.

• Improve the effectiveness of monetary policy. Stronger monetary frameworks would allow CCA countries to consolidate gains from price stability, increase the resilience of their economies to shocks, and support growth. Moving toward exchange rate flexibility would help make monetary policy more effective.

• Foster financial sector development. Underdeveloped financial systems limit the effectiveness of monetary policy and hamper productive private investment and job creating growth. Policymakers could work toward applying prudential rules evenly across financial institutions, providing easier access to finance for small and medium-sized enterprises, and developing capital markets.