IMFSurvey Magazine: IMF Research

A Chinese worker rides past a poster showing Beijing's central business district. A sharper-than-expected slowdown in China could spill over to other countries through effects on trade, asset and commodity prices, and confidence (photo: Jason Lee/Reuters/Corbis)

WORLD ECONOMIC OUTLOOK UPDATE

Weak Pickup in Global Growth, with Risks Pivoting to Emerging Markets

IMF Survey

January 19, 2016

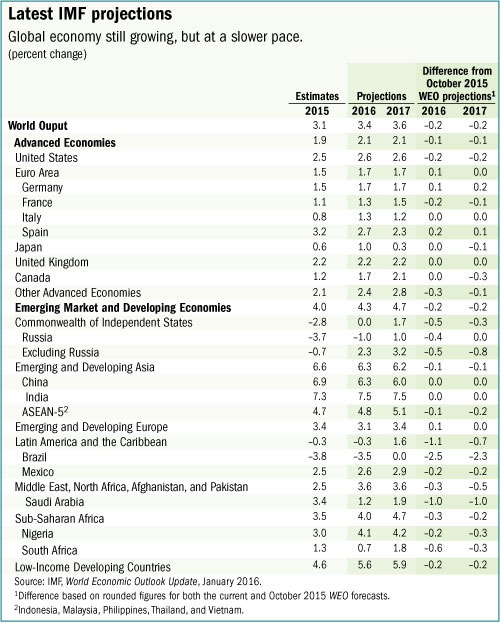

- Global growth forecast revised down—3.4 percent in 2016 and 3.6 percent in 2017

- Emerging market and developing economies facing increased challenges

- Key risks relate to China slowdown, stronger dollar, geopolitical tensions, renewed global risk aversion

The pickup in global growth is weak and uneven across economies, with risks now tilted toward the emerging markets, says the IMF’s latest World Economic Outlook (WEO) Update.

Advanced economies will see a modest recovery, while emerging market and developing economies face the new reality of slower growth.

The WEO Update now projects global growth at 3.4 percent this year and 3.6 percent in 2017 (see Table), slightly lower than the forecast issued in October 2015.

“This coming year is going to be a year of great challenges and policymakers should be thinking about short-term resilience and the ways they can bolster it, but also about the longer-term growth prospects,” said Maurice Obstfeld, IMF Economic Counsellor and Director of Research.

”Those long-term actions,” he continued, “will actually have positive effects in the short run by increasing confidence and increasing people's faith in the future.”

Marginal improvements in advanced economies

Growth in advanced economies is projected to rise to 2.1 percent and to hold steady in 2017, a slightly weaker pickup than that forecast in October.

Overall activity remains robust in the United States, supported by still-easy financial conditions and strengthening housing and labor markets. But there are also challenges stemming from the strength of the dollar, which is causing the U.S. manufacturing sector to shrink marginally.

In the euro area, stronger private consumption supported by lower oil prices and easy financial conditions is outweighing a weakening of net exports.

Growth in Japan is also expected to firm up in 2016, on the back of fiscal support, lower oil prices, accommodative financial conditions, and rising incomes.

Emerging markets face growth slowdown

Emerging market and developing economies are now confronting a new reality of lower growth, with cyclical and structural forces undermining the traditional growth paradigm, as IMF chief Christine Lagarde pointed out in a recent speech.

Growth forecasts for most emerging market and developing economies reveal a slower pickup than previously predicted. Growth is projected to increase from 4 percent in 2015—the lowest rate since the 2008–09 financial crisis—to 4.3 and 4.7 percent in 2016 and 2017, respectively.

But these overall numbers fail to do full justice to the diversity of situations across countries.

India and parts of emerging Asia are bright spots, projected to grow at a robust pace, whereas Latin America and the Caribbean will again see a contraction in 2016, reflecting the recession in Brazil and economic stress elsewhere in the region, even as most other countries in the region will continue to grow. Emerging Europe is expected to grow at a steady pace, albeit with some slowing in 2016, given that Russia could remain in recession in 2016. Most countries in sub-Saharan Africa will see a gradual pickup in growth, but only to rates that remain lower than those achieved during the past decade.

Risks tilted to downside

Looking beyond the short-run forecasts, there are important risks to the outlook, which are particularly prominent for emerging market and developing economies and could stall global recovery.

These risks relate mostly to the ongoing adjustments of the global economy, namely China’s rebalancing, lower commodity prices, and the prospects for the progressive increase in interest rates in the United States. They include the following possibilities:

• A sharper-than-expected slowdown in China, which could bring more international spillovers through trade, commodity prices, and waning confidence.

• A further appreciation of the dollar and tighter global financing conditions which could raise vulnerabilities in emerging markets, possibly creating adverse effects on corporate balance sheets and raising funding challenges for those with high dollar exposures.

• A sudden bout of global risk aversion, regardless of the trigger, could lead to sharp further depreciations and possible financial strains in vulnerable emerging market economies.

• An escalation of ongoing geopolitical tensions in a number of regions, which could affect confidence and disrupt global trade, financial flows, and tourism. New economic or political shocks in countries currently in economic distress which could also derail the projected pickup in activity.

Commodity markets pose two-sided risks. On the downside, further declines in commodity prices would worsen the outlook for already-fragile commodity producers, and widening yields on energy sector debt threaten a broader tightening of credit conditions.

On the upside, the recent decline in oil prices may provide a stronger boost to demand in oil importers, including through consumers’ possible perception that prices will remain lower for longer.

“All in all, there is a lot of uncertainty out there, and I think that contributes to the volatility,” said Obstfeld. “We may be in for a bumpy ride this year, especially in the emerging and developing world,” he said.

Raising growth still a priority

In this global environment, with the risk of low growth persisting for a long time, the WEO Update underlines the urgent need for policymakers to raise actual and potential growth through a mix of demand support and structural reforms.

Structural reforms, in particular, remain critical. Priorities vary, but many advanced economies would benefit from reforms to strengthen labor force participation (Japan, euro area) and overall employment levels (given aging populations), as well as measures to tackle private debt overhangs.

Policymakers in emerging markets and developing economies need to redirect activity to new sources of growth. Lifting growth will also ensure continued convergence toward advanced economy income levels.

These economies also need to press on with structural reforms to remove infrastructure bottlenecks, facilitate a dynamic and innovation-friendly business environment, and bolster human capital through reforms to education, labor, and product markets.

Stay Connected

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Write to us

The IMF Survey welcomes comments, suggestions, and brief readers' letters, a selection of which are posted under What readers say. Letters may be edited. Please address Internet correspondence to imfsurvey@imf.org.