World Economic Outlook (WEO)

Subdued Demand:

Symptoms and Remedies

October 2016

The World Economic Outlook (WEO) presents IMF economists' analyses of global economic developments, issues affecting advanced, emerging, and developing economies, and topics of current interest.

Summary

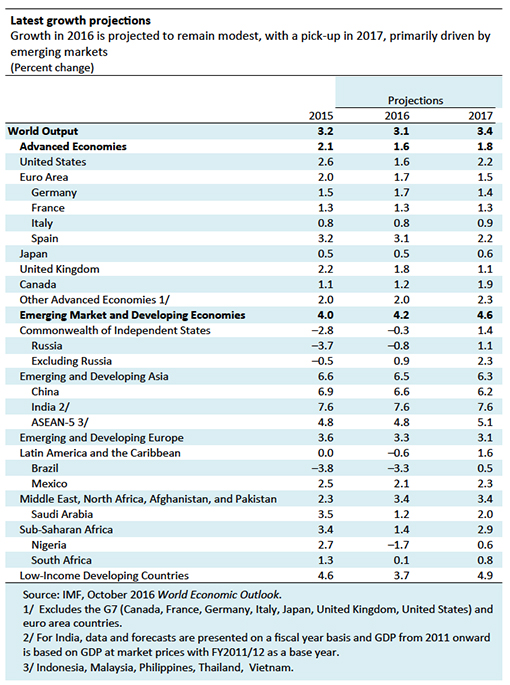

Global growth is projected to slow to 3.1 percent in 2016 before recovering to 3.4 percent in 2017. The forecast, revised down by 0.1 percentage point for 2016 and 2017 relative to April, reflects a more subdued outlook for advanced economies following the June U.K. vote in favor of leaving the European Union (Brexit) and weaker-than-expected growth in the United States. These developments have put further downward pressure on global interest rates, as monetary policy is now expected to remain accommodative for longer.

Front Matter

Chapter 1: Global Prospects and Policies

Full Text News Article Video{kind=link}

| Figures | |||

|---|---|---|---|

| Chart | Data | 1.1 | Global Activity Indicators |

| Chart | Data | 1.2 | Global Inflation |

| Chart | Data | 1.3 | Commodity and Oil Markets |

| Chart | Data | 1.4 | Real Effective Exchange Rate Changes, March 2016–September 2016 |

| Chart | Data | 1.5 | Emerging Market Economies: Capital Flows |

| Chart | Data | 1.6 | Advanced Economies: Monetary and Financial Market Conditions |

| Chart | Data | 1.7 | Advanced Economies: Credit, House Prices, and Balance Sheets |

| Chart | Data | 1.8 | Emerging Market Economies: Interest Rates |

| Chart | Data | 1.9 | Emerging Market Economies: Equity Markets and Credit |

| Chart | Data | 1.10 | Domestic Demand, Output Gap, Unemployment, and Labor Force Participation in Advanced Economies |

| Chart | Data | 1.11 | Demographics |

| Chart | Data | 1.12 | Advanced Economies: Growth, Investment, and Employment in Recent WEO Vintages |

| Chart | Data | 1.13 | Emerging Markets: Terms-of-Trade Windfall Gains and Losses and Real Exchange Rates |

| Chart | Data | 1.14 | Real per Capita Growth Rates and Convergence (1995–2020) |

| Chart | Data | 1.15 | Fiscal Indicators |

| Chart | Data | 1.16 | External Sector |

| Chart | Data | 1.17 | Creditors versus Debtors |

| Chart | Data | 1.18 | Current Account Gaps and Real Exchange Rates |

| Chart | Data | 1.19 | Risks to the Global Outlook |

| Chart | Data | 1.20 | Recession and Deflation Risks |

| Chart | Data | Scen.Fig.1 | Unilateral and Bilateral Imposition of Tariffs on Imported Goods |

| Chart | Data | Scen.Fig.2 | A Worldwide Increase in Protectionism |

| Chart | Data | 1.1.1 | World Growth Projections over the Medium Term |

| Chart | Data | 1.SF.1 | Commodity Market Developments |

| Chart | Data | 1.SF.2 | Producer Support Estimate |

| Chart | Data | 1.SF.3 | World Food Production and Consumption by Country, 2015 |

| Chart | Data | 1.SF.4 | Population and World Food Consumption |

| Chart | Data | 1.SF.5 | Maize Yield |

| Chart | Data | 1.SF.6 | Food Prices and Violent Events |

| Chart | Data | 1.SF.7 | Global Food Security Index, 2016 |

| Chart | Data | 1.SF.1.1 | Evolution of Deals over Time by Target Region |

The forces shaping the global outlook—both those operating over the short and long term—point to subdued growth for 2016 and a gradual recovery thereafter but also to downside risks. These forces include new shocks, such as Brexit; ongoing realignments in China and among commodity exporters; slow-moving trends in demographics and productivity growth, as well as noneconomic factors, such as geopolitical uncertainties.

- Recent Developments and Prospects

- The Forecast

- Risks

- Policy Priorities

- Scenario Box 1. Tariff Scenarios

- Box 1.1. World Growth Projections over the Medium Term

- Special Feature: Commodity Market Developments and Forecasts, with a Focus on Food Security and Markets in the World Economy References

- References

| Tables |

|---|

- Table 1.1. Overview of the World Economic Outlook Projections

- Annex Table 1.1.1. Europe: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Annex Table 1.1.2. Asia and Pacific: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Annex Table 1.1.3. Western Hemisphere: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Annex Table 1.1.4. Commonwealth of Independent States: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Annex Table 1.1.5. Middle East, North Africa, Afghanistan, and Pakistan: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Annex Table 1.1.6. Sub-Saharan Africa: Real GDP, Consumer Prices, Current Account Balance, and Unemployment

- Table 1.SF.1. Used-to-Available Land Suitable for Agriculture by Region, 2013

- Table 1.SF.2. Food Exports

- Table 1.SF.3. Agricultural Yield

- Table 1.SF.4. Urban Population by Region

- Table 1.SF.5. Net Export of Food

- Table 1.SF.6. Share of Food and Beverages in Total Consumption, 2010

- Table 1.SF.1.1. Impact of Land Governance and Food Security on Land Deals

| Figures | |||

|---|---|---|---|

| Chart | Data | 1.1 | Global Activity Indicators |

| Chart | Data | 1.2 | Global Inflation |

| Chart | Data | 1.3 | Commodity and Oil Markets |

| Chart | Data | 1.4 | Real Effective Exchange Rate Changes, March 2016–September 2016 |

| Chart | Data | 1.5 | Emerging Market Economies: Capital Flows |

| Chart | Data | 1.6 | Advanced Economies: Monetary and Financial Market Conditions |

| Chart | Data | 1.7 | Advanced Economies: Credit, House Prices, and Balance Sheets |

| Chart | Data | 1.8 | Emerging Market Economies: Interest Rates |

| Chart | Data | 1.9 | Emerging Market Economies: Equity Markets and Credit |

| Chart | Data | 1.10 | Domestic Demand, Output Gap, Unemployment, and Labor Force Participation in Advanced Economies |

| Chart | Data | 1.11 | Demographics |

| Chart | Data | 1.12 | Advanced Economies: Growth, Investment, and Employment in Recent WEO Vintages |

| Chart | Data | 1.13 | Emerging Markets: Terms-of-Trade Windfall Gains and Losses and Real Exchange Rates |

| Chart | Data | 1.14 | Real per Capita Growth Rates and Convergence (1995–2020) |

| Chart | Data | 1.15 | Fiscal Indicators |

| Chart | Data | 1.16 | External Sector |

| Chart | Data | 1.17 | Creditors versus Debtors |

| Chart | Data | 1.18 | Current Account Gaps and Real Exchange Rates |

| Chart | Data | 1.19 | Risks to the Global Outlook |

| Chart | Data | 1.20 | Recession and Deflation Risks |

| Chart | Data | Scen.Fig.1 | Unilateral and Bilateral Imposition of Tariffs on Imported Goods |

| Chart | Data | Scen.Fig.2 | A Worldwide Increase in Protectionism |

| Chart | Data | 1.1.1 | World Growth Projections over the Medium Term |

| Chart | Data | 1.SF.1 | Commodity Market Developments |

| Chart | Data | 1.SF.2 | Producer Support Estimate |

| Chart | Data | 1.SF.3 | World Food Production and Consumption by Country, 2015 |

| Chart | Data | 1.SF.4 | Population and World Food Consumption |

| Chart | Data | 1.SF.5 | Maize Yield |

| Chart | Data | 1.SF.6 | Food Prices and Violent Events |

| Chart | Data | 1.SF.7 | Global Food Security Index, 2016 |

| Chart | Data | 1.SF.1.1 | Evolution of Deals over Time by Target Region |

Chapter 2: Global Trade: What's behind the Slowdown?

Full Text News Article Video| Figures | |||

|---|---|---|---|

| Chart | Data | 2.1 | World Real Trade and GDP Growth in Historical Perspective |

| Chart | Data | 2.2 | World Trade in Volumes, Values, and across Countries |

| Chart | Data | 2.3 | Trade Dynamics across Broad Country Groups |

| Chart | Data | 2.4 | Trade Dynamics across Types of Trade and Products |

| Chart | Data | 2.5 | Empirical Model: Actual and Predicted Evolution of Real Import Growth |

| Chart | Data | 2.6 | Empirical Model: Difference Between Actual and Predicted Growth of Real Goods Imports |

| Chart | Data | 2.7 | Empirical Model: Decomposing the Slowdown in Real Goods Import Growth |

| Chart | Data | 2.8 | Structural Model: Actual and Model-Implied Evolution of Nominal Import-to-GDP Ratio |

| Chart | Data | 2.9 | Trade Costs in Historical Perspective: A Top-Down Approach |

| Chart | Data | 2.10 | Trade Policies in Historical Perspective |

| Chart | Data | 2.11 | Logistics and Transportation Costs of Trade in Historical Perspective |

| Chart | Data | 2.12 | Global Value Chains in Historical Perspective |

| Chart | Data | 2.13 | Contribution of Trade Policies and Global Value Chains to the Slowdown in Real Goods Import Growth |

| Chart | Data | 2.14 | Gravity Model: Global Value Chain Participation and Bilateral Sectoral Trade Growth |

| Chart | Data | Annex 2.1.1 |

Nominal Import Growth across Categories of Services |

| Chart | Data | Annex 2.2.1 |

Real Import Growth |

| Chart | Data | Annex 2.5.1 |

Trade Finance Availability |

| Chart | Data | Annex 2.5.2 |

Contribution of Trade Policies and Global Value Chains to the Slowdown in Real and Nominal Goods Import Growth |

| Chart | Data | 2.1.1 | The Evolution of Trade across Industries in Major Economies |

| Chart | Data | 2.2.1 | Potential Gains from Tackling Traditional Trade Barriers |

| Chart | Data | 2.2.2 | Trade Policy Frontier Areas |

| Chart | Data | 2.3.1 | Gains from Eliminating Tariffs and Implementing the World Trade Organization Trade Facilitation Agreement |

Trade growth has slowed since 2012 relative both to its strong historical performance and to overall economic growth. This chapter finds that the overall weakness in economic activity, in particular in investment, has been the primary restraint on trade growth, accounting for up to three-fourths of the slowdown. However, other factors are also weighing on trade. The waning pace of trade liberalization and the recent uptick in protection-ism are holding back trade growth, even though their quantitative impact thus far has been limited. The decline in the growth of global value chains has also played an important part in the observed slowdown. The findings suggest that addressing the general weak-ness in economic activity, especially in investment, will stimulate trade, which in turn could help strengthen productivity and growth. In addition, given the subdued global growth outlook, further trade reforms that lower barriers, coupled with measures to mitigate the cost to those who shoulder the burden of adjustment, would boost the international exchange of goods and services and revive the virtuous cycle of trade and growth.

- The Implications of Trade for Productivity and Welfare: A Primer

- The Slowdown in Trade Growth: Key Patterns

- Understanding the Slowdown in Trade Growth

- Summary and Policy Implications

- Box 2.1. Is the Trade Slowdown Contributing to the Global Productivity Slowdown? New Evidence

- Box 2.2. The Role of Trade Policies in Reinvigorating Trade

- Box 2.3. Potential Gains from Jump-Starting Trade Liberalization References

- Annex 2.1. Data

- Annex 2.2. Constructing Disaggregated Import Volume and Price Indices

- Annex 2.3. Analysis Using an Empirical Model of Import Demand

- Annex 2.4. Analysis Using a General Equilibrium Model

- Annex 2.5. Analysis at the Product Level

- Annex 2.6. Analysis Using Gravity Model of Trade

- References

| Tables |

|---|

- Table 2.1. Historical Association among Real Import Growth at the Product Level, Trade Policies, and Participation in Global Value Chains

- Table 2.1.1. Baseline Estimation Results

- Table 2.2.1. Trade Policy Challenges Vary across Countries

- Annex Table 2.1.1. Data Sources

- Annex Table 2.1.2. Sample of Economies Included in the Analytical Exercises

- Annex Table 2.3.1. Import Content of Aggregate Demand Components

- Annex Table 2.3.2. Empirical Model of Real Imports of Goods and Services

- Annex Table 2.3.3. Empirical Model of Real Imports of Goods

- Annex Table 2.3.4. Empirical Model of Real Imports of Services

- Annex Table 2.3.5. Residuals: Real Goods Import Growth

- Annex Table 2.3.6. Residuals: Real Services Import Growth

- Annex Table 2.3.7. Residuals: Real Goods import Growth Controlling for Global Uncertainty, Global Financial Conditions, and Financial Stress

- Annex Table 2.3.8. Decomposing the Decline in Real Goods Import Growth: Full Sample

- Annex Table 2.3.9. Residuals: Real Goods Import Growth, Corrected for Potential Effect of Trade Policies on Aggregate Demand

- Annex Table 2.3.10. Decomposing the Decline in Real Goods Import Growth Controlling for Trade Policies

- Annex Table 2.5.1. Alternative Specifications for Real Imports in Product-Level Regressions

- Annex Table 2.5.2. Alternative Specifications for Nominal Imports in Product-Level Regressions

- Annex Table 2.6.1. Link between Global Value Chain Integration and Yearly Nominal Import Growth Using Gravity Model Estimated in Levels

- Annex Table 2.6.2. Link between Global Value Chain Integration and Yearly Nominal Import Growth Using Gravity Model Estimated in Growth Rates

| Figures | |||

|---|---|---|---|

| Chart | Data | 2.1 | World Real Trade and GDP Growth in Historical Perspective |

| Chart | Data | 2.2 | World Trade in Volumes, Values, and across Countries |

| Chart | Data | 2.3 | Trade Dynamics across Broad Country Groups |

| Chart | Data | 2.4 | Trade Dynamics across Types of Trade and Products |

| Chart | Data | 2.5 | Empirical Model: Actual and Predicted Evolution of Real Import Growth |

| Chart | Data | 2.6 | Empirical Model: Difference Between Actual and Predicted Growth of Real Goods Imports |

| Chart | Data | 2.7 | Empirical Model: Decomposing the Slowdown in Real Goods Import Growth |

| Chart | Data | 2.8 | Structural Model: Actual and Model-Implied Evolution of Nominal Import-to-GDP Ratio |

| Chart | Data | 2.9 | Trade Costs in Historical Perspective: A Top-Down Approach |

| Chart | Data | 2.10 | Trade Policies in Historical Perspective |

| Chart | Data | 2.11 | Logistics and Transportation Costs of Trade in Historical Perspective |

| Chart | Data | 2.12 | Global Value Chains in Historical Perspective |

| Chart | Data | 2.13 | Contribution of Trade Policies and Global Value Chains to the Slowdown in Real Goods Import Growth |

| Chart | Data | 2.14 | Gravity Model: Global Value Chain Participation and Bilateral Sectoral Trade Growth |

| Chart | Data | Annex 2.1.1 |

Nominal Import Growth across Categories of Services |

| Chart | Data | Annex 2.2.1 |

Real Import Growth |

| Chart | Data | Annex 2.5.1 |

Trade Finance Availability |

| Chart | Data | Annex 2.5.2 |

Contribution of Trade Policies and Global Value Chains to the Slowdown in Real and Nominal Goods Import Growth |

| Chart | Data | 2.1.1 | The Evolution of Trade across Industries in Major Economies |

| Chart | Data | 2.2.1 | Potential Gains from Tackling Traditional Trade Barriers |

| Chart | Data | 2.2.2 | Trade Policy Frontier Areas |

| Chart | Data | 2.3.1 | Gains from Eliminating Tariffs and Implementing the World Trade Organization Trade Facilitation Agreement |

Chapter 3: Global Disinflation in an Era of Constrained Monetary Policy

Full Text News Article| Figures | |||

|---|---|---|---|

| Chart | Data | 3.1 | Oil Prices and Consumer Price Inflation |

| Chart | Data | 3.2 | Share of Countries with Low Inflation |

| Chart | Data | 3.3 | Medium-Term Inflation Expectations and Oil Prices |

| Chart | Data | 3.4 | Effect of Disinflationary Shocks in Advanced Economies under Constrained Monetary Policy and Unanchored Inflation Expectations |

| Chart | Data | 3.5 | Consumer Price Inflation |

| Chart | Data | 3.6 | Share of Consumer Price Inflation Variation Explained by First Common Factor |

| Chart | Data | 3.7 | Core Consumer Price Inflation |

| Chart | Data | 3.8 | Wage Inflation in Advanced Economies |

| Chart | Data | 3.9 | Sectoral Producer Prices in Advanced Economies |

| Chart | Data | 3.10 | Sectoral Consumer Prices in Advanced Economies |

| Chart | Data | 3.11 | Estimated Phillips Curve Parameters |

| Chart | Data | 3.12 | Contribution to Inflation Deviations from Targets: Advanced Economies |

| Chart | Data | 3.13 | Contribution to Inflation Deviations from Targets: Emerging Market Economies |

| Chart | Data | 3.14 | Correlation of Manufacturing Slack in China, Japan, and the United States with Import Price Contribution to Inflation in Other Economies |

| Chart | Data | 3.15 | Survey- and Market-Based Inflation Expectations |

| Chart | Data | 3.16 | Sensitivity of Inflation Expectations to Inflation Surprises |

| Chart | Data | 3.17 | Sensitivity of Inflation Expectations to Inflation Surprises and Monetary Policy Frameworks |

| Chart | Data | 3.18 | Sensitivity of Inflation Expectations to Inflation Surprises before and after Adoption of Inflation Targeting |

| Chart | Data | 3.19 | Sensitivity of Inflation Expectations to Inflation Surprises over Time |

| Chart | Data | 3.20 | Change in Sensitivity of Inflation Expectations to Inflation Surprises |

| Chart | Data | 3.21 | Average Sensitivity of Inflation Expectations to Inflation Surprises in Countries at the Effective Lower Bound |

| Chart | Data | 3.22 | Sensitivity of Longer-Term Inflation Expectations to Changes in Oil Prices |

| Chart | Data | Annex 3.2.1 |

Effect of Disinflationary Shocks on Core Inflation in Advanced Economies under Constrained Monetary Policy |

| Chart | Data | Annex 3.2.2 |

Effect of Disinflationary Shocks on Core Inflation in Advanced Economies under Constrained Monetary Policy and Unanchored Inflation Expectations |

| Chart | Data | Annex 3.3.1 |

Share of Consumer Price Inflation Variation Explained by Different Factors |

| Chart | Data | Annex 3.3.2 |

First Common Factor and Commodity Prices |

| Chart | Data | Annex 3.4.1 |

Contribution to Inflation Deviations from Targets Using Various Measures of Inflation Expectations |

| Chart | Data | Annex 3.4.2 |

Contribution to Inflation Deviations from Targets Using Various Measures of Cyclical Unemployment |

| Chart | Data | Annex 3.4.3 |

Correlation of Manufacturing Slack in China, Japan, and the United States with Import Price Contribution to Inflation in Other Economies |

| Chart | Data | 3.4.4 | Correlation of China Manufacturing Slack with Import Price Contribution to Inflation in Other Economies—Results from Panel Regressions |

| Chart | Data | Annex 3.5.1 |

Change in Inflation Expectations and Inflation Shocks |

| Chart | Data | Annex 3.5.2 |

Sensitivity of Inflation Expectations when Controlling for Slack: Advanced Economies |

| Chart | Data | 3.1.1 | Producer Price and Consumer Price Inflation in China, Japan, and the United States |

| Chart | Data | 3.1.2 | Industrial Slack in China, Japan, and the United States |

| Chart | Data | 3.1.3 | Decomposition for Total Producer Price Inflation for China, Japan, and the United States |

| Chart | Data | 3.2.1 | Inflation Dynamics |

| Chart | Data | 3.2.2 | Cyclical and Structural Indicators in Japan |

| Chart | Data | 3.2.3 | Policy Indicators in Japan |

| Chart | Data | 3.3.1 | Food Weights in Consumption and Per Capita GDP |

| Chart | Data | 3.3.2 | World Food Prices and Consumer Food Prices |

| Chart | Data | 3.3.3 | Food Prices Relative to Nonfood Prices |

| Chart | Data | 3.3.4 | Food Pass-Through Coefficients for Various Country Groups |

| Chart | Data | 3.3.5 | Distribution of Food Pass-Through Coefficients |

| Chart | Data | 3.4.1 | Commodity Prices and Producer Prices |

| Chart | Data | 3.4.2 | Contribution to Cumulative Producer Price Inflation |

| Chart | Data | 3.5.1 | Forecast as Envisaged at 2009:Q2: Loss-Minimization versus Linear Reaction Function |

Inflation has declined markedly in many economies over the past few years. This chapter finds that disinflation is broad based across countries, measures, and sectors—albeit larger for tradable goods than for services. The main drivers of recent disinflation are persistent economic slack and softening commodity prices. Most of the available measures of medium-term inflation expectations have not declined substantially so far. However, the sensitivity of expectations to inflation surprises—an indicator of the degree of anchoring of inflation expectations—has increased in countries where policy rates have approached their effective lower bounds. While the magnitude of this change in sensitivity is modest, it does suggest that the perceived ability of monetary policy to combat persistent disinflation may be diminishing in these economies.

- A Primer on the Costs of Disinflation, Persistently Low Inflation, and Deflation Inflation Dynamics: Patterns and Recent Drivers

- Inflation Dynamics: Patterns and Recent Drivers

- How Well Anchored Are Inflation Expectations?

- Summary and Policy Implications

- Annex 3.1. Sample and Data

- Annex 3.2. Model Simulations

- Annex 3.3. Principal Component Analysis

- Annex 3.4. Drivers of the Recent Decline in Inflation

- Annex 3.5. The Effect of Inflation Shocks on Inflation Expectations

- Box 3.1. Industrial Slack and Producer Price Inflation

- Box 3.2. The Japanese Experience with Deflation

- Box 3.3. How Much Do Global Prices Matter for Food Inflation?

- Box 3.4. The Impact of Commodity Prices on Producer Price Inflation

- Box 3.5. A Transparent Risk-Management Approach to Monetary Policy

- References

| Tables |

|---|

- Table 3.3.1. Cross-Country Determinants of Pass-Through of Free-on-Board Food Prices to Food Consumer Price Inflation

- Annex Table 3.1.1. Sample of Advanced and Emerging Market Economies

- Annex Table 3.1.2. Data Sources

- Table 3.3.1. Cross-Country Determinants of Pass-Through of Free-on-Board Food Prices to Food Consumer Price Inflation

- Annex Table 3.1.1. Sample of Advanced and Emerging Market Economies

- Annex Table 3.1.2. Data Sources

| Figures | |||

|---|---|---|---|

| Chart | Data | 3.1 | Oil Prices and Consumer Price Inflation |

| Chart | Data | 3.2 | Share of Countries with Low Inflation |

| Chart | Data | 3.3 | Medium-Term Inflation Expectations and Oil Prices |

| Chart | Data | 3.4 | Effect of Disinflationary Shocks in Advanced Economies under Constrained Monetary Policy and Unanchored Inflation Expectations |

| Chart | Data | 3.5 | Consumer Price Inflation |

| Chart | Data | 3.6 | Share of Consumer Price Inflation Variation Explained by First Common Factor |

| Chart | Data | 3.7 | Core Consumer Price Inflation |

| Chart | Data | 3.8 | Wage Inflation in Advanced Economies |

| Chart | Data | 3.9 | Sectoral Producer Prices in Advanced Economies |

| Chart | Data | 3.10 | Sectoral Consumer Prices in Advanced Economies |

| Chart | Data | 3.11 | Estimated Phillips Curve Parameters |

| Chart | Data | 3.12 | Contribution to Inflation Deviations from Targets: Advanced Economies |

| Chart | Data | 3.13 | Contribution to Inflation Deviations from Targets: Emerging Market Economies |

| Chart | Data | 3.14 | Correlation of Manufacturing Slack in China, Japan, and the United States with Import Price Contribution to Inflation in Other Economies |

| Chart | Data | 3.15 | Survey- and Market-Based Inflation Expectations |

| Chart | Data | 3.16 | Sensitivity of Inflation Expectations to Inflation Surprises |

| Chart | Data | 3.17 | Sensitivity of Inflation Expectations to Inflation Surprises and Monetary Policy Frameworks |

| Chart | Data | 3.18 | Sensitivity of Inflation Expectations to Inflation Surprises before and after Adoption of Inflation Targeting |

| Chart | Data | 3.19 | Sensitivity of Inflation Expectations to Inflation Surprises over Time |

| Chart | Data | 3.20 | Change in Sensitivity of Inflation Expectations to Inflation Surprises |

| Chart | Data | 3.21 | Average Sensitivity of Inflation Expectations to Inflation Surprises in Countries at the Effective Lower Bound |

| Chart | Data | 3.22 | Sensitivity of Longer-Term Inflation Expectations to Changes in Oil Prices |

| Chart | Data | Annex 3.2.1 |

Effect of Disinflationary Shocks on Core Inflation in Advanced Economies under Constrained Monetary Policy |

| Chart | Data | Annex 3.2.2 |

Effect of Disinflationary Shocks on Core Inflation in Advanced Economies under Constrained Monetary Policy and Unanchored Inflation Expectations |

| Chart | Data | Annex 3.3.1 |

Share of Consumer Price Inflation Variation Explained by Different Factors |

| Chart | Data | Annex 3.3.2 |

First Common Factor and Commodity Prices |

| Chart | Data | Annex 3.4.1 |

Contribution to Inflation Deviations from Targets Using Various Measures of Inflation Expectations |

| Chart | Data | Annex 3.4.2 |

Contribution to Inflation Deviations from Targets Using Various Measures of Cyclical Unemployment |

| Chart | Data | Annex 3.4.3 |

Correlation of Manufacturing Slack in China, Japan, and the United States with Import Price Contribution to Inflation in Other Economies |

| Chart | Data | 3.4.4 | Correlation of China Manufacturing Slack with Import Price Contribution to Inflation in Other Economies—Results from Panel Regressions |

| Chart | Data | Annex 3.5.1 |

Change in Inflation Expectations and Inflation Shocks |

| Chart | Data | Annex 3.5.2 |

Sensitivity of Inflation Expectations when Controlling for Slack: Advanced Economies |

| Chart | Data | 3.1.1 | Producer Price and Consumer Price Inflation in China, Japan, and the United States |

| Chart | Data | 3.1.2 | Industrial Slack in China, Japan, and the United States |

| Chart | Data | 3.1.3 | Decomposition for Total Producer Price Inflation for China, Japan, and the United States |

| Chart | Data | 3.2.1 | Inflation Dynamics |

| Chart | Data | 3.2.2 | Cyclical and Structural Indicators in Japan |

| Chart | Data | 3.2.3 | Policy Indicators in Japan |

| Chart | Data | 3.3.1 | Food Weights in Consumption and Per Capita GDP |

| Chart | Data | 3.3.2 | World Food Prices and Consumer Food Prices |

| Chart | Data | 3.3.3 | Food Prices Relative to Nonfood Prices |

| Chart | Data | 3.3.4 | Food Pass-Through Coefficients for Various Country Groups |

| Chart | Data | 3.3.5 | Distribution of Food Pass-Through Coefficients |

| Chart | Data | 3.4.1 | Commodity Prices and Producer Prices |

| Chart | Data | 3.4.2 | Contribution to Cumulative Producer Price Inflation |

| Chart | Data | 3.5.1 | Forecast as Envisaged at 2009:Q2: Loss-Minimization versus Linear Reaction Function |

Chapter 4: Spillovers from China’s Transition and from Migration

Full Text News Article Video| Figures | |||

|---|---|---|---|

| Chart | Data | 4.1 | China: GDP and Trade Growth |

| Chart | Data | 4.2 | Number of International Migrants and Refugees |

| Chart | Data | 4.3 | China: Global Clout and Rebalancing |

| Chart | Data | 4.4 | Spillovers from China over Time |

| Chart | Data | 4.5 | Impact on Exports of a 1-Percent Shock to China’s Demand after One Year |

| Chart | Data | 4.6 | Decline in Average Export Growth Rate Attributed to China Demand, 2014:Q1–2015:Q3 |

| Chart | Data | 4.7 | China: Processing Trade |

| Chart | Data | 4.8 | A Large Footprint in Commodity Markets |

| Chart | Data | 4.9 | Cumulative One-Year Price Impact from a 1 Percent Shock to China’s Industrial Production |

| Chart | Data | 4.10 | China: Slowdown Scenario |

| Chart | Data | 4.11 | Spillovers from China |

| Chart | Data | 4.12 | Transmission of Spillovers through Financial Channels |

| Chart | Data | 4.13 | China: Cyclical Slowdown Scenario |

| Chart | Data | 4.14 | International Migrants and Refugees |

| Chart | Data | 4.15 | Migration by Age and Skill |

| Chart | Data | 4.16 | Determinants of Migration |

| Chart | Data | 4.17 | Females: Low Education versus High Skilled, 2000 |

| Chart | Data | 4.18 | Labor Market Performance |

| Chart | Data | 4.19 | Germany: Present Value of Expected Future Net Fiscal Contribution by Age Group |

| Chart | Data | 4.20 | Estimated Impact of Migration in More Developed Economies, 2100 |

| Chart | Data | 4.21 | Migration: Positive Longer-Term Growth Effects |

| Chart | Data | 4.22 | Contributions of Outward Migration to Population Growth |

| Chart | Data | 4.23 | Migration of Population with Tertiary Education |

| Chart | Data | 4.24 | Remittances and Diasporas |

| Chart | Data | 4.1.1 | China’s Ties with Low-Income and Developing Countries |

| Chart | Data | 4.3.1 | Migration in Sub-Saharan Africa |

| Chart | Data | 4.3.2 | Age and Education of Migrants and Origin Country Population |

| Chart | Data | 4.3.3 | Top Receivers of Remittances in Sub-Saharan Africa, 2013–15 |

Spillovers are a key factor shaping the global outlook and the risks around it, and the growing clout of emerging markets means that they are playing an increasing role, including from noneconomic shocks. This chapter analyzes spillovers of: (i) China’s rebalancing towards more sustainable growth, and (ii) increasing migration flows. China’s transition has a direct negative impact on global demand through trade, an indirect impact through commodity prices, and an effect on asset prices. However, a well-managed transition will benefit the global economy in the long term, with more sustainable growth in China and a reduction of risks of a disruptive adjustment. China can help by accepting the slowdown and by clearly communicating its policy intentions. Countries experiencing negative spillovers can use policy buffers in the short term, but plan for adjustment and explore new opportunities to bolster trade. As for migration, it can provoke political backlash in recipient economies, but offers gains in terms of higher growth and relief from population aging. Labor market integration is key to harnessing the gains in terms of growth and migrants’ contributions to the fiscal accounts. Source countries may face negative growth effects, which can be mitigated by remittances, the benefits of diaspora networks, and policies addressing the effects of emigration of young and skilled population.

- Introduction

- The Challenges and Opportunities of Migration

- Box 4.1. China’s Ties with Low Income and Developing Countries

- Box 4.2. Conflicts Driving Migration: Middle East and North Africa

- Box 4.3. Migration in Sub-Saharan Africa

- References

| Figures | |||

|---|---|---|---|

| Chart | Data | 4.1 | China: GDP and Trade Growth |

| Chart | Data | 4.2 | Number of International Migrants and Refugees |

| Chart | Data | 4.3 | China: Global Clout and Rebalancing |

| Chart | Data | 4.4 | Spillovers from China over Time |

| Chart | Data | 4.5 | Impact on Exports of a 1-Percent Shock to China’s Demand after One Year |

| Chart | Data | 4.6 | Decline in Average Export Growth Rate Attributed to China Demand, 2014:Q1–2015:Q3 |

| Chart | Data | 4.7 | China: Processing Trade |

| Chart | Data | 4.8 | A Large Footprint in Commodity Markets |

| Chart | Data | 4.9 | Cumulative One-Year Price Impact from a 1 Percent Shock to China’s Industrial Production |

| Chart | Data | 4.10 | China: Slowdown Scenario |

| Chart | Data | 4.11 | Spillovers from China |

| Chart | Data | 4.12 | Transmission of Spillovers through Financial Channels |

| Chart | Data | 4.13 | China: Cyclical Slowdown Scenario |

| Chart | Data | 4.14 | International Migrants and Refugees |

| Chart | Data | 4.15 | Migration by Age and Skill |

| Chart | Data | 4.16 | Determinants of Migration |

| Chart | Data | 4.17 | Females: Low Education versus High Skilled, 2000 |

| Chart | Data | 4.18 | Labor Market Performance |

| Chart | Data | 4.19 | Germany: Present Value of Expected Future Net Fiscal Contribution by Age Group |

| Chart | Data | 4.20 | Estimated Impact of Migration in More Developed Economies, 2100 |

| Chart | Data | 4.21 | Migration: Positive Longer-Term Growth Effects |

| Chart | Data | 4.22 | Contributions of Outward Migration to Population Growth |

| Chart | Data | 4.23 | Migration of Population with Tertiary Education |

| Chart | Data | 4.24 | Remittances and Diasporas |

| Chart | Data | 4.1.1 | China’s Ties with Low-Income and Developing Countries |

| Chart | Data | 4.3.1 | Migration in Sub-Saharan Africa |

| Chart | Data | 4.3.2 | Age and Education of Migrants and Origin Country Population |

| Chart | Data | 4.3.3 | Top Receivers of Remittances in Sub-Saharan Africa, 2013–15 |

Statistical Appendix

Full Text- Assumptions

- What's New

- Data and Conventions

- Country Notes

- Classification of Countries

- General Features and Composition of Groups in the World Economic Outlook Classification

- Table A. Classification by World Economic Outlook Groups and Their Shares in Aggregate GDP, Exports of Goods and Services, and Population, 2015

- Table B. Advanced Economies by Subgroup

- Table C. European Union

- Table D. Emerging Market and Developing Economies by Region and Main Source of Export Earnings

- Table E. Emerging Market and Developing Economies by Region, Net External Position, and Status as Heavily Indebted Poor Countries and Low-Income Developing Countries

- Table F. Economies with Exceptional Reporting Periods

- Table G. Key Data Documentation

- Box A1. Economic Policy Assumptions Underlying the Projections for Selected Economies

- World Economic Outlook, Selected Topics

- IMF Executive Board Discussion of the Outlook, September 2016

| List of Tables Part A (Download PDF) |

|---|

- Table A1. Summary of World Output

- Table A2. Advanced Economies: Real GDP and Total Domestic Demand

- Table A3. Advanced Economies: Components of Real GDP

- Table A4. Emerging Market and Developing Economies: Real GDP

- Table A5. Summary of Inflation

- Table A6. Advanced Economies: Consumer Prices

- Table A7. Emerging Market and Developing Economies: Consumer Prices

- Table A8. Major Advanced Economies: General Government Fiscal Balances and Debt

- Table A9. Summary of World Trade Volumes and Prices

- Table A10. Summary of Current Account Balances

- Table A11. Advanced Economies: Balance on Current Account

- Table A12. Emerging Market and Developing Economies: Balance on Current Account

- Table A13. Summary of Financial Account Balances

- Table A14. Summary of Net Lending and Borrowing

- Table A15. Summary of World Medium-Term Baseline Scenario

| List of Tables Part B (Download PDF - available on the web only) |

|---|

- Table B1. Advanced Economies: Unemployment, Employment, and Real GDP per Capita

- Table B2. Emerging Market and Developing Economies: Real GDP

- Table B3. Advanced Economies: Hourly Earnings, Productivity, and Unit Labor Costs in Manufacturing

- Table B4. Emerging Market and Developing Economies: Consumer Prices

- Table B5. Summary of Fiscal and Financial Indicators

- Table B6. Advanced Economies: General and Central Government Net Lending/Borrowing and General Government Net Lending/Borrowing Excluding Social Security Schemes

- Table B7. Advanced Economies: General Government Structural Balances

- Table B8. Emerging Market and Developing Economies: General Government Net Lending/Borrowing and Overall Fiscal Balance

- Table B9. Emerging Market and Developing Economies: General Government Net Lending/Borrowing

- Table B10. Selected Advanced Economies: Exchange Rates

- Table B11. Emerging Market and Developing Economies: Broad Money Aggregates

- Table B12. Advanced Economies: Export Volumes, Import Volumes, and Terms of Trade in Goods and Services

- Table B13. Emerging Market and Developing Economies by Region: Total Trade in Goods

- Table B14. Emerging Market and Developing Economies by Source of Export Earnings: Total Trade in Goods

- Table B15. Summary of Current Account Transactions

- Table B16. Emerging Market and Developing Economies: Summary of External Debt and Debt Service

- Table B17. Emerging Market and Developing Economies by Region: External Debt by Maturity

- Table B18. Emerging Market and Developing Economies by Analytical Criteria: External Debt by Maturity

- Table B19. Emerging Market and Developing Economies: Ratio of External Debt to GDP

- Table B20. Emerging Market and Developing Economies: Debt-Service Ratios

- Table B21. Emerging Market and Developing Economies, Medium-Term Baseline Scenario: Selected Economic Indicators