The year 2010 has opened amid generalized—–but tempered—optimism about the global economic and financial outlook.

The unprecedented scale and scope of the anti-crisis measures taken during the past year—and the unprecedented degree of multilateral policy coordination involved in their design and implementation—appear to have succeeded in averting a downturn of historic proportions.

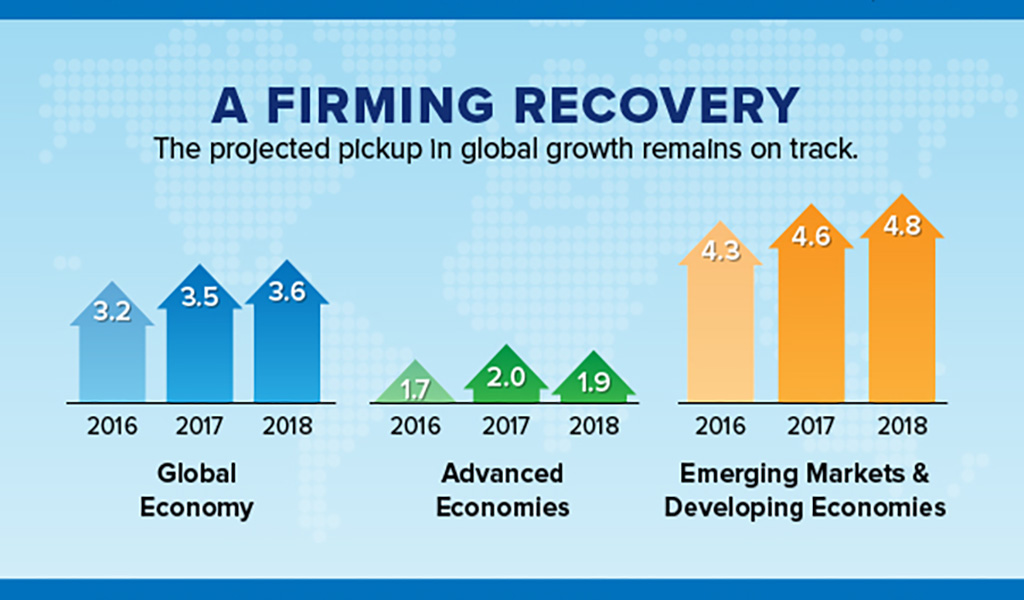

The improved prospects are evident in economic data, in financial market performance, and in the marking up of economic forecasts. In fact, somewhat more upbeat expectations no doubt will be reflected in the regular January update of the IMF’s World Economic Outloook forecast.

[caption id="attachment_1060" align="aligncenter" width="400"] Advanced economy output far below potential, still-cautious businesses and households, plus sluggish loan growth add up to a notable absence of inflation pressures (IMF photo)[/caption]

Advanced economy output far below potential, still-cautious businesses and households, plus sluggish loan growth add up to a notable absence of inflation pressures (IMF photo)[/caption]

In more normal times, the degree of optimism about near-term growth prospects in the advanced economies would be much more intense than at present. For example, U.S. firms reacted to the downturn with aggressive layoffs and unprecedented cutbacks in investment and inventories. In fact, U.S. business investments didn’t even match depreciation during the past two years. As a result, recent improvements in U.S. final sales are boosting both profitability and internally generated funds. Typically, these are key early-cycle building blocks for accelerating growth.

Reasons for caution

But these are not normal times, and the reasons for caution about the outlook remain powerful, pointing to a relatively modest recovery in the advanced economies. High unemployment rates in many cases—coupled with anemic income growth—are limiting consumption gains. Weakened household balance sheets add to the uncertainty about spending prospects. Financial conditions have improved, but in many ways they remain far from normal. Credit losses are still mounting in some sectors, especially commercial real estate.

The combination of advanced economy output that is far below potential, the still-cautious attitudes of businesses and households, plus sluggish loan growth reflecting bankers’ residual reticence, together add up to a notable absence of inflation pressures.

In turn, the combination of large output gaps, low inflation and the prospect of only a moderate advanced economy recovery underscore the Fund’s contention that it is premature to begin withdrawing the important support for growth currently being supplied by accommodative budgetary and monetary policies.

On the more positive side of the balance, the growth outlook remains upbeat in many emerging market economies, especially in Asia.

In most cases, this reflects improving export demand plus resilient domestic demand, the latter in many cases buoyed by significant policy support. With the specter receding of a sustained advanced economy downturn, and with global interest rates low, capital once again is flowing strongly to the best-performing emerging markets, reversing the sudden stop experienced in later 2008.

At least five challenges

Looking forward, the new decade is ushering in a series of at least five key challenges.

The first is to secure the recovery, by ensuring that policies among the key economies remain appropriately supportive of the expansion, as well as globally consistent.

In particular, advanced economy fiscal stimulus planned for 2010 should be implemented fully, even while countries lay out credible medium-term frameworks for limiting spending and debt to sustainable levels. Moving beyond the next several quarters, ensuring a robust global economy will require new growth patterns, including significant rebalancing of the sources of growth among and within most large economies.

The task of establishing the necessary foundations for restored global growth will fall in part to the policies followed by the G-20 countries. The new mutual assessment process agreed at the Pittsburgh Leaders Summit, is intended to do just that—in effect providing the practical implementation of the G-20’s Framework for Strong, Sustained and Balanced Growth. The IMF is helping to provide analytical support for this innovative approach to multilateral cooperation.

A second challenge is to protect the poorest and most vulnerable from the impact of the downturn and to restore growth in low income countries. During 2003–06, sub-Saharan Africa achieved the fastest sustained expansion since the IMF was created, adding to per capita incomes. While raising and sustaining growth in advanced economies would make a substantial contribution to the low income countries’ growth prospects, the expanded direct support provided through various initiatives—including the Fund’s new facilities for low-income countries and sharply increased resources for lending—are intended to provide important additional support.

Financial sector reform

The third challenge is the reform of the financial sector, with the triple goals of making the sector more effective, of reducing the risks of future instability, and to rethink how the potential costs of financial crises might be borne. This is the subject of my next blog.

The fourth challenge is that of restructuring and reforming the governance and mandate of the key international financial institutions. The creation of the G-20 leaders process was a potentially pivotal step in this regard. The leaders, in turn, have endorsed some specific goals for the IMF’s governance reform. That will be the subject of my third offering in this series.

There is a fifth challenge, and it will be the source of intense debate in the coming quarters—perhaps years. The economic success of the Great Moderation of the 1980s and 1990s encouraged policymakers and scholars alike to think that the prevailing framework of rule-based policies would prove to be durable. However, the crisis has called into question not just institutions, but also the intellectual underpinnings for prevailing views regarding economic and financial policies. Already, the Fund is helping to frame and contribute to the intellectual and empirical reassessment that is inevitable and even necessary.

In the coming months, we will be contributing original research as well as sponsoring conferences and symposia in an effort to distill the lessons of the crisis, and to help form a new policy consensus.

One potentially important aspect of this effort will be to devise new lending instruments that—building on the 2009 innovation of the Flexible Credit Line—will allow the Fund to play a larger role as a provider of insurance to our members, and enhancing our ability to help prevent future crises.