(Versions in 中文, Français, 日本語, Русский, and Español)

Five years into the crisis, the fiscal landscape remains challenging. On the positive side, deficit-cutting efforts and the first signs of recovery reduced the fiscal stress felt in many advanced economies; but debt ratios often remain at historical peaks. At the same time, slowing growth and rising borrowing costs, combined with unabated demands for improved public services, puts pressure on government budgets in emerging market economies.

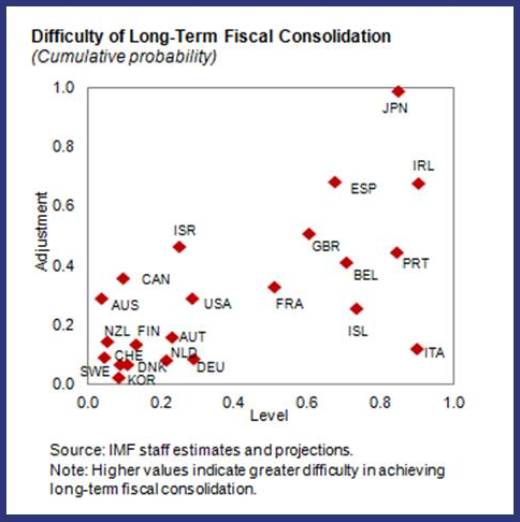

So we created an index of ‘fiscal difficulty’ that shows the biggest challenge ahead for advanced economies is to maintain budget surpluses until debt ratios return to lower levels. We expect this will take several years.

Advanced economies: not yet at the goal line

With the average deficit now lower by more than 4 percentage points of GDP compared to the height of the crisis, most advanced economies are well on their way to meeting their medium-term fiscal objectives of bringing their public debt ratio down to more comfortable levels. The IMF’s Fiscal Monitor estimates that those that need to make the most progress on deficit reduction are almost two-thirds of the way there—with the exception of Japan.

This does not mean that the last mile will be the easiest. To understand how difficult the remaining effort could be, we drew from past experiences with fiscal consolidation and constructed an index that measures “fiscal difficulty.” The index can be used to gauge the relative difficulty for countries under various fiscal adjustment scenarios. We looked at two things:

It’s clear from the chart that—at least for most countries—maintaining budget surpluses for the extended period of time required to bring debt ratios down is the most challenging, as “adjustment fatigue” creeps in. This is particularly relevant in Europe, where economic growth remains weak, and only adds further pressure to an already constrained budget.

Emerging market economies: mounting budget pressures

Fiscal vulnerabilities have been increasing in emerging market economies during the last couple of years. This is mostly due to two factors. First, the interest rate and growth environment has deteriorated. Growth forecasts have been revised down by as much as 1¾ percentage points on average, and borrowing costs have increased, especially in Asia and in the Middle East and North Africa. Second, deficits have widened and debt ratios increased in many countries as they—in most cases, appropriately—let automatic stabilizers operate and used fiscal stimulus to contain the impact of the global crisis. In some countries, quasi-fiscal activities such as subsidized lending by state-owned banks or off-budget activities by local governments and other public institutions have added to vulnerabilities.

That being said, the severity of the fiscal challenge varies across the emerging world: some countries have high debt and deficits, and thus pressing consolidation needs; in others, rising risks put more emphasis on initiating the consolidation process; still others remain in a relatively comfortable fiscal position. But overall, the scope for short-term discretionary fiscal action has but evaporated. And continued demands for more and better public services in the developing world raise significant medium-term challenges.

If fiscal adjustment is the order the day across most of the globe, countries must more than ever make sure they tax as efficiently, fairly, and effectively as they can. The second part of the Fiscal Monitor looks in detail at how that can be done—and that will be the topic of another blog in a few days.

[youtube=http://www.youtube.com/watch?v=bzSnrWmrNb8&w=420&h=315]