As the financial market turbulence of May 2013 demonstrated, the timing and management of the U.S. Fed exit from unconventional monetary policy is critical. Our analysis in the latest Global Financial Stability Report suggests that if the U.S. exit is bumpy (Figure 1), although this is a tail risk and not our prediction, the result could lead to a faster rise in U.S long-term Treasury rates that impacts other bond markets. This could have implications not only for emerging markets, as widely discussed, but, also for other advanced economies.

Indeed, historical episodes show that sharp rises in US treasury rates lead to increases in government bond yields across other major advanced economies.

Some facts

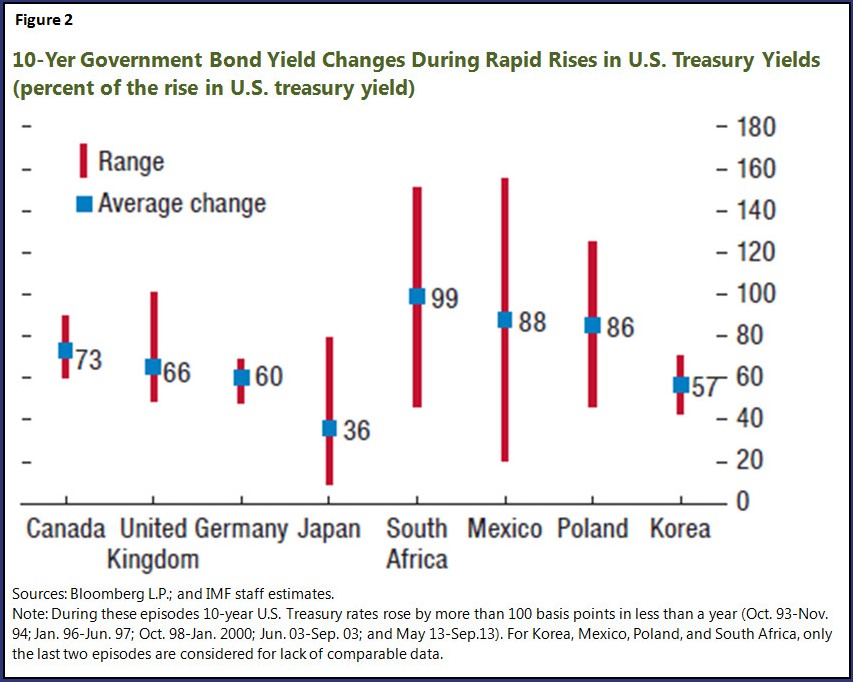

During the last five episodes when 10-year U.S. Treasury rates rose rapidly, bond yields rose, on average, by 73 basis point in Canada, 66 basis points in the United Kingdom, 60 basis points in Germany, and 36 basis points Japan, for every 100 basis point rise in the U.S. Treasury rate (Figure 2).

We saw a similar effect when we looked at U.S. Treasury rates’ impact on emerging market local-currency bond yields, especially during the selloff in 2013.

Tracking the connection: the term premium is a key channel

Why are long-long term bond yields in advanced economies correlated with U.S. Treasury rates, especially during financial shocks? Why does the correlation vary by country?

To answer these questions, we separated bond yields into two components: expected short rates, which expectations of central bank policy rates determine, and the term premium— the compensation sought by investors for potential losses due to interest rate or inflation risk.

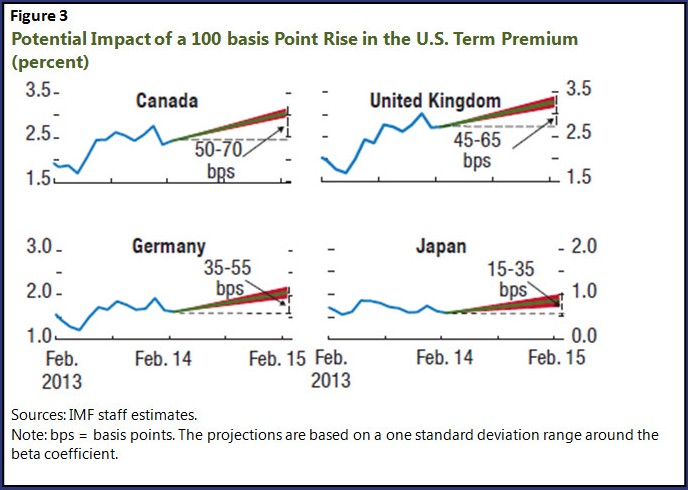

Our analysis showed that the term premium plays a key role in the transmission of U.S. shocks to other countries. We found that even if expected short rates deviated among countries because of differences in country circumstances, the term premium across countries was highly correlated.

Moreover, as with yields, we found the transmission of U.S. term premium shocks to other countries to be the highest for Canada, followed by the United Kingdom, Germany, and Japan. Here’s why.

Closer: for better or for worse

There are two possible explanations for this correlation in term premia.

These two factors could explain why we find a higher correlation of term premium between countries with stronger financial and economic linkages, such as Canada and the United States.

Implications for other countries

These highlight the importance of achieving a smooth exit from unconventional monetary policy in the United States. For more on these and related issues, we encourage you to take a look at the current issue of the GFSR, which discusses factors that could complicate achieving a smooth exit, and implications of a potentially bumpy exit on emerging market economies in more detail.