(Versión en español)

[caption id="attachment_8070" align="alignright" width="200"] photo: Patrick H. Corkery/DoD/Sipa USA/Newscom[/caption]

photo: Patrick H. Corkery/DoD/Sipa USA/Newscom[/caption]

After more than five years of exceptionally low interest rates, the U.S. Fed is getting closer to the point of managing a liftoff of policy interest rates from close to zero. As of today, liftoff is expected to take place by around mid-2015.

But this is not set in stone. The Fed has repeatedly emphasized that the timing will depend on the state of the U.S. economy. If things look better, policy rates may increase earlier. Conversely, weaker than expected data may well mean that interest rates will move up later.

In our view, based on our most recent economic projections, there is some scope for policy rates to stay at zero for a little while longer than mid-2015, given the remaining slack in the labor market and still low inflation.

Moving onto the launchpad

Although the Fed has to deal with multiple areas of uncertainty, the decision of when to move monetary policy onto the launchpad depends on two main factors:

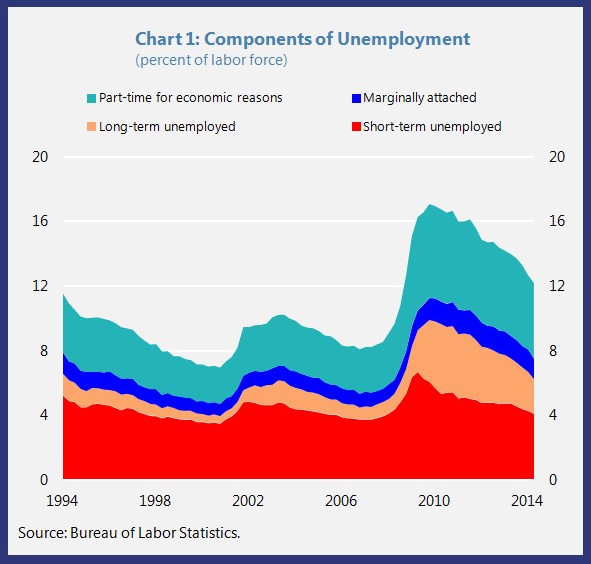

First, how much “labor market slack” there is in the economy. The unemployment rate has declined faster than anyone had expected even a year or so ago. It stood at 6.1 percent in August, which suggests that the economy may soon hit the speed limit created by labor force constraints (see Chart 1). Short-term unemployment is even lower—at 4.2 percent—and below its long-run average. However, there are still almost 3 million Americans who have been jobless for at least 27 weeks, more than 7 million part-timers that would like to work more, and close to 2 million others that have stopped looking for work. This points to more slack in the labor market than the headline unemployment numbers would suggest. At current rates of job growth, it may take 3 or 4 more years for the economy to fully absorb these workers.

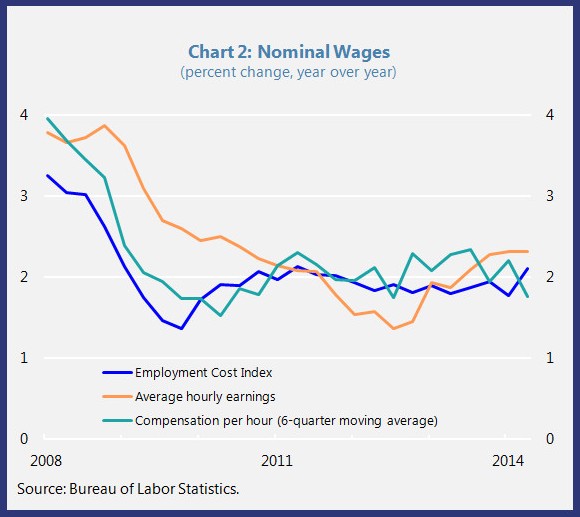

Second, to what extent this slack translates into future wage and price inflation. The Fed’s preferred measure of inflation has been moving up (personal consumption expenditure inflation was 1.6 percent in July) but is still well below the Fed’s 2 percent target. Also, there is little sign of a concerted increase in wage costs, particularly when measured alongside productivity (see Chart 2).

Taken together, this means the Fed can remain patient before proceeding with the countdown toward higher policy rates.

The dark side of the moon

At the same time, keeping policy rates at zero raises the likelihood that financial markets get ahead of themselves and investors start to over-reach. Nobody wants to repeat the financial excesses that led to the Great Recession. Concerns about financial stability may tilt the balance in favor of raising rates sooner rather than later.

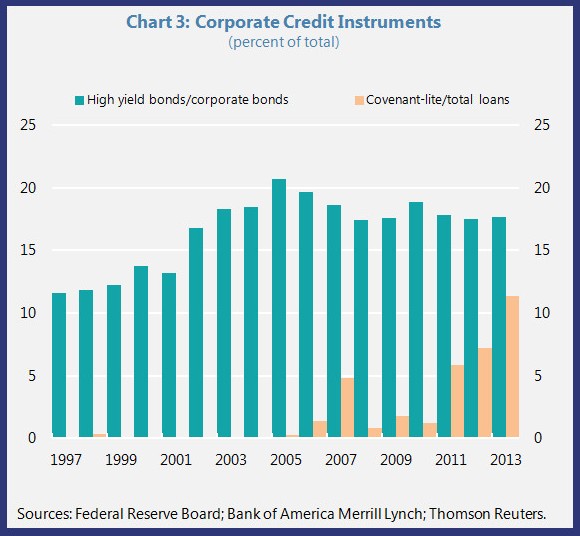

Indeed, there are some vulnerabilities developing in various parts of the financial system and in some sectors, such as lower-rated corporate debt that account for a bit less than a quarter of the corporate bond market, valuations appear stretched, and issuance has been brisk (see Chart 3). The authorities are also monitoring developments in the leveraged loan market and are working to enhance the effectiveness of supervisory guidance as underwriting standards deteriorate.

Linked to the potential frothiness of credit markets, we are also seeing asset managers increasingly investing in some of the riskier and less liquid credit markets. An unexpected reassessment of when and how fast the Fed will raise interest rates or an abrupt unwinding of investors’ current high tolerance for risk could well lead to a rush for the exits and a sudden re-pricing of assets. This would almost certainly have macroeconomic costs both in the United States and abroad.

There is scope to tackle these risks now with macroprudential policies. For example, there could be more demanding underwriting standards for banks that extend intermediate leveraged loans, regulators could tighten the limits on large exposures to riskier assets, prudential rules could be made tougher for regulated entities that hold riskier assets, and actions could be taken to address the mismatch between the liquidity promised to fund owners in good times and the ability of asset managers to provide liquidity in times of stress.

Overall, our current assessment is that monetary policy should remain committed to achieving the Federal Reserve’s mandate of price stability and maximum employment, while macroprudential policies should be the first line of defense against financial excesses, which can threaten systemic stability.

Timing is everything—but so is communication. Certainly, for NASA, the key to a successful mission is highly dependent on a functioning system of communications. The same is true for the Fed’s efforts at guiding the economy onto a stronger growth path. The Fed’s communications toolkit should continue to evolve, as it has done, to update Wall Street and Main Street about how it views the evolution of the economy toward its objectives of full employment with price stability. This could involve more frequent press conferences, a regular monetary policy report that gives the Fed policymakers’ majority view on the outlook, and providing clarity about the role of financial stability in monetary policy decisions.

All in all, timing the liftoff is a tough call to make. It will, inevitably, depend on how well the U.S. economy does in the next several months. While there are tangible risks, we remain optimistic that a solid period of economic growth ahead will facilitate a Fed interest rate lift-off.