(version in Español and Português)

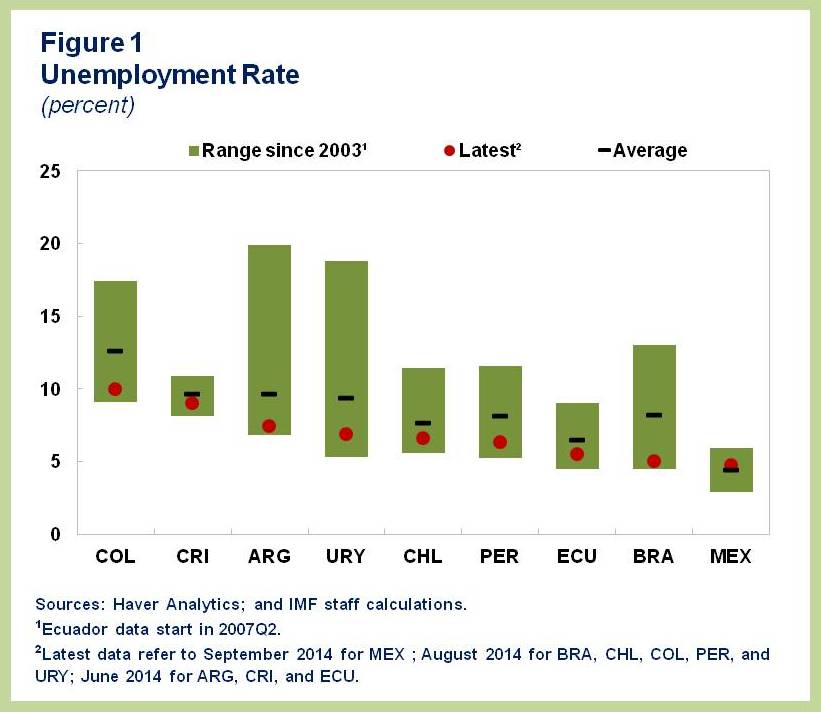

It looks as if labor markets in Latin America have not been following the economic news—literally! Economic activity has slowed markedly in the last three years, with some South American countries slipping into outright recession more recently. Yet, labor markets still appear remarkably strong, with unemployment rates, in particular, hovering at record-low levels in most countries (Figure 1). So, what is going on? Has the region discovered how to defy the law of gravity?

To analyze this apparent disconnect, we first scrutinize recent labor markets developments in more depth. We then assess to what extent these developments really deviate from historical patterns. Overall, we find that labor markets are not as strong as they appear, and their behavior can in fact be reconciled with the weakness in economic activity.

Some weakening beneath the surface

If we compare the evolution of labor market indicators in the first three quarters of 2014 with the average over 2011-13, we do find signs of weakening conditions across the region (Figure 2). Employment was still growing in 2014 in most countries (left panel), but generally at a softer pace than a few years ago (Uruguay stands out as having seen stronger employment growth more recently). In Brazil, job creation has stalled altogether.

Even the historically low unemployment rates disguise some softening in recent months (middle panel). Specifically, unemployment rates were on a downward path in most countries in the region during 2011-13. This year, though, the record has become more mixed. While unemployment rates have continued to decrease in a few countries (Colombia, Brazil, Mexico, and Peru, though generally at a slower pace), they have started to edge up in several others (Argentina, Chile, Costa Rica, Ecuador, and Uruguay).

To be sure, the recent weakening of labor market conditions does not necessarily imply that these markets already have slack. In most Latin American countries, unemployment remains well below the long-term average or typical estimates of the natural rate (i.e. the rate consistent with non-accelerating inflation). And while real wage growth is slowing in most countries, it is still firmly in positive territory (right panel).

Not that different from historical patterns

Once we found that labor market conditions are indeed weakening, the question is whether we should have expected even greater weakness given the extent of the current economic slowdown.

Our recent Regional Economic Outlook Update addresses this question for the case of Brazil, Chile, Colombia, Peru, Mexico, and Uruguay. We look at country-specific historical relationships between output and employment (a version of the so-called Okun’s Law), and find that employment growth in the four quarters through June 2014 was not stronger than expected for any of these countries (Figure 3, left panel). In fact, job creation fell significantly short of what economic activity would have predicted in some cases (Brazil and Mexico).

Notwithstanding the still low unemployment rates, the change in unemployment dynamics for particular countries over the last year can also be broadly explained by output growth (right panel). The notable exception is Brazil, where by June 2014 the unemployment rate was about 1 percentage point lower than would have been expected given the economy’s sharp slowdown. The reason is a surprisingly large drop in labor participation (by about 1½ percentage points). If this drop in participation were to prove temporary, unemployment could increase rather quickly going forward.

Prospects and policy options

More generally, employment growth is likely to remain subdued for some time, as changes in labor markets typically lag those in the overall economy, and output growth is not expected to revert to the high rates of the “golden decade” anytime soon.

In this context, unemployment rates will probably rise somewhat and real wage growth may well moderate further. The resulting slower growth of aggregate wage income will make it increasingly difficult to sustain the pace of poverty reduction and other social achievements observed in previous years.

What can be done? The overwhelming priority across the region is to rekindle economic growth while preserving macroeconomic stability. Given that economic slack is still limited in most Latin American countries, there is little scope for demand-side stimulus, even less so in economies with weak fiscal balances.

Instead, the focus should be on reforms to foster higher productivity and create better conditions for private investment. Improvements in physical infrastructure, educational systems, and the general business environment are key priorities. Pursuing targeted reforms in these areas is the most promising avenue not only for reviving growth, but also for generating more and better-paid jobs over the medium term.