Economists are paying increasing attention to the link between financial inclusion—greater availability of and access to financial services—and economic development. In a new paper, we take a closer look at exactly how financial inclusion impacts a country’s economy and what policies are most effective in promoting it.

The new framework developed in this paper allows us to identify barriers to financial inclusion and see how lifting these barriers might affect a country’s output and level of inequality. Because the more you know about what stands in the way of financial inclusion, the better you can be at designing policies that help foster it.

We found the lack of financial inclusion contributes to persistent income inequality and slower growth.

Why financial inclusion matters

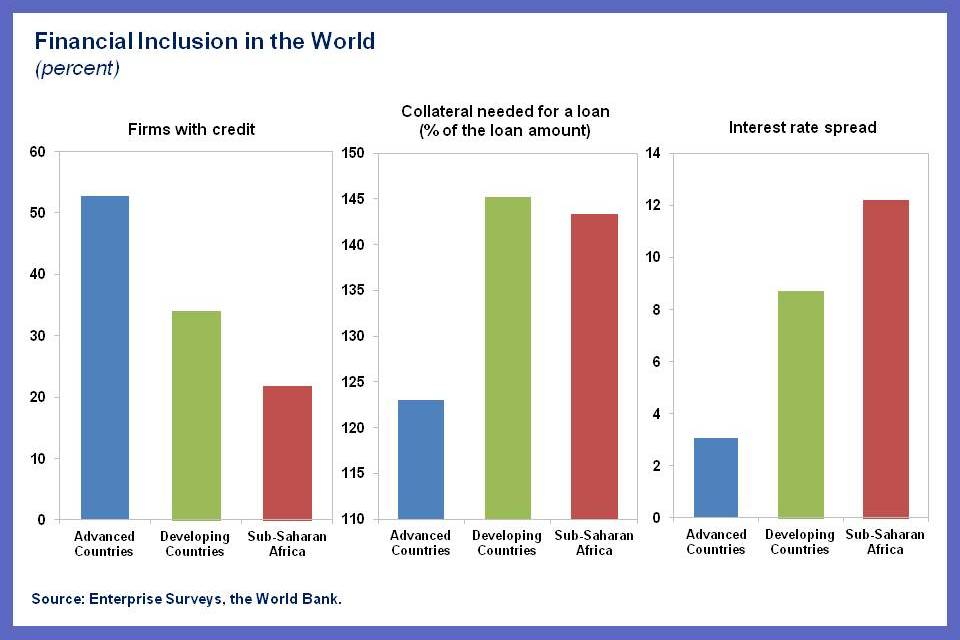

Large gaps exist in worldwide access to finance. Slightly more than half of the firms (58 percent) in developing countries and only one-fifth of those in low-income countries have access to bank credit (Figure 1). Firms—particularly small and medium-sized enterprises—continue to face barriers that further impede access to finance, such as high costs, travel distance, and onerous paperwork. Limited credit, high collateral requirements, and high interest rates also hamper companies’ growth.

What this means, as detailed in our recent work (and in a National Bureau of Economic Research Working Paper), is that individuals must rely on limited savings to become entrepreneurs. Once established, their fledgling enterprises tend to depend on self-financing to meet investment needs. This, in turn, limits the overall size of the firm, the ability to innovate, and productivity.

Examining country cases

To examine how best to increase financial inclusion, we applied our framework to three low-income countries: Kenya, Mozambique, and Uganda. We also applied it to three emerging market countries: Egypt, Malaysia, and the Philippines. Here’s what we found:

- Disentangling constraints to financial inclusion is crucial. We identified pertinent constraints to financial inclusion in these countries and evaluated the policy impact of relaxing these constraints on output and inequality. We found that the impact of financial inclusion policies really depends on country-specific characteristics.

For example, Uganda’s output is most responsive to a relaxation of collateral requirements, which is the country’s most binding constraint. By contrast, high participation costs for access to financial services are a major obstacle in Malaysia. Understanding the specific factors that hold back financial inclusion, therefore, is critical for tailoring policy advice.

- Financial inclusion doesn’t necessarily bring more equality immediately. We found that financial inclusion undoubtedly brings an increase in output, though the impact on inequality measured in relative terms (income dispersion) varies. For example, a decline in the cost of accessing financial services reduces income inequality as enterprises previously excluded from the financial system are able to obtain credit and workers receive higher wages.

Relaxing collateral requirements, however, may initially increase inequality. As wealthy firms invest with less collateral to get loans, they can leverage more and increase their production and profit. As banks lower collateral requirements, however, financial inclusion eventually becomes more beneficial for relatively poorer agents, driving down inequality.

- Distributional consequences could be sharp. The consequences of increased financial inclusion can be uneven. Our results indicate that the most effective policy for increasing access to finance— lowering the cost of participation in the financial system—benefits the poor, but wealthy firms can lose somewhat as a result of higher interest rates and wages.

By contrast, we found that policies that target financial depth— such as relaxing collateral requirements—benefit productive firms. Yet such policies also can impose losses on less productive firms as well as those with low credit demand, regardless of whether financial inclusion policies are in effect.

Policy implications

As we see in the six case studies highlighted here, there is no one-size-fits-all policy prescription for increasing financial inclusion. A key first step is to develop appropriate legal, regulatory, and institutional frameworks and a supporting information environment.

The government has a central role to play in dismantling obstacles to financial inclusion by introducing laws that protect property or creditor rights and ensuring that these laws are adequately enforced. It can also set standards for disclosure and transparency and promote credit information-sharing systems and collateral registries. More fundamentally, it has a role in educating and protecting consumers.

Governments could also consider policies such as granting exemptions from onerous documentation requirements, allowing correspondent banking, and shifting to the use of electronic payments into bank accounts for government payments. All these would help expand firms’ access to finance. By moving forward with these policy measures, governments can make big inroads into increasing financial inclusion, reducing inequality, and boosting growth.

More to come

Because of the growing recognition of the importance of financial inclusion, we are increasingly applying this framework in other emerging market and low-income countries. We have over 20 country studies completed or in progress, including Colombia, Costa Rica, El Salvador, Guatemala, Honduras, India, Nicaragua, Nigeria, Paraguay, Panama, Peru, Uruguay, the Economic Community of Central African States, and the Democratic Republic of Congo, Nigeria, and Zambia.

Stay tuned for future work on this topic.