If financing is the lifeblood of European small businesses, then the effect of the financial crisis was similar to a cardiac arrest. The flow of affordable credit from banks was choked off and small and medium-sized enterprises (SMEs) were hit hardest. Today, with bank lending still recovering from that shock, smart policy actions could open up securitization as a source of financing to help small businesses start up, flourish and grow.

SMEs are vital to the European economy. They account for 99 out of every 100 businesses, two in every three employees, and 58 cents of each euro of value added of the business sector in Europe. Improving access to finance would therefore not only revive small businesses, but also support a strong and lasting recovery for Europe as a whole.

Europe’s small businesses rely heavily on banks for credit. In 2014, more than two-thirds of SMEs in Europe used bank financing, while less than one fifth used non-bank financing sources, such as equity and debt securities (Chart 1). This dependence makes them vulnerable to banking sector difficulties. When the crisis hit, banks raised interest rates and rationed credit to SMEs more tightly than for larger firms.

Quick and lasting gains

Greater use of securitization could yield both quick wins and lasting gains as European Union countries move toward more integrated capital markets. It could help SMEs attract non-bank funding, since banks would sell securitized loans to investors. And from the perspective of banks, the process would free up capital to support new lending.

In the long run SMEs will also need direct access to bond markets, private equity, and venture capital. But the scope to mobilize additional funding now through securitization is considerable, given the large existing stock of SME loans. The combined stock of outstanding SME securitization in Germany, France, Italy and Spain was €57 billion in mid-2014, compared to banks’ outstanding SME loans of €849 billion. In other words, just above five percent of SME loans are currently securitized.

Ensuring safe securities

The subprime mortgage crisis in the United States has given securitization a bad reputation. Yet, securitization in Europe has been remarkably resilient. The default on European securitization instruments has ranged between 0.6 to 1.5 percent. It has been even lower—0.1 percent—for securities backed by SME loans.

Past performance is, however, no guarantee of future performance. Policymakers need to limit risks further by encouraging simple, transparent, and prudently-structured securitization instruments. In a recent paper, we proposed a definition of High-Quality Securitization (HQS) to distinguish such safe instruments. To qualify for the HQS label, securitization instruments should need to meet strict rules on asset eligibility and quality, and be subject to rigorous disclosure and reporting requirements (see annex in the paper). For SME securitization, there would be specific requirements to mitigate the underlying risks associated with SME loans.

Policy action is needed across several fronts to boost the SME securitization market. Many reforms are already in the pipeline, as European Union countries take steps towards building a Capital Markets Union. (See the recent European Commission Green Paper.)

- Recognizing high quality. Regulators should treat transparent, prudently-structured HQS more leniently than opaque, complex forms of securitization. European Union efforts are moving in this direction, but regulators need to settle on a uniform definition for HQS and then apply it consistently across all European Union financial regulations.

- Better infrastructure. Credit reporting should be harmonized and steps taken towards a functional convergence of debt enforcement regimes across European Union countries. This would bring down the cost of securitizing SME loans and encourage cross-border investments.

- Targeted official support. Several European Union initiatives support SME securitization—the European Investment Fund’s standing facility for credit enhancements, the European Union SME Initiative, COSME, and the European Fund for Strategic Investment. Integrating them would boost their catalytic role. To jumpstart the market, the European Investment Bank could act as a strategic investor. Finally, recognition of HQS as collateral for Eurosystem liquidity operations could help develop a deep and liquid securitization market.

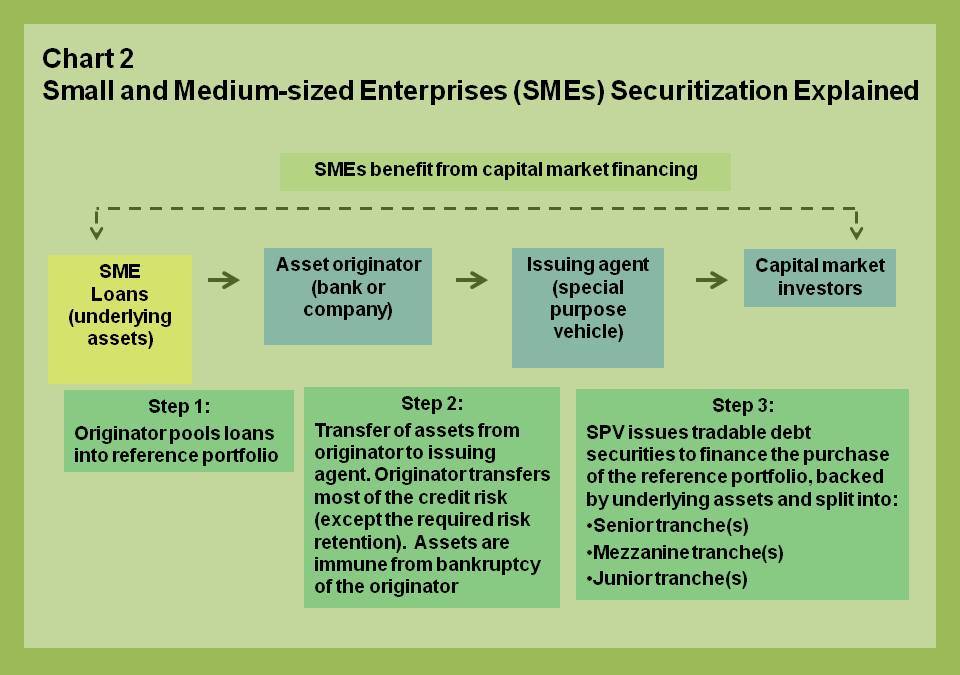

How SME securitization works

Securitization is the process in which certain types of income-producing assets are pooled so that they can be repackaged and sold to investors. (See also a Finance and Development article on “What is Securitization?”)

Through securitization, SMEs can indirectly tap capital market funding (see Chart 2). A bank holding SME loans can pool these loans into a ‘reference portfolio’ (Step 1), and sell it to an issuer (Step 2), such as a special purpose vehicle. By doing this, the bank passes on most of the credit risk of the SME loans to the issuer and frees up capital on its balance sheet for new lending.

The issuer finances the acquisition of the portfolio by selling tradable securities to capital market investors (Step 3). The investors receive interest payments funded by the cash flows generated from the SME loans in the reference portfolio. Since the portfolio assets are detached from the bank’s balance sheet (and its credit rating), issuers can raise funds more cheaply than would be possible on the strength of the bank’s balance sheet alone.

Slicing the securities into “tranches” helps the issuer tailor the risk-return properties to the risk tolerance of different investors, thereby reaching a broader group of backers.