As China’s economy slows and rebalances, its impact is being felt on an already fragile global economy, and particularly in the rest of the Asia region. Our recent studies show that while China’s rebalancing will adversely affect some Asian economies, it will also open opportunities for several others.

A significant partner

Because of its sheer size and integration into the global economy, China’s transition will certainly affect those around it. China is now the top trading partner of most major economies in the region, particularly in East Asia and the Association of Southeast Asian Nations (ASEAN). During 2000–15, exports to China increased dramatically from 3 percent to 9 percent of world exports and from 9 percent to 22 percent of Asian exports. According to IMF staff calculations, a 1 percentage point change in China’s real GDP growth is estimated to affect the real GDP growth of the median Asian economy by 0.15–0.30 of a percentage point.

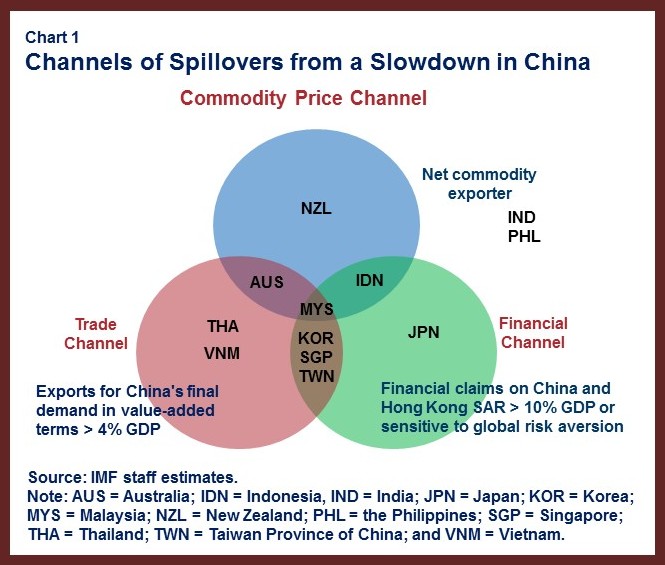

Against this backdrop, some countries have felt the pinch. As China’s economy moves away from investment, its demand for raw materials used intensively in related activities, such as iron ore, copper, and coal, is declining contributing to lower commodity prices. Commodity exporters such as Australia, Indonesia, Malaysia, and New Zealand are likely to be hard hit.

Beyond that, those economies that have been closely integrated with China through the global value chains, and which are heavily exposed to China’s investment activity, such as Korea and Taiwan Province of China, will be affected. Suppliers of technology like Japan and Korea, and providers of capital, such as Hong Kong and Singapore, will also feel the pain.

Finally, financial connections are also growing. Financial spillovers from China to regional markets are on the rise, in particular in equity and foreign exchange markets, driven by greater trade links with China (see Chart 1). In addition, several economies, such as Korea, Singapore, and Taiwan Province of China, have significant financial links with China, both directly and through Hong Kong. Overall, financial markets are likely to become more sensitive to shocks from China as these links develop further, including with the ongoing internationalization of the renminbi and China’s gradual capital account liberalization.

New opportunities for some countries

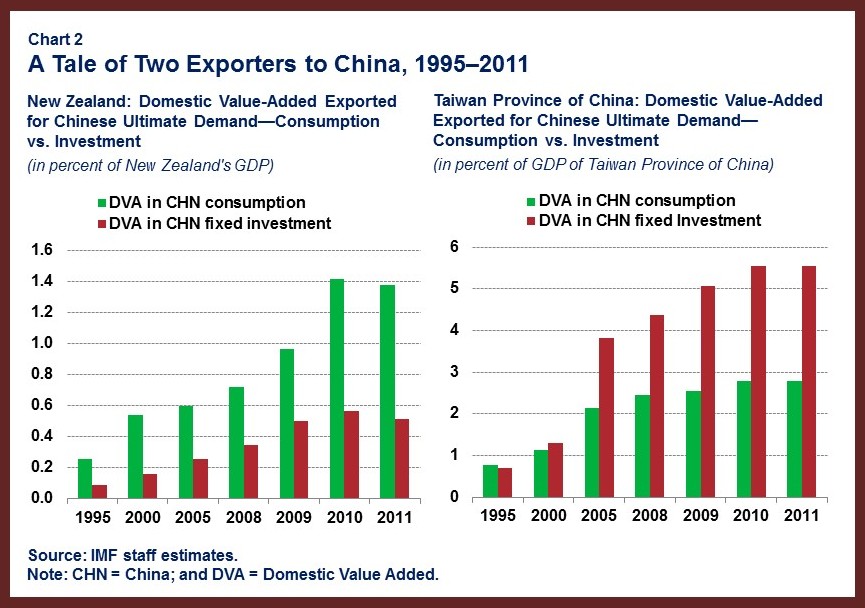

Still, China’s rebalancing also presents opportunities for several economies in the region. Countries that export consumer goods to China, such as New Zealand (higher end food), or that are destinations for rapidly-growing Chinese tourism, could benefit (see Chart 2).

China’s efforts to move to higher value-added production will also provide opportunities for low-income Asian countries, particularly in labor-intensive manufacturing sectors, such as apparel, footwear, furniture, and plastic toys. Already, Bangladesh, Cambodia, and Vietnam have captured some of the global market share in these sectors.

Adapting to change

As China moves to become a service economy, the region will need to adapt. Here are three things countries could do:

- Countries need to diversify their economies and look for new engines of growth, including through deeper trade (and financial) integration. Promoting the growth of the services sector can help, both as a response to China’s rebalancing and as a new source of growth while the region reduces its reliance on manufacturing and exports. Structural reforms, aided by growth-friendly fiscal policy, should support economic transitions, while boosting potential growth and alleviating poverty.

- With inflation low across most of the region, monetary policy should remain supportive of growth. At the same time, exchange-rate flexibility should be part of the risk-management toolkit. Flexible exchange rates have provided and will continue to provide an effective cushion, barring a trade-off with external stability. Countries with adequate fiscal space can use fiscal policy to help smooth the adjustment.

- Countries need to safeguard financial stability, especially if volatile asset prices and exchange rate movements increase vulnerabilities, including in the corporate sector. Measures could also include capital flow management to guard against sudden and large-scale cross-border capital flows associated with large external shocks.

Over time, though, as economic rebalancing makes China’s growth model more resilient and sustainable, its Asian neighbors will benefit. But in the meantime, some of them should expect to feel the effects of China’s rebalancing and be prepared to brace for change.