May 30, 2017

Version in 中文 (Chinese), 日本語 (Japanese)

Policy uncertainty remains a challenge in Japan, and can harm the country’s economic performance according to a new IMF study. The good news is that credible plans for taxation, spending and structural reforms, as well as greater clarity about monetary policy can reduce uncertainty.

Japan’s efforts over the past two decades to reinvigorate growth, lift wages, and minimize the risk of deflation have proved a challenge. Despite a clearer policy direction following the 2012 election of Prime Minister Shinzo Abe, confidence in ‘Abenomics’—his economic reform initiative to boost Japan’s economy—has at times wavered. Previous studies suggest that high uncertainty can discourage investment, slow hiring and prompt firms to opt for part-time workers.

Our new working paper looks at policy uncertainty and its relationship to economic performance in Japan from January 1987 onwards. We develop five new indices—one for overall economic policy uncertainty in Japan, and four others that focus on uncertainty about fiscal policy, monetary policy, exchange rate policy and trade policy. Each index reflects the frequency of articles that contain certain terms pertaining to the economy, policy matters and uncertainty in four major Japanese newspapers: Yomiuri, Asahi, Mainichi, and Nikkei.

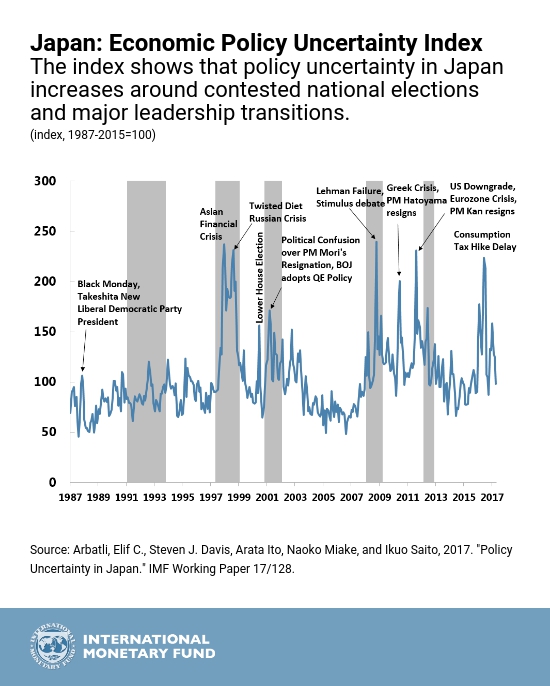

Our overall index shows that policy uncertainty increases around contested national elections and major leadership transitions. The index peaks during the Asian financial crisis and in reaction to the failure of US investment bank Lehman Brothers in September 2008, the resignation of Prime Minister Kan and the US debt-ceiling fight in 2011, the Brexit referendum in June 2016, and the recent deferral of a hike in Japan’s consumption tax rate. We also find that surprise increases in policy uncertainty foreshadow deteriorations in Japan’s macroeconomic performance. This evidence, as well as evidence in other studies, suggests that credible policy plans and better communication can lift economic performance by, in part, reducing policy uncertainty.

Fiscal matters are the leading source of policy uncertainty in Japan

While the proximate sources of policy uncertainty vary over time, we find that issues related to taxation and spending matter most for Japan. Among all news articles that satisfy the criteria for our overall economic policy uncertainty index, 57 percent reference fiscal policy matters, 27 percent reference monetary policy, 8 percent reference trade policy, and only 3 percent reference exchange rate policy.

Shinzo Abe’s election as Prime Minister in December 2012 and Abenomics marked an important milestone and a clearer policy direction. However, maintaining confidence in Abenomics has proved difficult. Fiscal policy targets are no longer seen as credible. For instance, the consumption tax hike initially scheduled for 2015, has now been postponed twice.

The Role of Global Factors

Policy uncertainty is not limited to domestic policy considerations. Global factors, too, contribute to policy uncertainty in Japan. For example, the Brexit referendum and the US presidential election triggered higher policy uncertainty in Japan, captured most visibly by the 140 percent jump in our Japan trade policy uncertainty index in 2016 relative to its average in 2014-15. Our overall Japan economic policy uncertainty index rose by 56 percent in 2016 compared to its average in 2014-15.

Policy uncertainty and economic performance

While it is hard to establish causal effects, our evidence favors the view that high policy uncertainty slows investment, hiring and growth. Our findings suggest that high policy uncertainty undermines macroeconomic performance by acting as an impulse behind fluctuations, or as a mechanism which amplifies and propagates shocks originating elsewhere, or both.

This means that credible policy plans and strong policy frameworks can favorably influence macroeconomic performance by reducing policy uncertainty.

For Japan, credible plans to follow through on structural reforms in product and labor markets would be helpful. Reforms to boost the employment of women and the elderly make especially good sense, given Japan’s aging population and the large share of working-age women not in the labor force. Clarifying the direction of trade policy is another priority, given the lost enthusiasm for the Trans-Pacific Partnership in the United States. A concrete and credible plan to tackle Japan’s long-term fiscal sustainability seems critical. With respect to monetary policy, better forward guidance and other efforts to improve the Bank of Japan’s communications framework would be welcome.