The Czech Republic exports only a small number of cars and car parts directly to the United States, but it’s likely to suffer significant economic damage if that country were to impose tariffs on auto imports. The reason: the Czech Republic supplies parts that are used to build cars exported by other European countries.

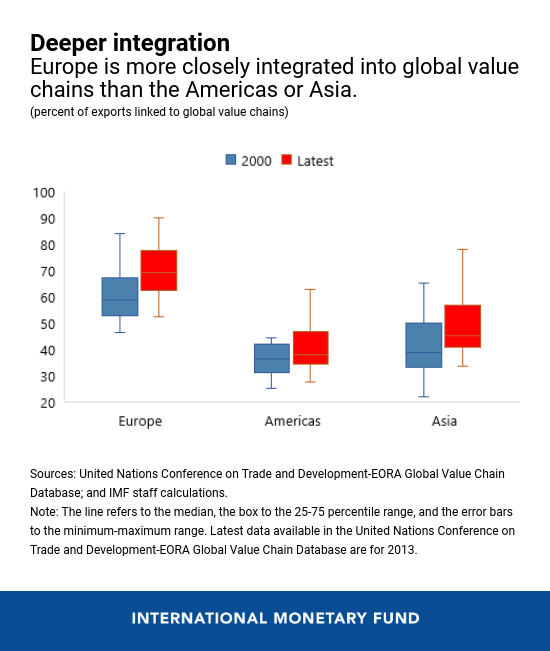

Europe’s auto industry is one of many that are part of global value chains, in which different stages of manufacturing are dispersed among several countries. Because almost 70 percent of European exports are linked to value chains, tariffs imposed on products shipped by one country can affect many others. That is why, as we explain in a recent study, it’s important to view manufacturing through the prism of value chains when assessing the potential economic impact of tariffs or other economic shocks.

We need to distinguish between two yardsticks: gross value and value added.

Two yardsticks

To do that, we need to distinguish between two yardsticks: gross value and value added. When a German resident buys a Volkswagen shipped from a factory in Bratislava, the purchase is recorded in gross terms as a Slovak export to Germany. But though that car was assembled in Slovakia, engine parts and other components came from third countries that provide a higher share of the value added to the final product than assembly does.

Distinguishing between traditional gross export measures and valued-added exports is especially important for Europe because the difference between the two is large; exports of other European countries to Germany are 8.3 percent of GDP in gross terms but only 2.9 percent of GDP in value-added terms.

To understand the importance of value-added measures, consider a scenario in which the United States imposes a 25 percent tariff on imports of cars and car parts. Gross exports of cars and parts from the European Union to the United States are 0.3 percent of EU GDP. The subsequent output loss for the EU is estimated at 0.1 percent of GDP, taking supply chain linkages into account. But only half the impact is in sectors and countries directly affected. The rest is transmitted via other sectors and trading partners along supply chains. Losses are distributed across more European countries than gross export data would suggest.

Let’s return to the case of the Czech Republic. Its direct exports of cars and parts to the United States are negligible in gross value terms. But in value added terms, the Czech Republic would rank fourth among European economies most hurt by car tariffs.

Our study also looked at how a big change in the pace of growth in the United States, China, or Germany—the three world trade hubs—would affect Europe through value chains. Our main conclusion was that growth spillovers from the United States and China are sizable, with larger effects on economies that are more exposed to them in terms of value-added exports.

On the other hand, we estimated that a growth shock that originates in Germany would have a smaller impact. This probably reflects the German economy’s smaller size relative to the United States and China. Also, Germany’s open and diverse economy is relatively resilient, so it was not a major source of independent shocks in the post-1995 period that we analyzed. Still, Germany could transmit shocks originating elsewhere, and its impact might be larger if growth were to be driven more by domestic demand. That was the case during the period around the reunification of East and West Germany in 1990.

These findings could be helpful for policymakers: measuring exports through value-added indicators gives a more precise picture of the distributional impact of potential trade shocks. And a better understanding of how trade shocks propagate through value chains could help formulate offsetting measures as well as policies to help the people who most likely to be affected.