US business investment has been on the rise. Since the passage of the Tax Cuts and Jobs Act at the end of 2017, US businesses have bought more machinery, developed software, and created new intellectual property.

Some believe that the key to this growth in business investment has been the Act’s cut to the corporate tax rate from 35 percent to 21 percent, which lowered the cost of capital. Lower capital costs could, at least theoretically, encourage business owners to increase investment.

But our recent study suggests a simpler reason: business investment has been rising because domestic demand and sales have been rising. We also find that rising market power—the ability of companies to charge prices above production costs—has dulled the impact of corporate tax cuts on business investment decisions.

Business investment has been rising because domestic demand and sales have been rising.

Investment drivers

Growth in sales and optimism about future sales prospects are central forces influencing companies to invest more.

For example, if a business owner expects that she’ll continue to have strong sales in the next quarter, she is more likely to increase investment in her business and boost production.

According to our study—released in the lead up to our recent economic assessment of the United States—virtually all of the growth in business investment since 2017 can be explained by private sector expectations of the future demand for products.

To measure expectations of future product demand, we used private-sector forecasts of US growth in domestic consumption and net exports—that is, the non-investment part of output.

As future sales prospects played a key role in influencing business owners to invest more, what drove consumers to spend more?

The factors that boosted demand in 2018 included households’ higher disposable income due to the tax law’s cut in personal taxes, as well as higher government spending due to the Bipartisan Budget Act of 2018. Other factors, such as reductions in the cost of capital from the lower business tax provisions, appear to explain little of the rise in investment.

Rising corporate market power

Then, what could explain this relatively muted response of investment to a reduction in the effective corporate tax rate?

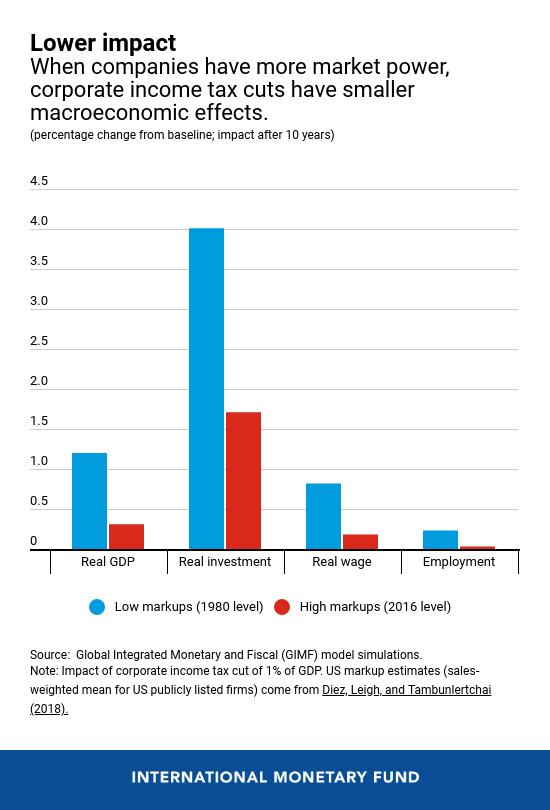

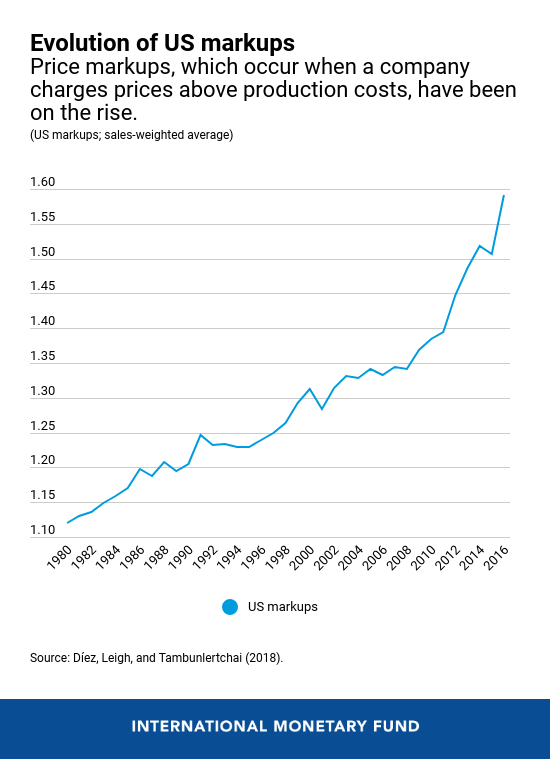

Our analysis suggests that the sensitivity of investment to tax changes may have declined over the past 30 years because of the rise in the market power of big companies, which, other studies suggest, has occurred across the economy—from airlines to pharmaceuticals to high-tech companies.

As companies gain market power and their respective industries become more concentrated, their profits are increasingly in the form of monopoly rents—well above the normal profits that prevail when there is more competition.

In such an environment, a cut to the corporate income tax rate should increase post-tax monopoly profits but induce a smaller behavioral response in companies’ production and investment decisions.

Therefore, as the chart shows, a tax cut today could be expected to have a smaller impact than in past decades due to the changing nature of the US corporate landscape.

Investment decisions

Enterprise-level data for 2018 also support the notion that rising market power is lessening firms’ sensitivity to tax changes. For listed companies across a range of different US industries,

their increase in investment in 2018 was smaller for firms that had higher markups (the difference between prices and marginal costs) before the tax cuts.

Other factors that have further subdued investment growth since 2017 include, we find, economic policy uncertainty, which has occurred in the context of escalating trade-related tensions between the United States and other countries.

The bottom line is this: strong demand since the passage of the Tax Cuts and Jobs Act has been the principal driver behind corporate investment decisions—not the reduction in the cost of capital coming from the corporate tax cuts themselves.

Moreover, the rise in corporate market power in recent decades appears to have muted the effectiveness of corporate tax cuts as a means for boosting business investment.

Finally, policymakers can support further growth in business investment by reducing economic policy uncertainty, including by resolving trade-related tensions.