Press Briefing

Video

World Economic

Outlook Database

Related Articles

Podcast

Podcast Database

Database Discussion Forum

Discussion Forum Frequently Asked Questions

Frequently Asked Questions Subscribe

SubscribeOrdering

Related Links

World Economic Outlook (WEO) Update

Cross Currents

January 2015

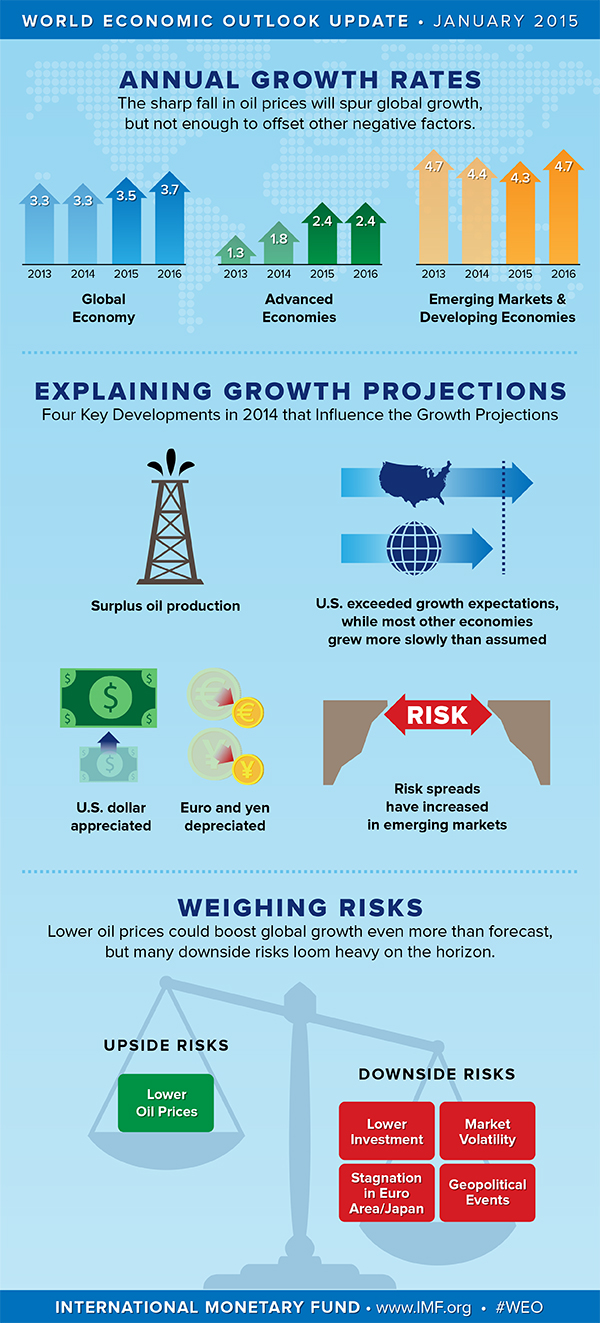

- Global growth will receive a boost from lower oil prices, which reflect to an important extent higher supply. But this boost is projected to be more than offset by negative factors, including investment weakness as adjustment to diminished expectations about medium-term growth continues in many advanced and emerging market economies.

- Global growth in 2015–16 is projected at 3.5 and 3.7 percent, downward revisions of 0.3 percent relative to the October 2014 World Economic Outlook (WEO). The revisions reflect a reassessment of prospects in China, Russia, the euro area, and Japan as well as weaker activity in some major oil exporters because of the sharp drop in oil prices. The United States is the only major economy for which growth projections have been raised.

- The distribution of risks to global growth is more balanced than in October. The main upside risk is a greater boost from lower oil prices, although there is uncertainty about the persistence of the oil supply shock. Downside risks relate to shifts in sentiment and volatility in global financial markets, especially in emerging market economies, where lower oil prices have introduced external and balance sheet vulnerabilities in oil exporters. Stagnation and low inflation are still concerns in the euro area and in Japan.

Four key developments have shaped the global outlook since the release of the October 2014 WEO.

First, oil prices in U.S. dollars have declined by about 55 percent since September. The decline is partly due to unexpected demand weakness in some major economies, in particular, emerging market economies—also reflected in declines in industrial metal prices. But the much larger decline in oil prices suggests an important contribution of oil supply factors, including the decision of the Organization of the Petroleum Exporting Countries (OPEC) to maintain current production levels despite the steady rise in production from non-OPEC producers, especially the United States. Oil futures prices point to a partial recovery in oil prices in coming years, consistent with the expected negative impact of lower oil prices on investment and future capacity growth in the oil sector.

Second, while global growth increased broadly as expected to 3¾ percent in the third quarter of 2014, up from 3¼ percent in the second quarter, this masked marked growth divergences among major economies. Specifically, the recovery in the United States was stronger than expected, while economic performance in all other major economies—most notably Japan—fell short of expectations. The weaker-than-expected growth in these economies is largely seen as reflecting ongoing, protracted adjustment to diminished expectations regarding medium-term growth prospects, as noted in recent issues of the WEO.

Third, with more marked growth divergence across major economies, the U.S. dollar has appreciated some 6 percent in real effective terms relative to the values used in the October 2014 WEO. In contrast, the euro and the yen have depreciated by about 2 percent and 8 percent, respectively, and many emerging market currencies have weakened, particularly those of commodity exporters.

Fourth, interest rates and risk spreads have risen in many emerging market economies, notably commodity exporters, and risk spreads on high-yield bonds and other products exposed to energy prices have also widened. Long-term government bond yields have declined further in major advanced economies, reflecting safe haven effects and weaker activity in some, while global equity indices in national currency have remained broadly unchanged since October.

Developments since the release of the October WEO have conflicting implications for the growth forecasts. On the upside, the decline in oil prices driven by supply factors—which, as noted, are expected to reverse only gradually and partially—will boost global growth over the next two years or so by lifting purchasing power and private demand in oil importers (see box). The impact is forecast to be stronger in advanced economy oil importers, where the pass-through to end-user prices is expected to be higher than in emerging market and developing oil importers. In the latter, more of the windfall gains from lower prices are assumed to accrue to governments (for example, in the form of lower energy subsidies), where they may be used to shore up public finances. However, the boost from lower oil prices is expected to be more than offset by an adjustment to lower medium-term growth in most major economies other than the United States. At 3.5 and 3.7 percent, respectively, global growth projections for 2015–16 have been marked down by 0.3 percent relative to the October 2014 WEO (Table 1).

Among major advanced economies, growth in the United States rebounded ahead of expectations after the contraction in the first quarter of 2014, and unemployment declined further, while inflation pressure stayed more muted, also reflecting the dollar appreciation and the decline in oil prices. Growth is projected to exceed 3 percent in 2015–16, with domestic demand supported by lower oil prices, more moderate fiscal adjustment, and continued support from an accommodative monetary policy stance, despite the projected gradual rise in interest rates. But the recent dollar appreciation is projected to reduce net exports.

In the euro area, growth in the third quarter of 2014 was modestly weaker than expected, largely on account of weak investment, and inflation and inflation expectations continued to decline. Activity is projected to be supported by lower oil prices, further monetary policy easing (already broadly anticipated in financial markets and reflected in interest rates), a more neutral fiscal policy stance, and the recent euro depreciation. But these factors will be offset by weaker investment prospects, partly reflecting the impact of weaker growth in emerging market economies on the export sector, and the recovery is projected to be somewhat slower than forecast in October, with annual growth projected at 1.2 percent in 2015 and 1.4 percent in 2016.

In Japan, the economy fell into technical recession in the third quarter of 2014. Private domestic demand did not accelerate as expected after the increase in the consumption tax rate in the previous quarter, despite a cushion from increased infrastructure spending. Policy responses—additional quantitative and qualitative monetary easing and the delay in the second consumption tax rate increase—are assumed to support a gradual rebound in activity and, together with the oil price boost and yen depreciation, are expected to strengthen growth to above trend in 2015–16.

In emerging market and developing economies, growth is projected to remain broadly stable at 4.3 percent in 2015 and to increase to 4.7 percent in 2016—a weaker pace than forecast in the October 2014 WEO. Three main factors explain the downshift:

• Lower growth in China and its implications for emerging Asia: Investment growth in China declined in the third quarter of 2014, and leading indicators point to a further slowdown. The authorities are now expected to put greater weight on reducing vulnerabilities from recent rapid credit and investment growth and hence the forecast assumes less of a policy response to the underlying moderation. Slower growth in China will also have important regional effects, which partly explains the downward revisions to growth in much of emerging Asia. In India, the growth forecast is broadly unchanged, however, as weaker external demand is offset by the boost to the terms of trade from lower oil prices and a pickup in industrial and investment activity after policy reforms.

• A much weaker outlook in Russia: The projection reflects the economic impact of sharply lower oil prices and increased geopolitical tensions, both through direct and confidence effects. Russia’s sharp slowdown and ruble depreciation have also severely weakened the outlook for other economies in the Commonwealth of Independent States (CIS) group.

• Downward revisions to potential growth in commodity exporters: In many emerging and developing commodity exporters, the projected rebound in growth is weaker or delayed compared with the October 2014 projections, as the impact of lower oil and other commodity prices on the terms of trade and real incomes is now projected to take a heavier toll on medium-term growth. For instance, the growth forecast for Latin America and the Caribbean has been reduced to 1.3 percent in 2015 and 2.3 percent in 2016. Although some oil exporters, notably members of the Cooperation Council for the Arab States of the Gulf, are expected to use fiscal buffers to avoid steep government spending cuts in 2015, the room for monetary or fiscal policy responses to shore up activity in many other exporters is limited. Lower oil and commodity prices also explain the weaker growth forecast for sub-Saharan Africa, including a more subdued outlook for Nigeria and South Africa.

Table 1. Overview of the World Economic Outlook Projections(Percent change unless noted otherwise) | |||||||||||

| Year over Year | |||||||||||

| Difference from October 2014 WEO Projections | Q4 over Q4 | ||||||||||

| Projections | Estimates | Projections | |||||||||

| 2013 | 2014 | 2015 | 2016 | 2015 | 2016 | 2014 | 2015 | 2016 | |||

|

World Output 1/ |

3.3 | 3.3 | 3.5 | 3.7 | -0.3 | -0.3 | 3.1 | 3.4 | 3.9 | ||

|

Advanced Economies |

1.3 | 1.8 | 2.4 | 2.4 | 0.1 | 0.0 | 1.7 | 2.7 | 2.3 | ||

|

United States |

2.2 | 2.4 | 3.6 | 3.3 | 0.5 | 0.3 | 2.6 | 3.4 | 3.2 | ||

|

Euro Area |

-0.5 | 0.8 | 1.2 | 1.4 | -0.2 | -0.3 | 0.7 | 1.4 | 1.4 | ||

|

Germany |

0.2 | 1.5 | 1.3 | 1.5 | -0.2 | -0.3 | 1.0 | 1.7 | 1.3 | ||

|

France |

0.3 | 0.4 | 0.9 | 1.3 | -0.1 | -0.2 | 0.3 | 1.2 | 1.3 | ||

|

Italy |

-1.9 | -0.4 | 0.4 | 0.8 | -0.5 | -0.5 | -0.5 | 0.9 | 0.8 | ||

|

Spain |

-1.2 | 1.4 | 2.0 | 1.8 | 0.3 | 0.0 | 1.9 | 1.8 | 1.7 | ||

|

Japan |

1.6 | 0.1 | 0.6 | 0.8 | -0.2 | -0.1 | -0.3 | 1.6 | 0.2 | ||

|

United Kingdom |

1.7 | 2.6 | 2.7 | 2.4 | 0.0 | -0.1 | 2.7 | 2.7 | 2.2 | ||

|

Canada |

2.0 | 2.4 | 2.3 | 2.1 | -0.1 | -0.3 | 2.4 | 2.1 | 2.1 | ||

|

Other Advanced Economies 2/ |

2.2 | 2.8 | 3.0 | 3.2 | -0.2 | -0.1 | 2.3 | . . . | . . . | ||

|

Emerging Market and Developing Economies 3/ |

4.7 | 4.4 | 4.3 | 4.7 | -0.6 | -0.5 | 4.5 | 4.1 | 5.4 | ||

|

Commonwealth of Independent States |

2.2 | 0.9 | -1.4 | 0.8 | -2.9 | -1.7 | -1.5 | -3.5 | 1.8 | ||

|

Russia |

1.3 | 0.6 | -3.0 | -1.0 | -3.5 | -2.5 | 0.0 | -5.4 | 1.9 | ||

|

Excluding Russia |

4.3 | 1.5 | 2.4 | 4.4 | -1.6 | -0.2 | . . . | . . . | . . . | ||

|

Emerging and Developing Asia |

6.6 | 6.5 | 6.4 | 6.2 | -0.2 | -0.3 | 6.4 | 6.3 | 6.2 | ||

|

China |

7.8 | 7.4 | 6.8 | 6.3 | -0.3 | -0.5 | 7.4 | 6.7 | 6.3 | ||

|

India 4/ |

5.0 | 5.8 | 6.3 | 6.5 | -0.1 | 0.0 | 5.6 | 6.5 | 6.6 | ||

|

ASEAN-5 5/ |

5.2 | 4.5 | 5.2 | 5.3 | -0.2 | -0.1 | 4.6 | 5.1 | 5.5 | ||

|

Emerging and Developing Europe |

2.8 | 2.7 | 2.9 | 3.1 | 0.1 | -0.2 | 2.9 | . . . | . . . | ||

|

Latin America and the Caribbean |

2.8 | 1.2 | 1.3 | 2.3 | -0.9 | -0.5 | 1.1 | . . . | . . . | ||

|

Brazil |

2.5 | 0.1 | 0.3 | 1.5 | -1.1 | -0.7 | -0.3 | 0.1 | 2.2 | ||

|

Mexico |

1.4 | 2.1 | 3.2 | 3.5 | -0.3 | -0.3 | 2.6 | 3.4 | 3.5 | ||

|

Middle East, North Africa, Afghanistan, and Pakistan |

2.2 | 2.8 | 3.3 | 3.9 | -0.6 | -0.5 | . . . | . . . | . . . | ||

|

Saudi Arabia 6/ |

2.7 | 3.6 | 2.8 | 2.7 | -1.6 | -1.7 | . . . | . . . | . . . | ||

|

Sub-Saharan Africa |

5.2 | 4.8 | 4.9 | 5.2 | -0.9 | -0.8 | . . . | . . . | . . . | ||

|

Nigeria |

5.4 | 6.1 | 4.8 | 5.2 | -2.5 | -2.0 | . . . | . . . | . . . | ||

|

South Africa |

2.2 | 1.4 | 2.1 | 2.5 | -0.2 | -0.3 | 1.0 | 1.9 | 2.8 | ||

|

Memorandum |

|||||||||||

|

Low-Income Developing Countries |

6.1 | 5.9 | 5.9 | 6.1 | -0.6 | -0.5 | . . . | . . . | . . . | ||

|

World Growth Based on Market Exchange Rates |

2.5 | 2.6 | 3.0 | 3.2 | -0.2 | -0.2 | 2.4 | 2.9 | 3.2 | ||

|

World Trade Volume (goods and services) |

3.4 | 3.1 | 3.8 | 5.3 | -1.1 | -0.2 | . . . | . . . | . . . | ||

|

Imports |

|||||||||||

|

Advanced Economies |

2.0 | 3.0 | 3.7 | 4.8 | -0.6 | -0.2 | . . . | . . . | . . . | ||

|

Emerging Market and |

5.5 | 3.6 | 3.2 | 6.1 | -2.9 | -0.2 | . . . | . . . | . . . | ||

|

Commodity Prices (U.S. dollars) |

|||||||||||

|

Oil 7/ |

-0.9 | -7.5 | -41.1 | 12.6 | -37.8 | 14.6 | -28.6 | -19.5 | 9.6 | ||

|

Nonfuel (average based on world commodity export weights) |

-1.2 | -4.0 | -9.3 | -0.7 | -5.2 | 0.1 | -7.4 | -4.5 | -0.4 | ||

|

Consumer Prices |

|||||||||||

|

Advanced Economies |

1.4 | 1.4 | 1.0 | 1.5 | -0.8 | -0.4 | 1.4 | 1.0 | 1.8 | ||

|

Emerging Market and Developing Economies 3/ |

5.9 | 5.4 | 5.7 | 5.4 | 0.1 | 0.2 | 5.8 | 6.3 | 5.6 | ||

|

London Interbank Offered Rate (percent) |

|||||||||||

|

On U.S. Dollar Deposits (six month) |

0.4 | 0.3 | 0.7 | 1.9 | 0.0 | 0.3 | 0.3 | 1.1 | 2.6 | ||

|

On Euro Deposits (three month) |

0.2 | 0.2 | 0.0 | 0.1 | -0.1 | -0.1 | 0.1 | 0.0 | 0.1 | ||

|

On Japanese Yen Deposits (six month) |

0.2 | 0.2 | 0.1 | 0.1 | 0.0 | 0.0 | 0.2 | 0.1 | 0.1 | ||

|

Note: Real effective exchange rates are assumed to remain constant at the levels prevailing during December 8, 2014–January 5, 2015. When economies are not listed alphabetically, they are ordered on the basis of economic size. The aggregated quarterly data are seasonally adjusted. | |||||||||||

Risks to the Outlook, Old and New

Sizable uncertainty about the oil price path in the future and the underlying drivers of the price decline has added a new risk dimension to the global growth outlook. On the upside, the boost to global demand from lower oil prices could be greater than is currently factored into the projections, especially in advanced economies. But oil prices could also have overshot on the downside and could rebound earlier or more than expected if the supply response to lower prices is stronger than forecast. Important other downside risks remain. In global financial markets, risks related to shifts in markets and bouts of volatility are still elevated. Potential triggers could be surprises in activity in major economies or surprises in the path of monetary policy normalization in the United States in the context of a continued uneven global expansion. Emerging market economies are particularly exposed, as they could face a reversal in capital flows. With the sharp fall in oil prices, these risks have risen in oil exporters, where external and balance sheet vulnerabilities have increased, while oil importers have gained buffers. In the euro area, inflation has declined further, and adverse shocks—domestic or external—could lead to persistently lower inflation or price declines, as monetary policy remains slow to respond. In many major economies, there are still some downside risks to prospective potential output, which would feed into near-term demand. Geopolitical risks are expected to remain high, although related risks of global oil market disruptions have been downgraded in view of ample net flow supply.

Policies

Weaker projected global growth for 2015–16 further underscores that raising actual and potential output is a policy priority in most economies, as discussed in previous issues of the WEO. There is an urgent need for structural reforms in many economies, advanced and emerging market alike, while macroeconomic policy priorities differ. In most advanced economies, output gaps are still substantial, inflation is below target, and monetary policy remains constrained by the zero lower bound. The boost to demand from lower oil prices is thus welcome, but additional policy measures are needed in some economies. In particular, if the further declines in inflation, even if temporary, lead to additional downdraft in inflation expectations in major economies, monetary policy must stay accommodative through other means to prevent real interest rates from rising. Fiscal adjustment must be attuned in pace and composition to supporting both the recovery and long-term growth. In this respect, there is a strong case for increasing infrastructure investment in some economies. In many emerging market economies, macroeconomic policy space to support growth remains limited. But in some, lower oil prices will alleviate inflation pressure and external vulnerabilities, thereby allowing central banks not to raise policy interest rates or to raise them more gradually.

Oil exporters, for which oil receipts typically contribute to a sizable share of fiscal revenues, are experiencing larger shocks in proportion to their economies. Those that have accumulated substantial funds from past higher prices and have fiscal space can let fiscal deficits increase and draw on these funds to allow for a more gradual adjustment of public spending to the lower prices. Allowing substantial exchange rate depreciation will be the main means available to others to cushion the impact of the shock on their economies. Some will have to strengthen their monetary frameworks to avert the possibility that depreciation will lead to persistently higher inflation and further depreciation.

Lower oil prices also offer an opportunity to reform energy subsidies and taxes in both oil exporters and importers. In oil importers, the saving from the removal of general energy subsidies should be used toward more targeted transfers, to lower budget deficits where relevant, and to increase public infrastructure if conditions are right.

| The Effects of Lower Oil Prices on the Global Economy1 |

|

Lower oil prices due to supply shifts boost global growth, although with important differences between oil importers and exporters. The global economic impact depends crucially on how large and persistent the oil supply shifts are expected to be. The more persistent they are, the more consumers and firms will adjust consumption and production. Given the considerable uncertainty about the impact of lower prices on future oil supply, Arezki and Blanchard (2014) consider two scenarios with different assumptions concerning the supply-related change in the oil price going forward. In the first scenario, 60 percent of the decline in the WEO oil price path through 2019 relative to the one used in the October 2014 WEO is attributed to supply shifts (in other words, the scenario assumes an oil price decline of 22 percent in 2015 and 13 percent in 2019). In the second, the supply shift accounts for 60 percent of the price decline initially, but its contribution will gradually decline to zero by 2019 because of the supply response to lower prices. Under the first scenario, the supply shift lifts global GDP by 0.7 and 0.8 percent, respectively, in 2015–16. In the second scenario, the same initial supply shift implies an increase in global GDP of 0.3 percent in 2015 and 0.4 percent in 2016 relative to what was expected with the oil price path used in the October WEO. These global effects of lower oil prices mask asymmetric effects across countries. Oil importers will benefit from higher real incomes of consumers and lower costs in the production of final goods. Among importers, the oil intensity in consumption and production varies, but the simulations used in the scenario analysis suggest GDP increases between 0.4 and 0.7 percent in 2015 in the case of China and between 0.2 and 0.5 percent in the United States. For many importers, the boost from lower oil prices—while sizable—is somewhat muted by the recent currency depreciation against the U.S. dollar, which implies a smaller oil price decline in domestic currency. In oil exporters, real incomes and profits generally decrease. Much will depend, however, on whether governments, which typically accrue most of the net oil revenue, will adjust spending. In countries with buffers, spending adjustment can be gradual, which would limit the negative impact on incomes and activity. But recent developments in Russia illustrate the potential for a greater impact in oil exporters where macroeconomic policies cannot afford to mitigate the negative growth impact.

|