(Version in Français)

Once again, the latest review of growth prospects for sub-Saharan Africa shows that the region’s economy is in strong health. Growth in the region is set to pick up to 5½ percent in 2014 compared to 4.9 percent last year (see Chart 1). My view is that this growth momentum will continue over the medium term if countries rise to new challenges and manage their economies as dexterously as they have over the past decade or so.

So what explains this continued strong growth performance? Apart from good macroeconomic policies in the region, the growth has been underpinned by investment in infrastructure, mining, and strong agricultural output. And favorable global tailwinds—high demand for commodities and low interest rates—have played a major supporting role.

That said, I do worry about the global shifts that are taking place and what they mean for the region. Unless countries navigate the new environment adroitly, the current growth momentum will slow down considerably.

So what are the downside risks to the otherwise favorable outlook? Let me mention four.

Export demand

First, growth in emerging markets could prove less supportive. If growth in these economies slows down considerably, then export demand will decline, especially for some base metals such as copper and iron ore. Countries such as the Democratic Republic of Congo, Liberia, and Zambia would be particularly hit. At the same time, tighter financial conditions in China could reduce the appetite for Chinese companies investing abroad. China has been a major source of foreign direct investment and infrastructure financing for Africa.

Second, as advanced economies unwind their highly accommodative monetary policies, global financial conditions will become tighter and countries in sub-Saharan Africa could experience a hike in interest rates and a slowdown, or even a reversal, of private capital flows.

But the risks to the growth momentum are not all external.

Security conditions remain difficult in some countries. The conflicts in the Central African Republic and South Sudan are exacting a heavy human and economic toll. At the same time, they are having negative spillover effects for the neighboring countries in terms of lower trade flows and higher security outlays.

I also worry about high fiscal deficits in some countries. Four years after the global crisis, fiscal policy has remained on an expansionary footing despite a recovery in both growth and revenue. I’ll go back to this theme shortly.

Warning signs

The issue of rising fiscal imbalances is worth dwelling on. A number of economic observers have asked the question: are countries heading back to the bad old days of rapid debt accumulation that may need to be forgiven down the line? Are these fears well grounded?

We all applauded when many countries in sub-Saharan Africa in 2009 were able to mitigate the worst effects of the global crisis by actively deploying countercyclical fiscal policy, or at least avoiding fiscal procyclicality. When revenue tanked in the wake of decelerating growth, many countries kept spending up and hence maintained growth. This was quite remarkable as, in all previous global recessions, countries had no option but to do the opposite: cut spending as revenue declined, and hence deepen the impact of the recession.

One concern now is that, five years on, many countries continue to show relatively high deficits despite the fact that growth and revenue have recovered rapidly. To illustrate the point, in the years preceding the crisis (that is, in 2004–08), the region saw a fiscal surplus that averaged about 2 percent of GDP (see Chart 2). Between 2010 and 2013, the average fiscal deficit amounts to some 3 percent of GDP, a deterioration of 5 percentage points compared with pre-crisis levels.

So, what explains the lack of adjustment despite the recovery in growth and revenue? Why has spending kept on growing so fast?

Higher-quality spending

In many cases, increased spending is the result of boosts to public investment and pro-poor spending. And this is exactly what we and others have often been arguing for. After all, the Heavily Indebted Poor Countries Initiative was precisely designed to give countries the necessary fiscal space to undertake socially useful spending in health and education, and rebuild decaying public infrastructure. And, over the long run, higher investment in human capital and infrastructure should raise potential growth sufficiently to pay off the debt, assuming that the quality of spending is high.

The solution to every protruding nail is not to hit it down with a sledgehammer. So deficits of the order of 2–3 percent of GDP are probably not a bad thing, and will not leading to rising debt burdens given that GDP growth rates are much higher.

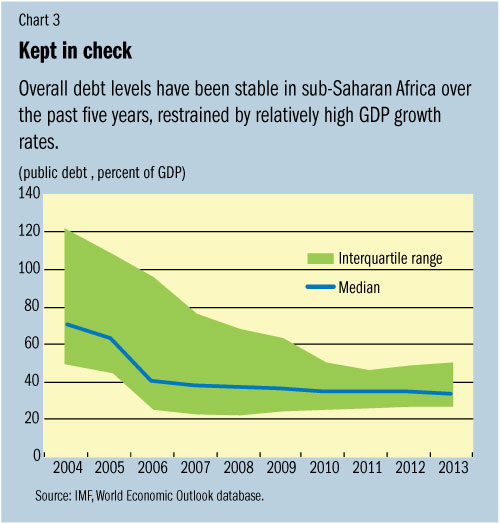

And it is true that overall debt levels are not particularly high as of now, and they have been quite stable over the past five years. Overall, public debt-to-GDP ratios have continued to decline, from a regional average of 37 percent in 2004–08 to some 33 percent in 2010–13 (see Chart 3). Debt burdens have been kept in check by relatively high GDP growth rates.

I am concerned about those countries where fiscal policy has continued to weaken and debt levels have risen rapidly. Particularly vulnerable are countries that depend heavily on portfolio flows to finance their deficits. It stands to reason therefore that to avoid the debilitating effects of a new shock on growth, these countries need to put their fiscal house in order.

Preparing for future shocks

We must first take lessons from the past. Sub-Saharan Africa was able to recover quickly from the effects of the global crisis because most countries started from an already strong position. To utilize perhaps an overused term, they had “fiscal buffers.” They had lowered their deficits and slashed their debt-to-GDP ratios in the preceding years. Now is the time to make hay while the sun shines.

Countries should aim to increase their resilience to shocks, notably by boosting their revenue base and avoiding excessive spending growth. Countries with large fiscal deficits and high or rapidly rising debt levels should intensify efforts to bring public finances on a more sustainable path. Fast-growing countries should take advantage of the growth momentum to strengthen their fiscal balances. And all countries should strive to improve the quality and efficiency of public spending.