Versions in Português (Portuguese) and Español (Spanish)

The rapid increase in Latin American corporate debt—fueled by an abundance of cheap foreign money during the past decade—has contributed to an increase in corporate risk. Total debt of nonfinancial firms in Latin America increased from US$170 billion in 2010 to US$383 billion in 2015. With potential growth across countries in the region slowing, in line with the end of the commodity supercycle, it will now be more difficult for firms to operate under increased debt burdens and reduced safety margins.

In this environment, Latin American firms are walking a tightrope. With external financial conditions tightening, the walk towards the other side—notably through adjustment and deleveraging—while necessary, has become riskier. After making good progress, the crossing has also become more perilous due to strong headwinds—including slower global demand and bouts of heightened market volatility.

In our most recent regional report, and in a companion working paper, we take a deeper look at the factors driving corporate risk in Latin America over the last decade. We use company-specific financial information for close to 500 publicly listed nonfinancial firms between 2005–15 in 7 major economies—Argentina, Brazil, Chile, Colombia, Mexico, Panama, and Peru. We then gauge the main factors driving corporate risk dynamics in the region. We analyze company-specific, country-specific, and global conditions and the factors contributing the most to the recent rise in corporate risk.

Warning signs

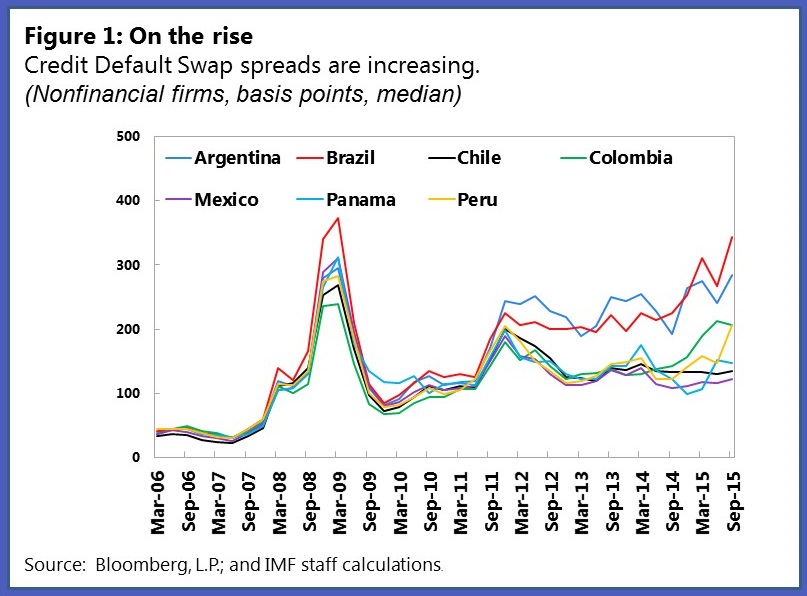

The data shows that corporate risk, as reflected in higher credit default swaps (CDS) spreads, has indeed been rising in 2014–15 (Figure 1), though only in the cases of Argentina and Brazil has it approached the levels observed during the global financial crisis. Interestingly, but not surprisingly, the peak year in most commodity prices (2011) marks the beginning of risk differences across countries, which have further widened since late 2014.

Our results show the following:

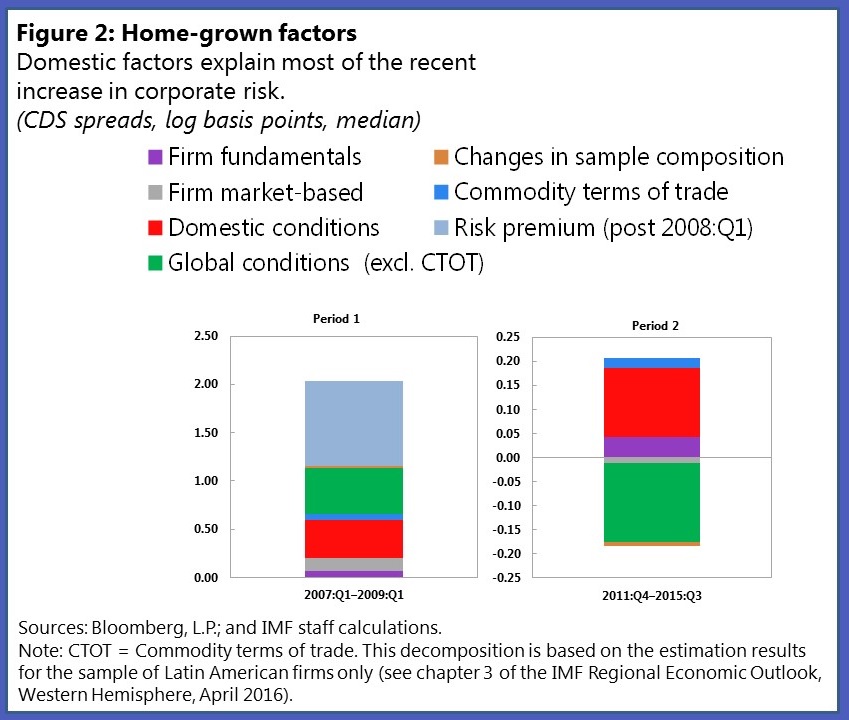

- All dimensions—company-specific, country-specific, and global factors—play a role in driving corporate risk, albeit to varying degrees and with different implications across countries. Overall, macroeconomic domestic factors, particularly the pace of currency depreciation and changes in sovereign spreads, are key direct factors placing upward pressure on corporate risk since 2011 (Figure 2).

- External conditions—in particular measures of global risk aversion (such as the Chicago Board Options Exchange Volatility Index, VIX)—constitute a dominant driver of corporate risk. Stress tests indicate that external shocks can generate substantial increases in corporate risk across the region—ranging from 100 to almost 300 basis points in the event that the VIX surges to just half of the spike observed during the global financial crisis.

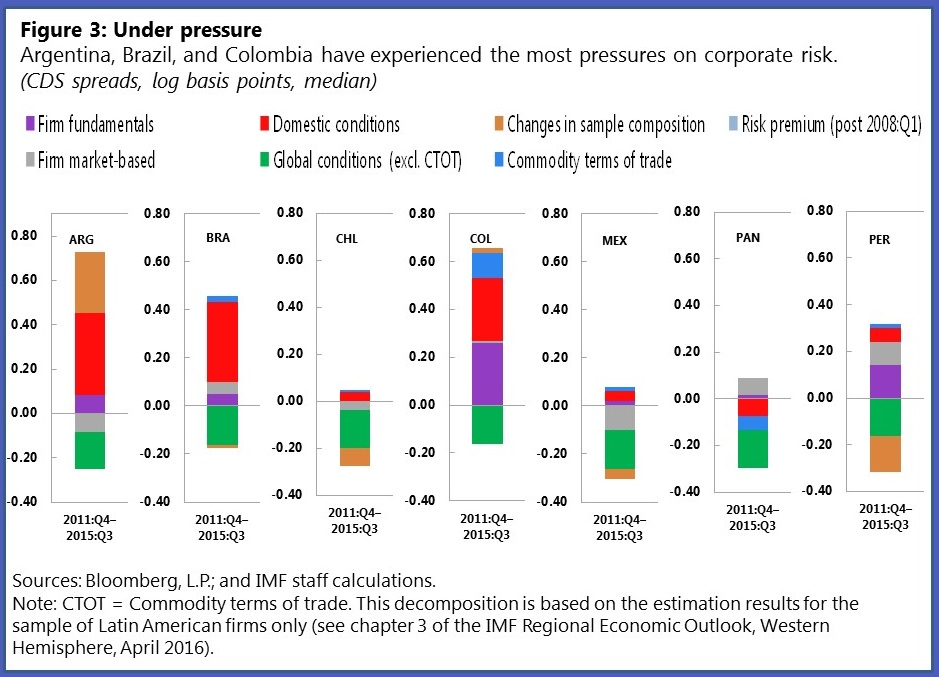

- Domestic macroeconomic and political factors have played a particularly important role in generating upward pressures on corporate risk in Argentina and Brazil through rapid exchange rate depreciation and an increase in sovereign CDS spreads—reflecting significant macroeconomic imbalances (Figure 3). Higher corporate vulnerabilities in Colombia have been driven by the large exchange rate depreciation, as well as deteriorating firm-specific factors. The latter has also generated upward pressure on corporate spreads in Peru. In contrast, Chile, Mexico, and Panama have experienced much lower pressures on corporate risk from domestic economic factors.

- Across these major Latin American economies, benign global financial conditions (in particular, low market volatility) have helped to contain corporate risk despite an environment of slower external demand and declining commodity prices.

Minimizing risk

The soundness of policy frameworks matters for corporate risk. Indeed, given the important link between corporate and sovereign spreads, macroeconomic stability and credible policies are an important defense against additional upward pressures on corporate spreads. For instance, reining in risks to fiscal sustainability as well as curbing inflation, particularly in Argentina and Brazil, is crucial to contain corporate risk.

Recognizing the importance of global factors in driving corporate risk at home, solid macroeconomic policies alone, however, may not be enough and supporting underlying microeconomic adjustments are also imperative. This means promoting firms’ capacity to push through needed adjustments. In particular, orderly deleveraging through market-based solutions should be the first line of defense in highly indebted companies. Public sector equity should not be used to stave off needed adjustments in the corporate sector. In the case of insolvent companies, restructuring and bankruptcy legislation should minimize both administrative costs and economic losses related to default.

Finally, enhanced monitoring and supervision and well-targeted macroprudential policies are key to alleviate risks and spillovers, particularly to the financial system. Policymakers should monitor closely corporate balance sheets and income flows, particularly in systemically important nonfinancial firms. Financial regulators also have a critical role to play. Adequate consolidated supervision, particularly in cases where financial and nonfinancial firms are highly interlinked, remains an important risk-mitigating tool.