August 10, 2017

Versions in 中文 (Chinese), 日本語 (Japanese)

[caption id="attachment_20962" align="alignnone" width="1024"]

Elderly shoppers in Tokyo’s Sugamo district: As Japan's population ages, demand for financial services shifts (photo: Issei Kato/Reuters/Newscom).

Elderly shoppers in Tokyo’s Sugamo district: As Japan's population ages, demand for financial services shifts (photo: Issei Kato/Reuters/Newscom).[/caption]

Japan’s population is shrinking and getting older, posing challenges to the nation’s financial system. How Japan copes could guide other advanced economies in Asia and Europe that are grappling with the same trends but are at an earlier phase of similar demographic developments.

A declining and aging population weighs on growth and interest rates. This puts pressure on profits of banks and insurance companies. Judging how these shifts affect financial firms was part of the IMF’s Financial Sector Assessment Program for Japan, the world’s third-largest economy. The program is a comprehensive and in-depth assessment of a country’s financial sector. It analyzes the resilience of the financial sector, the quality of the regulatory and supervisory framework, and the capacity to manage and resolve financial crises.

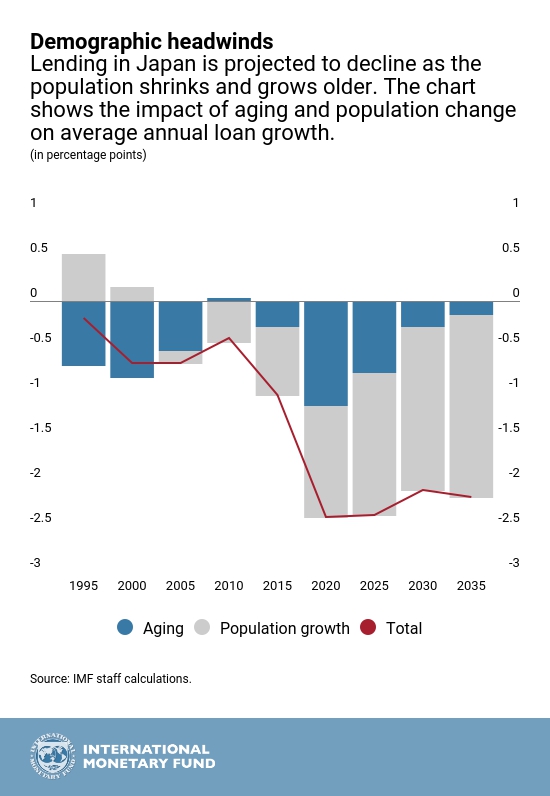

An aging population is also likely to reduce the role of banks in the financial system. With increasing longevity, the demand for longer-term securities rises (since people save more for longer retirements). This results in a flatter yield curve–and banks typically make money by borrowing at low short-term rates and lending at higher longer-term ones. In line with this intuition, analyses of data from 34 countries around the world confirm that the size of the banking sector relative to nonbank financial intermediaries is negatively associated with aging. About 40 percent of the increase in the size of market finance in Japan since 1990 can be explained by aging.

Smaller banks that rely on lending to local markets are particularly vulnerable, since they face less demand from households and firms. Older households still need banking services for transaction purposes, which means that lending will likely fall much faster than deposits. As a result, over the next two decades some regional banks could see their loan-to-deposit ratios fall by 40 percentage points.

In response to profitability problems, banks are also engaging in riskier forms of lending and investment as they search for yield. They have been making more real estate loans, helping to drive up housing prices in some areas despite overall population shrinkage. Condominium prices appear to be moderately overvalued in Tokyo, Osaka, and several outer regions. Banks have also been investing more in securities in countries where economic growth is faster than Japan’s.

Life insurance companies are also facing increasing pressure. They have been putting more money into riskier overseas markets to get the yield needed to meet interest guarantees.

The problem is that many banks and insurers still need to develop the capacity to manage the risks associated with these new types of investments.

Consequently, stress tests suggest that market risks are increasing and that there are some vulnerabilities among regional and shinkin (cooperative) banks and life insurers. Although bank liquidity is generally ample, some of the regional banks are exposed to risks in foreign-currency funding.

The Bank of Japan has had to adapt its monetary policy to low “natural” rates in the economy and sought to stimulate demand by monetary easing. In this context, it had to resort to large-scale asset purchases. These purchases in turn, have put a strain on markets. The level of liquidity—how easily and quickly investors can buy and sell securities—in Japanese government bond markets seems to have been adversely affected by the central bank’s purchases. Moreover, the resilience of government bond market liquidity also seems to have declined as the share of Bank of Japan holdings has increased.

Japan’s financial system has so far remained stable. But there are steps policymakers can take to ensure that it remains sound as society ages and slow growth continues:

- Supervisors need to modernize supervision to keep pace with the more sophisticated activities emerging across banks, insurers, and securities firms. Tailoring capital requirements to individual bank risk profiles and implementing a framework that appropriately recognizes the financial conditions of insurers would be key.

- Corporate governance needs to be strengthened across the banking and insurance sectors to manage new risk taking.

- The macroprudential framework could be further strengthened to better identify and address any buildup of systemic risks.

- Some (in particular regional) banks will feel increased pressure, so they should be encouraged to take timely action in response to viability concerns.

- Regional banks should be encouraged to consider augmenting fee-based income, reducing costs, and consolidating.

- Sustaining productivity growth is a particular challenge as the population ages, and new, innovative firms can play an important role. Constraints to financial access for small and medium enterprises and start-ups should be eased by further promoting risk-based lending. Alternative forms of financing for these young businesses should be further encouraged.

These long-term challenges for business models of many banks, combined with the existence of large systemic institutions, highlight the need for a strong crisis management and resolution framework.