عربي, 中文, Español, Français, 日本語, Português, Русский

How much you need to save for retirement depends on your country’s pension system. Our new research focuses on the interaction between saving and pension systems in an aging world. We use data from 80 countries to map public (government) and private savings in countries over the next 30 years, given their aging populations and the design of pension systems.

We find that trends in private saving drive the development of national saving. Assuming unchanged policies, population aging will drive up public spending on pensions by just over 2 percentage points of GDP by 2050. But the response of households’ private saving differs markedly across countries, with pension system characteristics a major factor determining how much households save. Policymakers need to understand what drives these changes in saving rates, as savings provide a form of insurance against downturns and, by financing investment, stimulate long-term economic growth.

Old enough to know better, young enough to do it anyway

Whether you are a millennial at the beginning of your career, a 40-something who teaches or assembles cars, or self-employed, at some point in your life you will retire.

You may have a good public pension awaiting you in retirement; or the public pension where you live may be meager. Your pension may be determined based on your past wages or it may be in the form of a dedicated pension saving account, like a 401(K) in the United States. When planning your retirement, you would also look at your other savings in bank accounts and, possibly, an investment portfolio.

Public spending on pensions will increase by just over 2 percentage points of GDP by 2050.

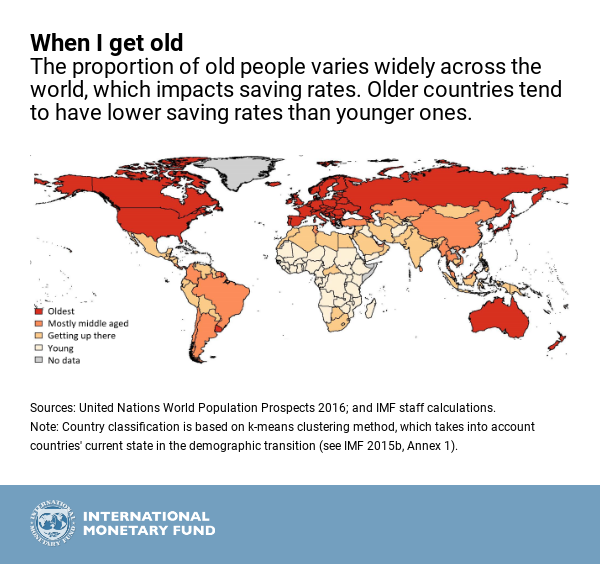

In general, saving behavior varies over a lifetime: the young borrow, prime working age people save, and older people spend their savings after retirement. Aging societies have more elderly people and are likely to see lower aggregate savings. At the same time, longer life spans mean people will need to save more for retirement throughout their working lives.

Your saving behavior matters

Our research shows how developments in private saving drive changes in national saving. In emerging markets and low-income developing countries collectively, relatively young populations lead to increased private saving. In contrast, we expect private saving rates in aging advanced economies to contract sharply. Our study also confirms findings that public spending on pensions will increase in emerging markets and low-income countries, where governments have yet to reform pension benefits.

These aggregates mask substantial differences between countries, driven by the varied designs of pension systems. The most important characteristics are the generosity of a public pension and the presence or absence of dedicated pension saving accounts.

Other things equal, generous public pensions lower both public saving―through more pension spending—and private saving—by reducing the incentive to save as retirees need to rely less on their own savings. Conversely, low public pensions can drive up private saving as they induce people to save more for their mainly self-funded retirement.

For example, Russia and Australia are both aging countries that offer dedicated pension saving accounts. But pensions in Australia are less generous relative to national income. As a result, saving in Australia is projected to increase much faster than in Russia.

Making it easier to save for retirement through dedicated pension saving accounts—such as Individual Retirement Accounts (IRAs) in the United States—helps increase private saving. In countries with such accounts, private saving is projected to increase, in contrast to countries without them.

What can policymakers do?

In countries with generous public pensions, curtailing early retirement or adjusting the size of pension benefits would help address (future) funding shortfalls.

In advanced economies, such reforms have made pensions less generous. For current workers to maintain their living standards in retirement, people will have to work longer and save more.

Our simulations suggest two things that would allow people to retire at a living standard similar to today’s. First, a gradual increase in the retirement age from today’s average of 63 to 68 by 2050—at which time life expectancy is also projected to have increased by some 3 years. Second, saving an additional 6 percent of earnings each year.

Governments can help their citizens by stimulating the development of financial sector instruments to encourage voluntary saving and adopting policies to encourage people to lengthen their productive lives. In emerging markets and low-income countries, they could also further stimulate work in the formal sector.

In some countries, such as China and Korea, however, private saving levels are already very high, while pension and social security systems are relatively weak. Policymakers in these countries should consider increasing pension system generosity. This would reduce households’ need for precautionary saving, while reducing inequality and old-age poverty.

Taken together, these policies can dampen projected declines in national saving, while at the same time improving the sustainability of pension systems and ensuring that people have decent living standards in retirement.