December 18, 2017

Versions in عربي (Arabic), 中文 (Chinese), Español (Spanish), Français (French), 日本語 (Japanese), Русский (Russian)

[caption id="attachment_22181" align="alignnone" width="1024"] On the economic front, 2017 is ending on a high note (photo: allstars/shutterstock).[/caption]

On the economic front, 2017 is ending on a high note (photo: allstars/shutterstock).[/caption]

It has been a tumultuous year marked by natural disasters, geopolitical tensions, and deep political divisions in many countries.

On the economic front, however, 2017 is ending on a high note, with GDP continuing to accelerate over much of the world in the broadest cyclical upswing since the start of the decade.

Here are five charts that help tell the economic story of the past year.

-

One notable aspect of last year’s upswing is its breadth. Growth accelerated in about three quarters of countries—the highest share since 2010. Even more important, some of the countries that had high unemployment for some time, for example, several in the euro area, are participating in the growth surge and experiencing strong employment growth. Some of the larger emerging market economies, such as Argentina, Brazil, and Russia, exited their recessions. Still, in per capita terms, growth in almost half of emerging market and developing economies—especially the smaller ones—lagged behind advanced economies, and almost a quarter have seen declines. Countries that struggled included fuel exporters and low-income economies suffering from civil strife or natural disasters.

-

Boosted by a recovery in investment, global trade growth rebounded from its slowest pace since 2001, other than during the recession of 2009. Weak capital spending in the energy sector had been an important contributor to the weakness in global investment in 2016.

-

Metal and fuel prices were supported by stronger momentum in global demand as well as supply restraints in the energy sector, including hurricane-related stoppages in the United States, financial disruptions in Venezuela, and security problems in regions of Iraq. With futures prices indicating general stability or some moderation in prices going forward, commodity exporters need to continue their adjustment to lower revenues while diversifying their economies’ production and export mixes to build resilience and support future growth.

-

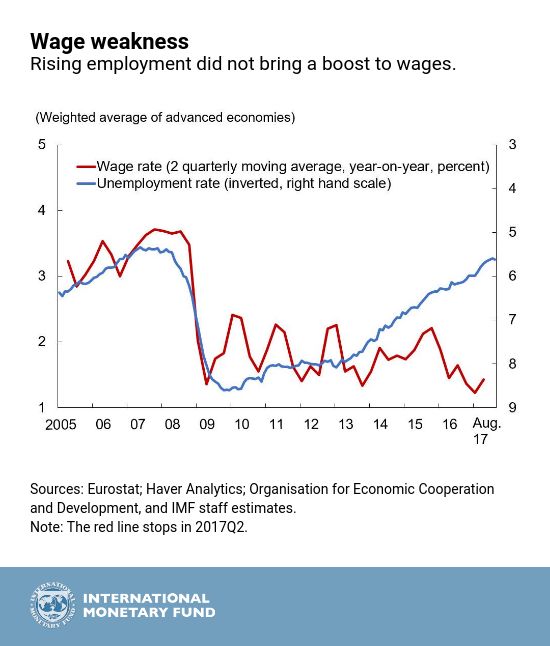

Wage growth has remained puzzlingly tepid in advanced economies despite falling unemployment rates. Continued slack in labor markets—in the form of still high unemployment in some countries or high levels of involuntary part time unemployment—along with weak productivity growth explain much of the sluggishness.

-

Equity valuations have continued their ascent and are near record highs, as central banks have maintained accommodative monetary policy settings amid weak inflation. This is part of a broader trend across global financial markets, where low interest rates, an improved economic outlook, and increased risk appetite boosted asset prices and suppressed volatility (as measured by the VIX, an index of volatility). While easier financial conditions bolstered growth momentum, they also pose risks if the search for yield extends too far.

Looking ahead to 2018

The bottom line: Don’t let a good recovery go to waste.

Reveries of an economic sweet spot should not lull policymakers or markets into complacency. Good times are most likely temporary. To ensure a more durable recovery, policymakers must seize the opportunity for reform.

Stay tuned for the update to the World Economic Outlook on January 22, 2018.