Credit ID Investors who bet on continued low volatility suffered steep losses.

Credit ID Investors who bet on continued low volatility suffered steep losses.

Credit ID Investors who bet on continued low volatility suffered steep losses.

Credit ID Investors who bet on continued low volatility suffered steep losses.

May 3, 2018

[caption id="attachment_23446" align="alignnone" width="1024"] Investors who bet on continued low volatility suffered steep losses (photo: Richard B. Levine/Newscom).[/caption]

Investors who bet on continued low volatility suffered steep losses (photo: Richard B. Levine/Newscom).[/caption]

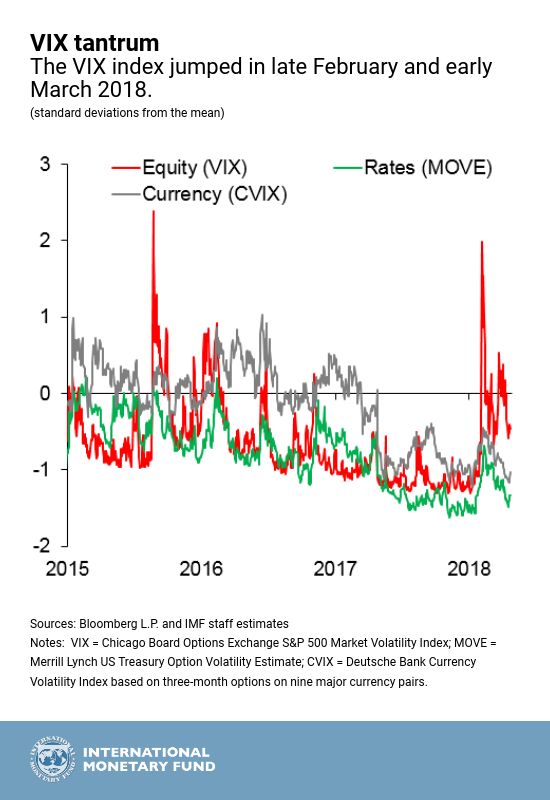

The bouts of volatility in early February and late March that spooked investors were confined to equity markets. Nevertheless, they illustrate the potential for sudden market moves to expose fragilities in the financial system more broadly.

With central banks in advanced economies set to normalize their monetary policies just as trade and geopolitical tensions flare up, economic and policy uncertainty may rise and financial conditions may tighten abruptly.

All this could lead to a period of renewed volatility.

The burst of turbulence early this year was preceded by a long period of calm marked by low economic uncertainty, low interest rates, easy funding conditions, and improving corporate performance, as shown in the October 2017 Global Financial Stability Report.

This extended period of calm led to the increasing popularity of volatility index-linked investment products. One example: investment strategies that involved selling VIX futures in the Chicago Board Options Exchange (CBOE) equity volatility index with the aim of profiting from declines in the index, known as the VIX. The VIX shows the expected level of price fluctuations in the Standard & Poor’s 500 Index of stocks over the next month.

These so-called short VIX strategies were profitable before the early February spike because, although the VIX index was near historic lows, realized volatility in equity markets was even lower. This premium in implied over-realized equity volatility provided steady returns for those selling VIX futures over the past year. But since the period of volatility that has come to be known as the VIX tantrum, this premium has turned negative, suggesting some of these strategies are now less appealing.

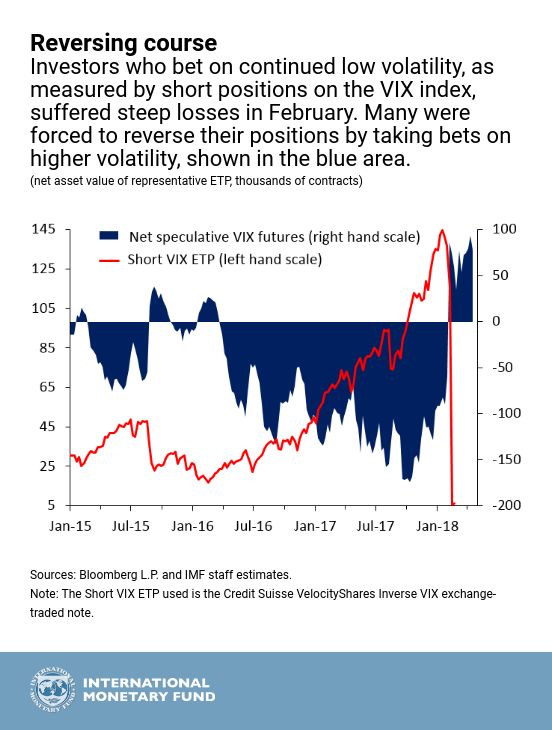

The April 2018 Global Financial Stability Report discusses how some of these short VIX strategies contributed to the February volatility spike. Among them, exchange-traded products that had built up significant bets on low volatility, and which were often sold to retail investors, incurred steep losses. More broadly, investors who expected low volatility to persist were forced to reverse their positions and cover losses by taking bets on higher volatility going forward. This sharp shift in positioning may have exacerbated the surge in the VIX.

The good news is that some of these short-VIX strategies, in particular those marketed to retail investors, appear to have been unwound. The bad news is that other strategies predicated on low volatility reportedly remain widespread, particularly among institutional investors. As a result, a more sustained rise in volatility across asset classes may force a broader class of investors to rebalance their portfolios, which could exacerbate declines in prices, especially if those positions employ financial leverage.

Volatility-targeting strategies are still popular and could be vulnerable. These strategies aim to keep the expected volatility of their investment portfolios at a certain target and use leverage to achieve that. However, their size and flexibility to deviate from their targets can vary significantly. Variable annuities and funds that use trading algorithms are apparently more likely to react to a spike in volatility by selling assets, which could exacerbate turbulence, although the exact extent and speed of such rebalancing are unclear.

Regulators and market participants should remain attuned to the risks associated with higher interest rates and greater volatility. They should ensure that financial institutions maintain robust risk management, including through the close monitoring of exposures to asset classes with valuations judged to be stretched.

Policymakers should develop tools to discourage excessive build-up of leverage that could increase market fragility. They should also be mindful of a migration of activities and risks to more opaque segments of the financial system. To address risks related to investment funds’ activities, regulators should endorse a common definition of financial leverage and strengthen supervision of liquidity risk.