View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

The current financial crisis is ferocious, but history shows the way to avoid another Great Depression Economic history is back in vogue. In the first half of 2008, surging prices of oil and other commodities revived unhappy memories of the stagflation of the 1970s. More recently, the extraordinary intensification of the global financial crisis since the mid-September collapse of Lehman Brothers has brought back an even more ominous specter from the past—the Great Depression of the 1930s. Comparing the present financial crisis to the deepest and most devastating economic cataclysm in modern history may seem a stretch, but there is now no question that the ongoing crisis has become the most dangerous of the post–World War II era. It is not so much the depth of the downturn in individual countries—devastating financial collapses have occurred before in advanced as well as in emerging economies—but its pervasive reach into all corners of the world economy that has created a threat to global prosperity not experienced in 70 years. But how large is the present financial crisis by past standards? And, crucially, what will be its likely economic impact and what can be done to contain the damage and pave the way for economic revival? Economic history can help answer these questions, offering both a useful perspective for understanding the relative magnitude and seriousness of the current crisis and invaluable lessons that can be applied to resolving it.

Not quite the Great Depression

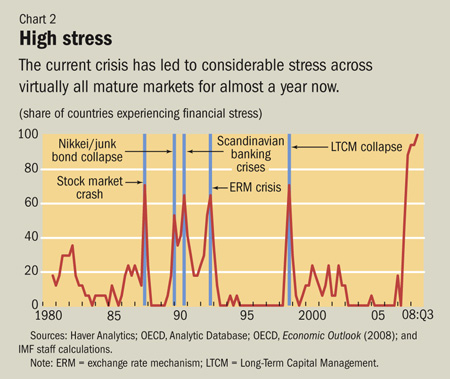

Another measure is the degree of market stress. The IMF’s October 2008 World Economic Outlook (Lall, Cardarelli, and Elekdag, 2008) calculates an index of financial stress, calibrated for 17 advanced economies since 1980. This index—available through September 2008 and covering variables such as interbank spreads and equity and bond market performance—has reached a level comparable to previous peak periods of stress across the range of countries. What is even more striking is that the stress has already been sustained at very high levels for almost a year and has affected all the countries in the sample (see Chart 2). And, since September, the strains have spread dramatically to emerging economies, including many of those that were initially seen as being more resilient to external factors than in the past because of strengthened balance sheets and huge international reserves.

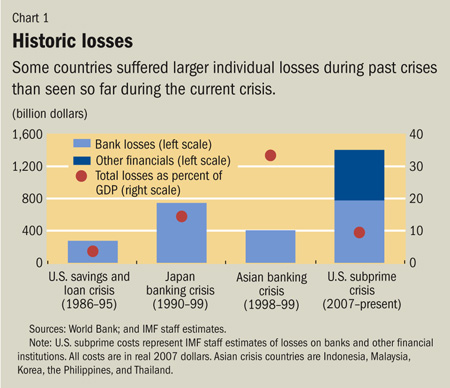

So certainly this is a crisis of extraordinary depth, extent, and ferocity. But does it match the financial collapse seen in the 1930s? Not quite. Between 1929 and 1933, 2,500 banks closed in the United States, and bank credit contracted by one-third. The stock market was down by 75 percent from its peak and unemployment rose to over 25 percent. Moreover, the impact of the Great Depression was felt in deep recessions worldwide. What we have seen so far still seems contained by these standards. Bank closures have been quite limited, and losses on deposits and other claims on banks have been minimal, as regulators have acted swiftly to deal with failing institutions. So far at least, bank credit has been sustained as country authorities have worked long hours to prevent a deeply disruptive collapse of bank capital, even if this has required digging deep into the unorthodox emergency tool kit of nationalization and public capital injections.

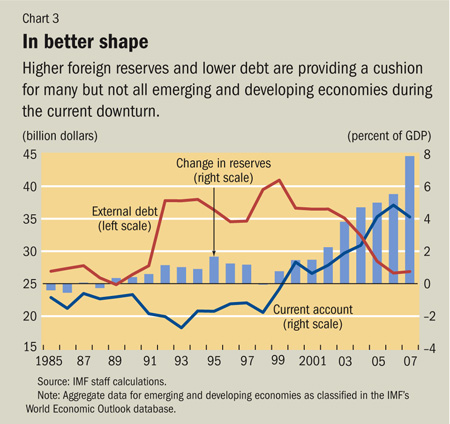

Complex linkages How big will the aggregate impact be? Some insights can be gained by looking at the historical record of what has happened to economic activity following financial crises in the past. At first glance, the evidence is mixed. The recent World Economic Outlook study found that only about half of 113 episodes of financial stress over the past 30 years were followed by economic slowdowns or recessions. However, the characteristics of a stress episode are a key determinant of the scale of its macroeconomic impact. Episodes associated with banking crises tend to have a much more severe macroeconomic impact. In fact, recessions associated with banking crises tend to last twice as long and to be twice as intense, and thus to imply four times the cumulative output losses. Also, episodes in which the financial stress lasts for a longer period are likely to be more damaging. Prior conditions are also critical in determining the macroeconomic impact of financial stress. One source of resilience for the global economy is that corporate balance sheets were generally strong going into this episode, given the major restructuring efforts that followed the 2001–02 dot-com bubble collapse. On the whole, corporate leverage had been reduced, and profitability had been raised to high levels, both of which should provide buffers in the face of tightening financing conditions. But what is less reassuring is that household balance sheets do not look nearly so solid, particularly in the United States, where saving rates dropped and borrowing soared during the housing boom years through 2006, and recent equity and house price declines have eroded net assets. What about the emerging economies? Again, the story must be nuanced. Their public sector balance sheets are much stronger than they were during the 2001–02 downturn, and the major emerging economies have accumulated large war chests of international reserves and reduced public-debt-to-GDP ratios during years of strong growth, providing more room for maneuver in the face of external pressures (see Chart 3). But these improved conditions are by no means uniform. Many countries, particularly in emerging Europe but also elsewhere, allowed large current account deficits to build up, financed in part through portfolio and banking inflows that are now being cut back sharply amid global deleveraging. And even countries with strong public balance sheets are showing vulnerabilities stemming from rapid private bank credit growth and overextended corporate and household borrowers, all of which are now contributing to sharp pullbacks from emerging markets. The sharp drop in commodity prices—a familiar pattern during global downturns—is adding to pressures on commodity exporters, especially on those that had spent a high proportion of the earlier buildup in revenues.

Drawing on this historical record, the global economy is clearly set for a major downturn. Indeed, activity has already slowed, and both business and consumer confidence have plunged. In 2009, activity in the advanced economies is projected in the IMF’s latest global forecast to contract on an annual basis for the first time in the post–World War II era. The emerging economies are also set to slow substantially in the aggregate, and more severely in the more vulnerable countries, although resilience in large economies like China will provide some support for the global economy.

Lessons from history A more recent cautionary tale is provided by Japan in the 1990s, where the impact on bank and corporate balance sheets of the collapse of the house and equity price bubbles was allowed to go unaddressed for many years, contributing to a decade of weak growth (see “The Road to Recovery: A View from Japan,” pp. 24–25, in this issue). A more positive case was the vigorous response to the Nordic banking crises of the early 1990s, which created the conditions for strong economic revival after a sharp downturn (see “Stockholm Solutions,” pp. 21–23, in this issue). A second important lesson is the value of providing macro-economic support in parallel with financial actions. With the effectiveness of monetary policy limited by financial disruptions, fiscal stimulus must play an important role to help maintain the momentum of the real economy and curtail negative feedbacks between the financial and real sectors. Indeed, increasing interest is now being paid to boosting infrastructure spending, akin to the public work programs of the Depression era. But, as the Japanese example makes clear, macroeconomic support by itself provides only breathing room, not a cure; it is essential to use the space provided to address the underlying financial problems or the outcome will be a series of fiscal packages with diminishing impact. And it should also be recognized that there will be limited space for macroeconomic responses in countries where the weakness of public sector management has been an integral source of the problem, as has often been the case in emerging market crises. The third lesson is the need for policy solutions that work at the global level. Again, the Great Depression provides a classic example of what not to do: the “beggar-thy-neighbor” tariff hikes following the Smoot-Hawley Tariff Act in the United States, which contributed to the international transmission of the crisis around the world. Other examples of the negative contagion effects of one country’s policy decisions on other countries can be drawn from the Latin American debt crises since the 1980s and from the Asian crisis. More positively, recent months have clearly demonstrated the benefits of internationally coordinated efforts, including to ensure liquidity support, enhance protection of deposits and interbank exposures, resolve failing institutions, and ease monetary policy. Actions are also in the works to ensure the adequacy of external financing for countries that have been affected by contagion from the crisis, including steps to increase the availability of IMF credits. The bottom line is that by learning lessons from experience, we can avoid the worst of the past. The global economy is being battered by a massive financial crisis, but the damage can be contained by strong and coordinated actions that repair the financial damage, support activity, and ensure continued access to external financing. References: Bernanke, Ben, 1983, “Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression,” American Economic Review, Vol. 73 (June), pp. 257–76. IMF, 2008, Global Financial Stability Report (Washington), October. Lall, Subir, Roberto Cardarelli, and Selim Elekdag, 2008, “Financial Stress and Economic Downturns,” in World Economic Outlook (Washington: IMF), October.

|