View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

Turning Nigeria's oil windfall into a blessing Nigeria squandered its oil windfall of the 1970s, which led to three decades of economic stagnation and the degradation of public institutions. The reason was a mix of bad fiscal and macroeconomic policy, corruption, and poor governance. Besides, not many countries (or even economists) at that time fully understood how difficult it is to manage oil windfalls. The latest oil boom gives Nigeria a chance to turn the "oil resource curse" into a blessing. It must learn from its past mistakes and can no longer plead inexperience. The country has made a good start by making fundamental changes in its response to the current oil boom, but sustaining these reforms is vital, both for Nigerians and for the entire African continent. In April 2006, Nigeria paid the last installment on the $30 billion it owed the Paris Club of official creditors, which had accounted for more than 85 percent of its external debt. As part of the agreement, Nigeria immediately paid $6 billion in arrears, with the remaining $24 billion restructured on Naples Terms—the Paris Club's concessionary terms for restructuring poor countries' external debt, resulting in an $18 billion write-off. While an unalloyed triumph, the very fact that Nigeria, a country blessed with vast oil reserves, had to extricate itself from a debt overhang was ironic. How did Nigeria get itself into this predicament, and what lessons can it and other oil-exporting developing countries draw from this experience? This is a good time to be asking these questions. The reason is that the oil price boom of the past few years has given oil-exporting developing countries, especially those that squandered the proceeds of the previous oil price booms of 1973–74 and 1979–80, a rare shot at redemption.

The debt overhang Reflecting these developments, Nigeria's currency, which was pegged to the U.S. dollar, was devalued by 36 percent between 1980 and 1984. But inflation was far higher, and the excess demand for foreign exchange was rationed by tightening restrictions on import licensing, raising the black market premium on foreign exchange. Eventually, in September 1986, Nigeria floated the naira. By that time, debt rescheduling and external financing had become urgent concerns. The float was the centerpiece of a reform program based on market incentives, liberalized prices, and the elimination of import licenses and commodity boards. But external debt kept mounting, reflecting not so much new borrowing after the mid-1980s as the cumulative effect of arrears and penalty interest rates. In addition to this macroeconomic imbalance, the country had little to show for its oil windfall in terms of economic development and poverty reduction. Why did this happen? The answer lies in the authorities' mismanagement of the oil boom of the 1970s, which shows that even brief periods of mismanagement can have negative consequences that persist for decades. The authorities' focus at that time was on avoiding Dutch disease, or a deterioration in the non-oil traded goods sector—notably, agriculture and manufacturing. Only much later did the authorities recognize the more serious damage to the economy—in the form of a debt overhang (see Box 1), prolonged economic stagnation, and degradation of public institutions—caused by corruption and bad governance. Box 1 External debt overhang Why, in view of Nigeria's vast oil and gas reserves, was the rescheduling so difficult? First, because Nigeria's external borrowings were effectively collateralized by oil, creditors became skittish as oil prices fell. Second, in view of the economic dominance of oil by the mid-1980s, coupled with serious policy and institutional failures, creditors were unwilling to reschedule Nigeria's debt without an IMF-supported program. Nigeria had developed a credibility gap and was unable to attract foreign financing even for potentially high-rate-of-return investments: it had developed a classic "debt overhang."

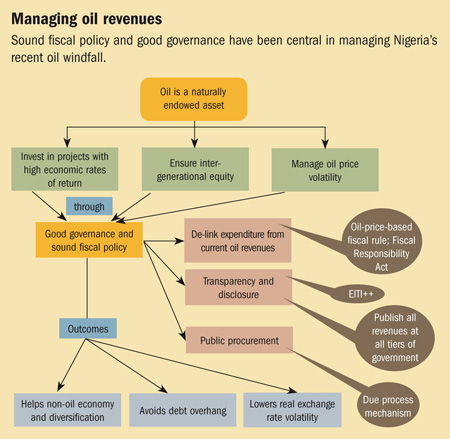

A new chance Box 2 Extractive Industries Transparency Initiative Nigeria was one of the first countries to adopt the EITI, approving the Nigeria Extractive Industries Transparency Initiative (NEITI) Bill in May 2007. Going beyond the basic requirement, Nigeria has conducted financial, physical, and process audits of the petroleum sector for the period 1999–2004. This has led to Nigeria's efforts being labeled EITI++, and the initiative is now being extended to other countries under the auspices of the World Bank and other EITI partners. On the macroeconomic front, the central challenge was to lower volatility by de-linking public expenditure from current oil revenue. Nigeria succeeded in doing this in 2004 by adopting an "oil-price-based fiscal rule." The rule's objective was to constrain spending by transferring oil revenues to the budget in accordance with a reference price, together with a ceiling on the non-oil deficit. The Fiscal Responsibility Bill, signed by President Umaru Yar'Adua in November 2007, enshrined the oil-price-based fiscal rule into law. To improve transparency and tackle corruption, the government adopted a two-pronged approach: • It embedded anticorruption measures in a comprehensive economic reform program, and For example, to fight corruption, the government reviewed the public procurement process and instituted a "due process mechanism" in public contracts. The oil-price-based fiscal rule and the adoption of the EITI both underscored Nigeria's determination to make a clean break with the past by fighting corruption and improving governance. In a revolutionary move, Nigeria went beyond the petroleum sector by publishing revenues from all sources at all tiers of government. The credibility boost facilitated Nigeria's debt cancellation by the Paris Club and lifted its profile in the eyes of investors. Standard & Poor's and Fitch Ratings assigned Nigeria a sovereign credit rating of BB– for 2007, affirming earlier results. Nigeria's rating peers at the time included Indonesia, Turkey, Ukraine, Venezuela, and Vietnam. The improved rating led to sizable increases in foreign direct investment in both the oil sector (about $6 billion a year) and non-oil sectors (about $3 billion a year). The current oil boom was necessary for elimination of Nigeria's debt overhang—by providing needed liquidity—but it was by no means sufficient. If the lessons from the 1970s had not been learned, the opportunity presented by the new boom would have certainly been squandered. The combination of high oil prices, improved governance, new political will and leadership, and better fiscal management have made all the difference. The big challenge now is to maintain the momentum of reforms. (For the challenges and policy responses, see chart.)

Lessons learned Although the oil-price-based rule helps save part of the oil windfall, it is not enough because the accrual of oil revenues results from the depletion of an asset (oil reserves). Hence, the government also needs to ensure that the rate of return on government spending is at least as high as the yield on a diversified portfolio of financial assets. This means careful screening of public investment projects and altering the composition of spending. Nigeria is ensuring a higher rate of return on government spending partly through the due process mechanism, which has promoted an open tender process with competitive bidding for government contracts. But it also needs a system for the effective cost-benefit analysis of public investments. An excellent example of a high-rate-of-return investment was Nigeria's 2005–06 buyback of its Paris Club debt. Not only did the buyback save on future debt service costs, it improved the climate for investment and growth by eliminating the external debt overhang and strengthening Nigeria's creditworthiness. Because oil is a naturally endowed and exhaustible asset, its benefits should be shared across generations. One way to ensure this is by bequeathing the next generation a healthy and diversified economy with low indebtedness. Nigeria has taken the first steps in this process. Saving part of the windfall and investing in infrastructure and long-gestation projects in health and education is another part of the equation. But despite the real progress made in the past few years, Nigeria remains heavily dependent on oil. The share of oil and gas reached more than 95 percent of exports in 2007 on the back of the huge oil price rise; moreover, oil and gas continue to account for 85 percent of government revenues and 52 percent of GDP. And despite the boom and Nigeria's resource abundance, nearly 54 percent of its population lives on less than $1 a day. Clearly, Nigeria has a long way to go in diversifying its economy, furthering its development agenda, and reducing poverty. While the current oil boom has provided the means to eliminate the debt overhang and even build up a reserves cushion, policymakers need to guard against overexuberance about the continuing rise in oil prices. Such caution is underscored by the recent fall in oil prices linked to the spreading global financial crisis and the prospect of a worldwide recession. We are seeing that fortunes can change rapidly and dramatically, as they did in the early 1980s. The bitter lesson from experience is clear: governments of oil-rich developing countries must adopt conservative reference prices and anticipate volatility and downside risks. The second major lesson from Nigeria's experience is that corrective measures must go beyond the confines of economic policy and embrace governance and transparency. Good fiscal policy is critical, but ensuring that Nigeria gets its fair share of oil revenues and that the oil is extracted with minimal waste and maximum transparency is equally important. In this regard, Nigeria has been a trailblazer by earning a label of EITI++ and publishing the revenues of all levels of government. Nigeria has embarked on an ambitious effort to boost growth and maximize the welfare of all its citizens. The latest oil boom has provided the wherewithal to reverse the damage caused by the squandering of the oil boom of the 1970s. This opportunity must not be allowed to slip by. Suggested Readings: Aghion, Philippe, Philippe Bacchetta, Romain Ranciere, and Kenneth Rogoff, 2006, "Exchange Rate Volatility and Productivity Growth: The Role of Financial Development," NBER Working Paper No. 12117 (Cambridge, Massachusetts: National Bureau of Economic Research). Budina, Nina, Gaobo Pang, and Sweder van Wijnbergen, 2007, "Nigeria's Growth Record—Dutch Disease or Debt Overhang?" World Bank Policy Research Working Paper No. 4256 (Washington: World Bank). Okonjo-Iweala, Ngozi, and Philip Osafo-Kwaako, 2007, "Nigeria's Economic Reforms: Progress and Challenges," Brookings Global Economy and Development Working Paper No. 6 (Washington: Brookings Institution). Pinto, Brian, 1987, "Nigeria During and After the Oil Boom: A Policy Comparison with Indonesia," The World Bank Economic Review, Vol. 1, No. 3, pp. 419–45. World Bank, 2007, Country Brief on Nigeria (November).

|