|

Table 1. Overview of the World Economic Outlook Projections |

|

(Percent change unless noted otherwise) |

| |

| |

Year over Year |

|

|

|

|

| |

|

|

Projections |

|

Difference from October 2012 WEO Projections |

|

Q4 over Q4 |

| |

|

|

|

|

Estimates |

Projections |

| |

2011 |

2012 |

2013 |

2014 |

|

2013 |

2014 |

|

2012 |

2013 |

2014 |

| |

|

World Output 1/ |

3.9 |

3.2 |

3.5 |

4.1 |

|

–0.1 |

–0.1 |

|

2.9 |

3.8 |

4.0 |

|

Advanced Economies |

1.6 |

1.3 |

1.4 |

2.2 |

|

–0.2 |

–0.1 |

|

0.9 |

2.0 |

2.1 |

|

United States |

1.8 |

2.3 |

2.0 |

3.0 |

|

–0.1 |

0.1 |

|

1.9 |

2.4 |

3.2 |

|

Euro Area |

1.4 |

–0.4 |

–0.2 |

1.0 |

|

–0.3 |

–0.1 |

|

–0.7 |

0.5 |

1.0 |

| Germany |

3.1 |

0.9 |

0.6 |

1.4 |

|

–0.3 |

0.1 |

|

0.6 |

1.3 |

1.1 |

| France |

1.7 |

0.2 |

0.3 |

0.9 |

|

–0.1 |

–0.2 |

|

0.3 |

0.3 |

1.2 |

| Italy |

0.4 |

–2.1 |

–1.0 |

0.5 |

|

–0.3 |

0.0 |

|

–2.4 |

0.1 |

0.4 |

| Spain |

0.4 |

–1.4 |

–1.5 |

0.8 |

|

–0.1 |

–0.2 |

|

–1.9 |

–0.3 |

0.8 |

| Japan |

–0.6 |

2.0 |

1.2 |

0.7 |

|

0.0 |

–0.4 |

|

0.2 |

2.6 |

–0.1 |

| United Kingdom |

0.9 |

–0.2 |

1.0 |

1.9 |

|

–0.1 |

–0.3 |

|

0.0 |

1.4 |

2.0 |

| Canada |

2.6 |

2.0 |

1.8 |

2.3 |

|

–0.2 |

–0.1 |

|

1.3 |

2.2 |

2.3 |

| Other Advanced Economies 2/ |

3.3 |

1.9 |

2.7 |

3.3 |

|

–0.3 |

–0.1 |

|

2.0 |

3.5 |

3.2 |

| Newly Industrialized Asian Economies |

4.0 |

1.8 |

3.2 |

3.9 |

|

–0.4 |

–0.2 |

|

2.4 |

3.9 |

3.8 |

| Emerging Market and Developing Economies 3/ |

6.3 |

5.1 |

5.5 |

5.9 |

|

–0.1 |

0.0 |

|

5.5 |

5.9 |

6.2 |

|

Central and Eastern Europe |

5.3 |

1.8 |

2.4 |

3.1 |

|

–0.1 |

0.0 |

|

1.6 |

3.2 |

3.1 |

|

Commonwealth of Independent States |

4.9 |

3.6 |

3.8 |

4.1 |

|

–0.3 |

–0.1 |

|

2.4 |

4.3 |

3.4 |

| Russia |

4.3 |

3.6 |

3.7 |

3.8 |

|

–0.2 |

–0.1 |

|

2.4 |

4.4 |

3.4 |

| Excluding Russia |

6.2 |

3.9 |

4.3 |

4.7 |

|

–0.5 |

–0.1 |

|

. . . |

. . . |

. . . |

| Developing Asia |

8.0 |

6.6 |

7.1 |

7.5 |

|

–0.1 |

0.0 |

|

7.3 |

7.1 |

7.8 |

| China |

9.3 |

7.8 |

8.2 |

8.5 |

|

0.0 |

0.0 |

|

8.1 |

7.9 |

8.8 |

| India |

7.9 |

4.5 |

5.9 |

6.4 |

|

–0.1 |

0.0 |

|

5.4 |

6.0 |

6.4 |

| ASEAN-5 4/ |

4.5 |

5.7 |

5.5 |

5.7 |

|

–0.2 |

0.0 |

|

7.7 |

5.8 |

5.5 |

| Latin America and the Caribbean |

4.5 |

3.0 |

3.6 |

3.9 |

|

–0.3 |

–0.1 |

|

3.1 |

4.2 |

3.6 |

| Brazil |

2.7 |

1.0 |

3.5 |

4.0 |

|

–0.4 |

–0.2 |

|

2.1 |

4.0 |

4.1 |

| Mexico |

3.9 |

3.8 |

3.5 |

3.5 |

|

0.0 |

0.0 |

|

2.8 |

4.9 |

2.5 |

| Middle East and North Africa |

3.5 |

5.2 |

3.4 |

3.8 |

|

–0.2 |

0.0 |

|

. . . |

. . . |

. . . |

| Sub-Saharan Africa 5/ |

5.3 |

4.8 |

5.8 |

5.7 |

|

0.0 |

0.1 |

|

. . . |

. . . |

. . . |

| South Africa |

3.5 |

2.3 |

2.8 |

4.1 |

|

–0.2 |

0.3 |

|

1.5 |

4.2 |

4.1 |

| Memorandum |

|

|

|

|

|

|

|

|

|

|

|

| European Union |

1.6 |

–0.2 |

0.2 |

1.4 |

|

–0.3 |

–0.2 |

|

–0.3 |

1.0 |

1.2 |

| World Growth Based on Market Exchange Rates |

2.9 |

2.5 |

2.7 |

3.4 |

|

–0.2 |

–0.1 |

|

2.1 |

3.1 |

3.3 |

| World Trade Volume (goods and services) |

5.9 |

2.8 |

3.8 |

5.5 |

|

–0.7 |

–0.3 |

|

. . . |

. . . |

. . . |

| Imports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

4.6 |

1.2 |

2.2 |

4.1 |

|

–1.1 |

–0.4 |

|

. . . |

. . . |

. . . |

| Emerging Market and Developing Economies |

8.4 |

6.1 |

6.5 |

7.8 |

|

–0.1 |

–0.1 |

|

. . . |

. . . |

. . . |

| Exports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

5.6 |

2.1 |

2.8 |

4.5 |

|

–0.8 |

–0.4 |

|

. . . |

. . . |

. . . |

| Emerging Market and Developing Economies |

6.6 |

3.6 |

5.5 |

6.9 |

|

–0.2 |

–0.2 |

|

. . . |

. . . |

. . . |

| Commodity Prices (U.S. dollars) |

|

|

|

|

|

|

|

|

|

|

|

| Oil 6/ |

31.6 |

1.0 |

–5.1 |

–2.9 |

|

–4.1 |

1.3 |

|

–1.0 |

–3.3 |

–3.3 |

| Nonfuel (average based on world commodity export weights) |

17.8 |

–9.8 |

–3.0 |

–3.0 |

|

–0.1 |

1.9 |

|

1.2 |

–4.2 |

–2.6 |

| Consumer Prices |

|

|

|

|

|

|

|

|

|

|

|

| Advanced Economies |

2.7 |

2.0 |

1.6 |

1.8 |

|

0.0 |

0.0 |

|

1.8 |

1.6 |

1.8 |

| Emerging Market and Developing Economies 3/ |

7.2 |

6.1 |

6.1 |

5.5 |

|

0.3 |

0.2 |

|

5.1 |

5.1 |

4.6 |

| London Interbank Offered Rate (percent) 7/ |

|

|

|

|

|

|

|

|

|

|

|

| On U.S. Dollar Deposits |

0.5 |

0.7 |

0.5 |

0.6 |

|

–0.1 |

–0.1 |

|

. . . |

. . . |

. . . |

| On Euro Deposits |

1.4 |

0.6 |

0.1 |

0.3 |

|

–0.1 |

–0.2 |

|

. . . |

. . . |

. . . |

| On Japanese Yen Deposits |

0.3 |

0.3 |

0.2 |

0.2 |

|

–0.1 |

–0.1 |

|

. . . |

. . . |

. . . |

| |

Note: Real effective exchange rates are assumed to remain constant at the levels prevailing during November 12–December 10, 2012. When economies are not listed alphabetically, they are ordered on the basis of economic size. The aggregated quarterly data are seasonally adjusted.

1/ The quarterly estimates and projections account for 90 percent of the world purchasing-power-parity weights.

2/ Excludes the G7 (Canada, France, Germany, Italy, Japan, United Kingdom, United States) and Euro Area countries.

3/ The quarterly estimates and projections account for approximately 80 percent of the emerging market and developing economies.

4/ Indonesia, Malaysia, Philippines, Thailand, and Vietnam.

5/ Regional and global aggregates include South Sudan.

6/ Simple average of prices of U.K. Brent, Dubai, and West Texas Intermediate crude oil. The average price of oil in U.S. dollars a barrel was $105.08 in 2012; the assumed price based on futures markets is $99.71in 2013 and $96.78 in 2014.

7/ Six-month rate for the United States and Japan. Three-month rate for the euro area. |

The near-term growth outlook for Japan has not been downgraded despite renewed recession. Activity is expected to expand by 1.2 percent in 2013, broadly unchanged from October. The recession is expected to be short-lived because the effects of temporary factors, such as the car subsidy and disruptions to trade with China, will subside. And a sizeable fiscal stimulus package and further monetary easing will give growth at least a near-term boost, with support from a pickup in external demand and a weaker yen.

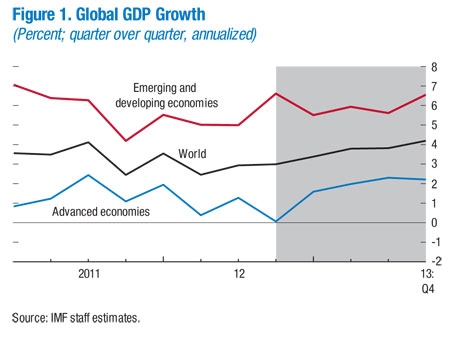

Growth in emerging market and developing economies is on track to build to 5.5 percent in 2013. Nevertheless, growth is not projected to rebound to the high rates recorded in 2010–11. Supportive policies have underpinned much of the recent acceleration in activity in many economies. But weakness in advanced economies will weigh on external demand, as well as on the terms of trade of commodity exporters, given the assumption of lower commodity prices in 2013 in this Update. Moreover, the space for further policy easing has diminished, while supply bottlenecks and policy uncertainty have hampered growth in some economies (for example, Brazil, India). Activity in Sub-Saharan Africa is expected to remain robust, with a rebound from flood-related output disruptions in Nigeria contributing to an acceleration in overall growth in the region in 2013.

Against this backdrop, the projections in this WEO Update imply that global growth will strengthen gradually through 2013, averaging 3.5 percent on an annual basis, a moderate uptick from 3.2 percent in 2012, but 0.1 percentage point lower than projected in the October 2012 WEO. A further strengthening to 4.1 percent is projected for 2014, assuming recovery takes a firm hold in the euro area economy.

Policy Action Is Needed to Secure the Fragile Global Recovery

The policy requirements outlined in the October 2012 WEO remain relevant. Most advanced economies face two challenges. First, they need steady and sustained fiscal consolidation. Second, financial sector reform must continue to decrease risks in the financial system. Addressing these challenges will support recovery and reduce downside risks.

The euro area continues to pose a large downside risk to the global outlook. In particular, risks of prolonged stagnation in the euro area as a whole will rise if the momentum for reform is not maintained. Adjustment efforts in the periphery countries need to be sustained and must be supported by the center, including through full deployment of European firewalls, utilization of the flexibility offered by the Fiscal Compact, and further steps toward full banking union and greater fiscal integration.

In the United States, the priority is to avoid excessive fiscal consolidation in the short term, promptly raise the debt ceiling, and agree on a credible medium-term fiscal consolidation plan, focused on entitlement and tax reform.

In Japan, the priority is to underpin the renewed emphasis on raising growth and inflation with more ambitious monetary policy easing, adopt a credible medium-term fiscal consolidation plan anchored by the consumption tax increases in 2014–15, and raise potential growth through structural reforms. Absent a strong medium-term fiscal strategy, the stimulus package carries important risks. Specifically, the stimulus-induced recovery could prove short lived, and the debt outlook significantly worse.

In China, ensuring sustained rapid growth requires continued progress with market-oriented structural reforms and rebalancing of the economy more toward private consumption. In other emerging market and developing economies, requirements differ. The general challenge is to rebuild macroeconomic policy space. The appropriate pace of rebuilding must balance external downside risks against risks of rising domestic imbalances. In some economies with large external surpluses and low public debt, this entails a lower, more sustainable pace of credit growth and fiscal measures to support domestic demand. In others, fiscal deficits need to be rolled back further, while monetary tightening proceeds gradually. Macroprudential measures can help stem emerging financial excesses. In the Middle East and North Africa region, many countries will need to maintain macroeconomic stability under difficult internal and external conditions.