| Japan and the IMF | |

|

|

February 13, 2003 Ordering Information

| ||||||||||||||||||||||||||||||||||||||||||||

| Overview Tim Callen and Jonathan D. Ostry |

|

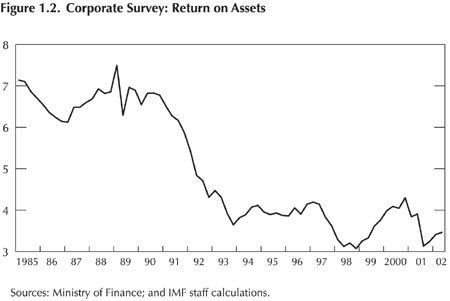

Japan's economic performance since the early 1990s has been disappointing, both in relation to its own history and relative to the record of other major industrial countries. Real GDP growth has averaged 1 percent a year over the past 10 years, well below that in other OECD countries, and only one-fourth of the 4 percent annual average growth rate recorded in Japan in the 1980s. Japan, moreover, experienced three recessions in the past decade, in contrast to the trend in other industrial countries toward milder and less frequent downturns in the postwar period. Meanwhile, nominal GDP has fared even worse than real GDP (the level of nominal GDP in 2001 was approximately the same as in 1995), as moderate deflation has become entrenched. This poor economic performance has led some commentators to call the 1990s Japan's "lost decade." It is now generally recognized that Japan's economic problems reflect a failure to deal proactively with the impact of the collapse in asset prices in the early 1990s. The bubble in Japanese stock prices burst in 1990 and, by mid-1992, equity prices had fallen by about 60 percent. Land prices began their downward spiral a year after stock prices and, while initially less precipitous than the drop in equity prices, the decline continued inexorably through the 1990s and early 2000s. The asset price collapse created problems for the banking system by impairing loan collateral and eroding bank capital—initially by wiping out hidden gains on stock holdings and subsequently through a direct feed through to banks' capital ratios under the new marking-to-market rules. Firms—which had borrowed heavily to finance expansive business strategies in the bubble years—found themselves with massive excess debt and capacity in the face of the ensuing economic slowdown. While the growth slowdown was initially viewed as a cyclical response to the decline in asset prices, the long period of weak growth has led to a number of competing hypotheses to explain the poor performance. Research at the International Monetary Fund (IMF)—see, for example, the papers in Bayoumi and Collyns, 2000—has highlighted the central role played by financial institutions in magnifying the impact of the decline in asset prices on the economy. Increases in bank lending, operating both directly and through a self-reinforcing cycle with increases in land and stock prices, helped explain the strong growth in the second half of the 1980s. But, once asset prices began to fall, this process operated in reverse as undercapitalized banks restrained lending to maintain capital adequacy standards. In turn, this blunted the impact of macroeconomic policies as households and firms were unable to respond to monetary and fiscal stimulus because of the limited availability of funds from the banking system. Hayashi and Prescott (2002), by contrast, argue that the problem was a sharp fall in productivity stemming from the increasing failure of the traditional Japanese economic model to adapt to the requirements of a more deregulated and competitive world economy. Krugman (1998) takes yet a third view, according to which an insufficiency of demand drove the downturn, as Japan entered a liquidity trap—with nominal interest rates unable to fall below zero, and real interest rates too high to stimulate economic activity. The above hypotheses are not, of course, mutually exclusive, and indeed the prolonged period of lackluster performance may owe much to counterproductive interactions among the various forces, which magnified the downturn. For example, there is little doubt that dysfunctionality in the banking system—because of a shortage of capital in the face of still-to-be-recognized downgrades to asset quality—hampered the ability of monetary policy to end deflation. It is also likely that fiscal policy management—especially the focus on rural public works projects with low multiplier effects—undercut that instrument's ability to support aggregate demand. Uneven progress in regulatory reforms has also contributed to a documented lack of productivity growth in many of Japan's domestic sectors, in contrast to the more dynamic export-oriented industries such as electronics. This has resulted in a sharp slowdown in potential growth in the 1990s, helping to contain the size of the output gap, unemployment, and capacity underutilization over the past decade. At the time of writing this overview in late 2002, Japan appears to have emerged from its worst recession in postwar history. After three consecutive quarters of negative growth in 2001, activity picked up in early 2002, led by net exports as the United States and Asian economies rebounded. But private domestic demand has remained stubbornly weak, as the underpinnings of business investment and household spending continue to be plagued by excess stocks of debt, capital, and labor, as well as by ongoing uncertainties about the soundness of the banking and fiscal systems. Despite the modest recovery, capacity utilization rates in manufacturing are low, while the IMF staff's production functionbased estimate of the output gap remains stuck around 3 percent of (potential) GDP despite a significant slowdown in the potential growth rate. Labor market adjustment continues, with firms scaling down jobs and the unemployment rate near record levels. And, particularly pernicious given the extent of corporate and public debt burdens, deflation persists at about 1 percent a year, with surveys suggesting this is likely to continue for some time to come. Financial markets also appear less than sanguine that a durable recovery is finally under way. Equity prices remain stuck at post-bubble lows, with bank stocks continuing to weigh heavily on the market. In addition to the weakness in the earnings outlook, structural factors—including the continued unwinding of cross-shareholdings between banks and corporates—have also had an impact on the market. The yen, however, has strengthened considerably since early 2002, although this likely reflects the strengthening of the balance of payments in the export-led phase of the recovery, rather than the market's assessment that a durable economic turnaround is under way. Yields on Japanese government bonds (JGBs), meanwhile, have declined to 1 percent, despite sovereign rating downgrades and mounting public debt, consistent with the view that a pickup in nominal growth is some way off. More than a decade after the bursting of the asset price bubble, there remains pervasive evidence of unaddressed weaknesses in the banking and corporate sectors. Despite write-offs of 16 percent of GDP over the past decade, banks' nonperforming loans (NPLs) have risen, and there is a likelihood that more loans will turn sour in the future. Weak profitability, meanwhile, continues to constrain banks' provisioning capacity. While measured capital ratios remain above the minima mandated by the regulatory authorities, the weight of government preferred shares and deferred tax assets undermines capital quality. As well as the domestic implications, bank weaknesses also have potential ramifications for international financial stability given banks' foreign securities holdings and lending and foreign investors' exposure to Japan. On the corporate side, rates of return remain low, not least because of the slow progress in reducing the still significant excesses of capital, debt, and employment from the bubble years (Figures 1.1 and 1.2). Concerns about the impact of restructuring on unemployment may constrain the speed of adjustment—for example, the recourse to the Industrial Revitalization Law in some recent high-profile cases may reflect a desire to limit job losses relative to what would ensue under a court-led restructuring plan. The government of Prime Minister Koizumi, which came into office in April 2001, has made some progress in addressing the fundamental weaknesses in the economy. A strategy has been set out, encompassing banking reform, fiscal consolidation, and deregulation, but it is not fully fleshed out, and implementation has been slower and less complete than hoped and undermined by resistance from vested interests. The banking strategy is appropriately focused on strengthening loan classification practices, accelerating the disposal of NPLs, and reducing exposure to equity price risk. While some progress has been made on the first issue—including through the special bank inspections concluded in April 2002—there remain concerns that the true scale of the NPL problem has yet to be recognized, partly because the special inspections focused primarily on major banks' exposure to large corporate borrowers, and thus ignored exposures to potentially weak small and medium-sized enterprises and of nonmajor banks. The authorities' strategy on bad loan disposal is focused too narrowly, with specific time-bound requirements set only for the worst of major banks' bad loans, rather than all NPLs across the entire banking system. Against this background, the IMF staff has been engaged in an intensive dialogue with the Japanese authorities to flesh out an integrated policy strategy to lift Japan's economy from its decade-long period of lackluster performance and set the stage for self-sustained growth without deflation. The essence of the strategy is to move forward forcefully with bank and corporate restructuring in the context of supportive macroeconomic policies designed to limit any short-term adverse impact on economic activity and reverse the course of deflation. The staff's strategy has four interlinked pillars, dealing respectively with banking reforms, corporate restructuring, fiscal policy, and monetary policy. With regard to the financial sector, the staff has stressed the need to adopt a more forward-looking approach to loan classification and provisioning practices systemwide to ensure that loans are realistically valued on bank balance sheets. A key issue relates to "gray-zone" loans—loans that are performing (in no small measure because near-zero interest rates allow firms with barely positive cash flow to remain current on debt service) but are at clear risk of becoming nonperforming. Absent regulatory pressure or a strong capital base, banks lack incentives to be aggressive with such claims, especially if they expect higher recovery values down the road. If such a comprehensive review of classification and provisioning practices were to result in bank capital ratios falling below regulatory minima, as many observers expect, and if banks continue to face difficulty in raising private funds, there would be no alternative in the staff's view but to inject public capital into systemically important banks, subject to strong conditionality to limit moral hazard. An alternative approach—spreading recognition of nonperforming loans over a number of years to allow provisions to be paid from operating profits with no impact on capital—would preserve an aura of stability, but would postpone resolution of the fundamental problems. For nonsystemic banks that fail to meet capital requirements, "prompt corrective action" would need to be invoked, including orderly exit of nonviable banks. Together with a scaled-down role of public financial intermediation achieved by leveling the playing field with private banks, this would underpin efforts to boost banks' core profitability over the medium term. On corporate restructuring, the lack of progress by banks in pushing through strong restructuring at debtor firms needs to be overcome. Given that the bulk of firms' excess leverage is owed to banks, it is the banks that must take the lead in agreeing restructuring plans with their potentially viable debtors, pushing nonviable firms into liquidation, and disposing of unwanted loans to third parties—such as the Resolution and Collection Corporation (RCC), the soon-to-be-created Industrial Revitalization Corporation (ICC), or private investors. The RCC and ICC have a key role to play in developing Japan's distressed debt market, not least by accelerating purchases and rapid resales of NPLs, including "gray-zone" loans, where the bulk of companies with a real chance of a turnaround are likely to be found. A range of structural reforms are also needed to ease the transitional costs from corporate restructuring and generate new investment and job opportunities, including steps to improve labor mobility and enhance the social safety net; regulatory reforms in critical sectors (such as health and child care, retail and distribution, and housing); proactive enforcement of competition policy; and strengthening of corporate governance rules. Given the high level of public sector debt and the large budget deficit, the staff has stressed the need to lay out a detailed and credible medium-term fiscal consolidation strategy to maintain investor confidence in JGBs. At the same time, however, steps would be needed to ensure that a sizable near-term fiscal contraction did not add headwinds to economic activity that would arise from an accelerated effort to spur bank and corporate restructuring. Key fiscal reforms that would help to establish the credibility of the government's program include:

In addition to the need to make early progress on implementing these reforms, the IMF has also stressed the need for the government to publicly lay out a comprehensive strategy to stabilize the public debt ratio over a 5–10 year horizon and to subsequently bring the debt ratio down, given the looming demographic pressures. A permanent fiscal responsibility law could provide an appropriate vehicle to set out a medium-term debt target and the broad objectives of tax, spending, and social security policies. On monetary policy, there is a broad consensus—including in the Bank of Japan itself—that the policy actions taken to date are unlikely to produce an early end to deflation. A range of research nevertheless suggests that there is scope to do more on the monetary policy front, even though short-term interest rates are at their floor. Deflationary episodes in Sweden and the United States in the 1930s are at least suggestive that more aggressive and sustained actions than have yet been undertaken by the Bank of Japan could be helpful in ridding Japan of entrenched deflation. While bank weaknesses are clearly undercutting the effectiveness of monetary policy, the monetary transmission mechanism—including through the portfolio-rebalancing and expectations channels—does not appear to have been fully short-circuited. IMF staff have thus stressed the need for the Bank of Japan to publicly commit to end deflation within a reasonable (12–18-month) time frame, backed up by further quantitative easing, including accelerated purchases of JGBs. This should be followed over the medium term with a positive inflation target to help guard against the risk of again being constrained by the zero bound on nominal interest rates. Movements in the yen have been a source of concern for countries in the Asian region, particularly for those that fix their currencies to the U.S. dollar. While the exchange rate may constitute one potential transmission channel of monetary policy at this stage, the IMF staff's view has been that concerns about the potential regional impact should not impede the implementation of a vigorous monetary policy aimed at delivering a timely end to deflation. The impact of movements in the yen are likely to be more manageable now than during the Asian crisis, given the generally greater flexibility of exchange rate regimes, stronger reserve positions, and healthier external debt profiles in the region. Indeed, were monetary easing to take place in the context of a comprehensive policy package to restore healthy growth in Japan, any weakening of the yen might be limited by an increase in confidence about Japan's future economic prospects. Such a policy package would be of substantial benefit to the Asian region—and the rest of the world—over the medium term. The papers presented in this book flesh out the details of the four interlinked pillars of the IMF staff's proposed policy strategy. The first two sections of the book address the core issues of bank and corporate restructuring. Section I, "Addressing Financial Sector Weaknesses," deals with issues relating to the reform of the financial sector, while Section II, "Corporate Restructuring and Structural Reforms," examines the policies needed to accelerate restructuring in the corporate sector, and the implementation of structural reforms to help generate employment and investment opportunities in new sectors of the economy. The third and fourth sections of the book discuss issues related to macroeconomic policies. In Section III, "Fiscal Policy Challenges," the sustainability of public debt position and the effectiveness of fiscal policy as a demand management tool are taken up. Section IV, "Monetary and Exchange Rate Policy in Japan," discusses the conduct of monetary policy in a deflationary environment. Because of Japan's importance in the Asia region, Section V of the book, "Japan and Asia," looks at the impact of reforms in Japan on other Asian countries. In Chapter 2, "Current Issues Facing the Financial Sector," Tim Callen and Martin Mühleisen provide an overview of recent developments in the banking and life insurance sectors. In light of the sharp economic slowdown in 2001 and the steep drop in equity prices, questions have once again been raised about the financial health of these institutions. In response, the authorities have set out a reform strategy to deal with the weaknesses in the banking sector, but the chapter assesses that much more needs to be done. In particular, despite steps to strengthen loan classification practices—including through the recently concluded special bank inspections—considerable doubt remains about whether the authorities have recognized the true scale of the NPL problem. Given the scheduled removal of the blanket guarantee on most demand deposits from end-March 2005, time is of the essence in dealing with these issues. If doubts remain then about the health of the banks, there is the potential for deposit shifting between institutions, and the risk that contagion could spread from weak institutions. Over the medium term, boosting underlying profitability is the key to ensuring a healthy banking system. Consequently, the authors discuss measures to raise bank profitability, including reforms to downsize the postal savings system and government financial institutions. The issue of how the quality of bank loan portfolios and the degree of corporate indebtedness have affected the evolution of bank credit in Japan is examined by Giovanni Dell'Ariccia in Chapter 3, "Banks and Credit in Japan." An important policy question is whether the recent contraction in bank credit stems from weaknesses in the banking system, which has led to a decline in the supply of credit, or from a lack of corporate demand for credit as companies reduce their excess leverage. To investigate this issue, a three-dimensional panel of data is used, disaggregated by firm size, industrial sector of the borrowing firm, and specialization of the lending bank. The results of the analysis suggest that both corporate and banking sector weaknesses share the blame for the decline in bank credit. On the banking side, credit growth is found to be lower for banks with a high initial proportion of nonperforming loans and a low initial loan-loss reserve ratio, while on the corporate side, a high initial degree of bank dependence and leverage are found to be detrimental to credit growth. The policy implications of these results are that the resolution of balance sheet problems in both the banking and corporate sectors is necessary to restore healthy credit growth in Japan. The role of the RCC in the corporate restructuring process is examined in detail in Chapter 4, "The Resolution and Collection Corporation and the Market for Distressed Debt in Japan," by Kenneth Kang. The chapter outlines the current operations of the RCC, and how it is supporting the government's objective of accelerating the removal of NPLs from bank balance sheets. Drawing on other countries' experiences with asset management companies, the chapter examines the role the RCC should assume in the corporate restructuring process in Japan, and outlines recommendations on how the RCC can play a more effective role in transferring NPLs from banks to the private sector and help to strengthen the existing market for distressed debt. In Chapter 5, "Structural Reforms, Information Technology, and Medium-Term Growth Prospects," Tim Callen and Takashi Nagaoka examine Japan's productivity performance during the 1990s. As productivity levels in many domestic sectors of the economy are well below international best standards, there appears to be considerable scope for raising productivity and growth in Japan over the medium term. Indeed, empirical studies have estimated that considerable benefits—anywhere from 2¼ percent to 18¾ percent of GDP—could accrue over the medium term from implementing a comprehensive reform program. The chapter highlights four particularly important areas—the labor market; entrepreneurship; the regulatory structure and competition policy; and the information technology (IT) sector—and assesses the reforms that have been implemented to date and what more needs to be done. The first chapter of the fiscal policy section of the book is "Population Aging: Its Fiscal and Macroeconomic Implications" by Hamid Faruqee. Demographic changes—a rapidly aging and shrinking population—will be a prominent feature of the Japanese economic landscape in the coming years, and will have important implications for economic and fiscal developments. In this chapter, demographic dynamics and the social security system are incorporated into MULTIMOD—the IMF's multicountry macroeconomic model—and simulations conducted to examine the economic implications of population aging in Japan, as well as the policies designed to address it. The results suggest that demographic changes will likely result in slower output growth over the next half century (relative to the case of no demographic change), although saving rates and the current account ratio need not decline significantly. In terms of policy implications, the analysis highlights the importance of taking into account prospective changes in the macroeconomic environment when evaluating policies that address the challenges posed by population aging, as well as the impact of reforms on private sector behavior. For example, the simulations suggest that reforms to social security benefits could have a large effect on private saving as agents anticipate having to finance more of their own consumption in retirement. In Chapter 7, "Fiscal Policies During the Demographic Transition," Martin Mühleisen examines the policies that could help restore fiscal sustainability in Japan in the face of the ongoing unfavorable demographic trends. Building on the model developed in Chapter 6, detailed simulations of the fiscal accounts in Japan are used to address a number of issues: (1) the degree of fiscal adjustment needed to stabilize public debt over the medium term; (2) the output costs of alternative fiscal strategies to achieve that target; (3) the implications of demographic developments for public finances under the present policy framework; and (4) reforms that would safeguard the viability of the social security system while mitigating the impact on economic growth. The simulation results suggest that strong policy adjustments will be needed to put Japan's public finances back on a sustainable footing. Cuts in public investment, base-broadening measures for income taxes, some increase in the consumption tax, and reductions in social security benefits are likely to be the key building blocks of a solution to the difficult fiscal situation. The issue of the effectiveness of fiscal policy as a demand management tool is taken up by Sanjay Kalra in Chapter 8, "Fiscal Policy: An Evaluation of Its Effectiveness." The persistence of slow growth in Japan since the early 1990s despite rising structural budget deficits has led some observers to question whether fiscal policy is able to provide even a short-term stimulus to economic activity in Japan in present circumstances. In this chapter, structural vector autoregressions are used to derive dynamic fiscal multipliers for government revenues and expenditures to assess the impact of budgetary policies on economic activity. The results suggest that fiscal policy still has a role as a countercyclical demand management tool. Short-run fiscal multipliers are positive, and actually do not appear to have changed much over time. Fiscal multipliers at longer time horizons, however, are found to have declined significantly, and the chapter argues that this is likely due to changes in the composition of government spending, which has reduced the economic impact of such expenditures. Specifically, public investment has increasingly been focused on expanding social infrastructure and capacity—mostly related to agriculture and rural road construction—which have little flow-on effect to private activity, while government consumption has become more concentrated on health care and less on the provision of economic services. In Chapter 9, " The Zero-Interest-Rate Floor and Its Implications for Monetary Policy in Japan," Ben Hunt and Doug Laxton use the Japan block of MULTIMOD to investigate the implications of the zero bound on nominal interest rates for the design of monetary policy, and the effectiveness of different policy interventions to stimulate the economy when short-term nominal interest rates are at their floor. The results of the simulations presented in the chapter suggest that the Bank of Japan should commit to achieving a target rate of inflation above 2 percent to significantly reduce the probability that the zero bound on nominal interest rates will again become binding, and that macroeconomic performance will consequently suffer. In terms of the different policy responses considered, one-off fiscal and monetary policy interventions are both found to be effective in stimulating the economy even when the zero bound is binding. However, a monetary policy response—through a credible commitment to future inflation—results in a better outcome for the government debt-to-GDP ratio. The impact of quantitative monetary easing on activity and prices is taken up by Taimur Baig in Chapter 10, "Monetary Policy in a Deflationary Environment." The chapter first looks at deflationary episodes in Sweden and the United States in the 1930s, and argues that these episodes suggest more aggressive and sustained quantitative easing than has so far been undertaken by the Bank of Japan could be helpful in ending deflation. It then uses reduced-form vector autoregressions (VARs) to examine the monetary policy transmission mechanism in Japan when nominal short-term interest rates are at their floor. The results from the VARs indicate a potentially favorable impact of quantitative easing on demand and prices through the asset price or portfolio rebalancing channel. Moreover, the results suggest that, while banking sector weaknesses dampen the effectiveness of monetary policy, they do not completely short-circuit the transmission between base money and other economic variables. The authorities' heavy intervention in the foreign exchange market to counter the sharp appreciation of the yen during May and June 2002 has again raised questions about the effectiveness of sterilized foreign exchange intervention. This issue is taken up in Chapter 11, "The Yen-Dollar Rate: Have Interventions Mattered?" by Ramana Ramaswamy and Hossein Samiei. An interest rate arbitrage rational expectations model of the exchange rate and a probit model of the probability of interventions are estimated to assess the effectiveness of intervention in the yen-dollar market since the mid-1990s. The results indicate that interventions—even though they are routinely sterilized—have on the whole mattered, and have succeeded on a number of occasions in changing the path of the yen-dollar rate in the desired direction. The chapter argues that this relative success—which is contrary to conventional wisdom—is because interventions influence market participants' expectations of future economic fundamentals and the stance of monetary policy, and erode bandwagon effects in the foreign exchange market. The estimation results also indicate that coordinated interventions are more effective than unilateral ones—and, when successful, have a much larger effect on the exchange rate—while unilateral interventions to weaken the yen have had a lower success rate than unilateral interventions to strengthen the currency. This latter finding is important in the context of the authorities' recent interventions to weaken the yen. The final chapter of the book, "The Impact of Japanese Economic Policies on the Asia Region," by Tim Callen and Warwick McKibbin, examines the trade and financial links between Japan and its regional neighbors, and how these have changed over time. It then uses the G-cubed (Asia-Pacific) model—a macroeconomic model with rich cross-country links—to explore the implications of a number of policies and developments in Japan for the domestic and regional economies. The simulation results suggest that:

Taken together, the papers in this book aim to provide a comprehensive assessment of the current economic situation in Japan, and the policies needed to reverse the economy's long slump. The overall message is that while the Japanese authorities have made an important start in implementing the necessary reforms, much more needs to be done to secure a return to self-sustained growth. Moreover, such a return is urgently needed, not only for Japan's own prosperity, but also to enable Japan to once again play an economic leadership role in Asia and in the global economy. References Bayoumi, Tamim, and Charles Collyns, 2000, Post-Bubble Blues: How Japan Responded to Asset Price Collapse (Washington: International Monetary Fund). Hayashi, Fumio, and Edward C. Prescott, 2002, "The 1990s in Japan: A Lost Decade," Review of Economic Dynamics, Vol. 5 (Special issue, January). Krugman, Paul, 1998, "It's Baaack: Japan's Slump and the Return of the Liquidity Trap," Brookings Papers on Economic Activity: 2 (Washington: Brookings Institution), pp. 137–205. |