| Russia and the IMF | | | |

©2003 International Monetary Fund September 9, 2003 Ordering Information

|

|||||||||||||||||||||||||||||||||||||||||||||

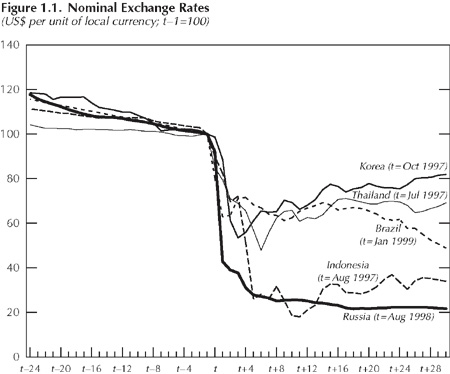

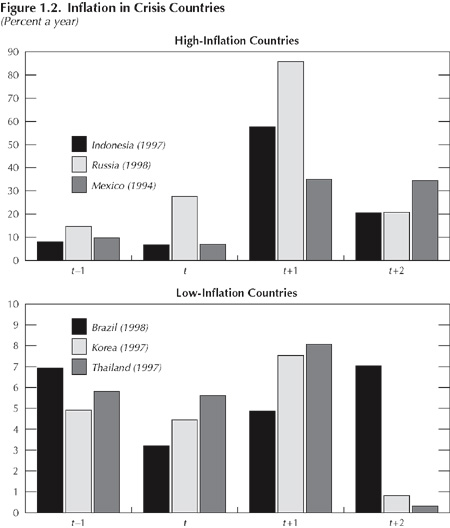

| I. Overview Russia's traditional capacity to puzzle and surprise observers has been revealed again in the economic developments of the past decade. Early in the transition, few outsiders could understand how the population survived such a massive decline in output, the collapse of basic infrastructure, and the nonpayment of wages. Similarly surprising has been the recovery since the financial crisis of 1998. Most observers at the time predicted that it would take many years for Russia to recover from the debt default and ensuing loss of international confidence. Instead, Russia has experienced its first period of sustained growth, and financial markets have become increasingly bullish about Russia's economic prospects, despite a high degree of uncertainty about prospects for the world economy. This recent optimism should not, however, obscure the fact that there are widely divergent views of the nature of Russia's newfound prosperity and the extent to which it reflects fundamental changes in the economy that can translate into sustained growth. In this book, IMF staff put forward their interpretation of the startling swings in Russia's economic fortunes that have marked the past five to six years. The following chapters thus attempt to explain recent developments and identify the key economic challenges that Russia faces. During the spring and summer of 1997, expectations about Russia's prospects reached a high point. Market sentiment surged, boosted in part by President Boris Yeltsin's election victory the previous year, and with the news that, after a long and painful decline in output and living standards, the Russian economy had finally begun to grow and inflation was being brought under control. During this brief period of economic stability and growth, investors overreacted and policymakers misjudged the degree to which they could take advantage of the situation. At that time, emerging markets worldwide were attracting capital from big institutional investors, and Russia was near center stage in this process. The Moscow Stock Exchange suddenly attained the dubious accolade of being the best performing equity market in the world. International capital flowed in in support of Russia's economic potential, even as news of Thailand's difficulties and mounting pressures in Indonesia were beginning to catch investors' attention. Russia successfully warded off the immediate contagion effects from Asia and retained market access for longer than many observers expected. However, it finally succumbed to collapsing confidence and declared a default on its debts in August 1998. The circumstances of Russia's financial crisis—particularly the debt default and the difficulties of reaching political agreement on a coherent rescue plan—sent shock waves through the international financial system. In Russia, the months following the crisis were quite chaotic, bringing forth gloomy predictions of political fragmentation and an end to Russia's great experiment with market economics. The banking system was paralyzed, asset prices plunged, and investors headed, as best they could, for the exits. As in the aftermath of other financial crises around the world, economic output declined, the prices of goods, including those of basic commodities, increased sharply, and many millions of families, vulnerable to these changes, fell back—or further—into poverty. There is a school of thought that crises are necessary evils that provide an opportunity to move away from traditional ways of doing business. It was certainly the case for Russia that the crisis had a marked salutary effect and brought many changes for the better in its wake. Russia did indeed rebound! And the rebound was both faster and stronger than anyone could have predicted in those last months of 1998. Today, after four years of solid growth, the economy is at new heights, international reserves are at record levels, foreign debt is being repaid early, and Russia is again able to tap international financial markets, if it wishes to do so. Expectations are once more on the rise and the Russian equity market is again a top performer in the world. How should one view this latest bout of optimism? There is, at one end of the spectrum, a somewhat unguarded view that the newly prospering Russia has freed itself from the drag of the old Soviet system and is now firmly headed toward catching up to and surpassing the more successful transition economies of Central and Eastern Europe. At the other end of the spectrum, a more skeptical view argues that Russia remains a country where the infrastructure is crumbling, social services are inadequate, and there is still widespread poverty and low life expectancy. The skeptics emphasize that Russia's newfound prosperity is attributable to high world energy prices and a bountiful endowment of oil and gas resources. This view holds that Russia will discover, like many other countries before it, that it is much more difficult than it may seem to translate a richness in resources into well-balanced long-term economic and social development. The objective of this book is to sort some of the wheat from the chaff in this debate. In looking again at the seeds of the financial crisis and its aftermath, and the nature of Russia's more recent "rebound," the book assesses whether the necessary fundamental changes have occurred to protect Russia's economic progress in a more adverse external environment of low oil prices. Can Russia produce goods and services that are competitive in the world market? And, looking ahead, what are the pivotal policy steps needed to ensure sustained and balanced growth for the next generation? This book is about economic policies, but politics and an ideological battle lie not far below the surface at every stage. Russia's search for political and economic identity are inextricably linked and, if the economic rebound has been a surprise, then even more so has been the direction of political change. The growing disillusionment with the inability of former President Boris Yeltsin's government to carry reformist policies through the Duma was integral to the collapse of confidence in 1998. The subsequent ousting of reformers from key economic posts and, later, the rise of the relatively unknown Vladimir Putin to the presidency were initially perceived as unfavorable to building a market economy. However, the contrary has been the case. Following the defeat of the communists and the election of a more pro-reform Duma in late 1999, President Putin's government utilized well its parliamentary support to embark on a well-thought-out and ambitious program of structural reforms aimed at creating a more conducive investment climate for both domestic and foreign investors. Putin's presidency marks a period of relative political stability that has no doubt contributed to the strong economic progress since the crisis. The oft-recited wisdom that economic well-being requires a strong and credible government has never been as forcefully demonstrated as in Russia during the past few years. The Path to Crisis The seeds of the 1998 Russian financial crisis lie in the choice, in the mid-1990s, of a set of policy tools designed to achieve macroeconomic stability, but without a sufficiently strong government in place to make these policy tools effective. Coming out of the immediate post-Soviet period in 1994, Russia had made good progress in putting in place the basic institutional and legislative framework for a market economy. The collapse of the old system and the slow adjustment to the new one had imposed heavy costs in terms of social dislocation, falling living standards, and inequities in the distribution of income and property. A priority—both politically and economically—was to bring down a continuing high rate of inflation, which was still, in 1994, over 300 percent. The emblematic picture from that time was one of pensioners trying to sell bread (which they received in lieu of pensions) to buy other necessities of life. Barter was still prevalent throughout the economy, and the monetary discipline of a market economy had yet to be effected. Arrears between firms were common, and the concept of debt repayment was far from well established and was difficult to enforce through the legal system. The taming of inflation was seen as essential both to normalizing the process of production and exchange and to ameliorating the plight of the poor. The source of inflation was correctly seen to lie in a lack of fiscal discipline—huge government budget deficits were being financed by credits from the Central Bank of Russia. Thus, the attempt in 1995 to lower inflation decisively focused on cutting by half the budget deficit (relative to GDP) and legally prohibiting the central bank from lending rubles to the government for the purpose of deficit financing. To further boost confidence in the government's determination to keep control over money growth, the government also pledged to keep the exchange rate of the ruble, vis—vis the U.S. dollar, within a preannounced corridor, with a depreciation rate well below the inflation rate. Thus, money growth would be limited to what was consistent with keeping the exchange rate within the corridor. In deciding to use the exchange rate as a "nominal anchor" for monetary policy, Russia followed the example of a number of other countries that, after a series of failed attempts to reduce inflation, decided to surrender monetary independence in order to restore confidence in the credibility of government promises. What is noteworthy in reviewing the international experience with the adoption of exchange rate anchors is that, while the immediate results are generally favorable, the longer-term impact is more mixed. The success of an exchange rate anchor ultimately depends on the nature and flexibility of the economy and, critically, whether the government can "change its (fiscal) spots," as well as continue to command credibility in its policies in more adverse periods. This distinction between short-term and long-term implications of exchange rate anchors has led observers to conclude that there is, for most countries, an optimal time when they could make an orderly exit from the anchor. For Russia, as for Argentina more recently, the controversy that followed the 1998 crisis focused on whether an orderly abandonment of the exchange rate anchor (or at least a movement of the peg) would have been possible and desirable ahead of the final collapse. The tightening of monetary policy, supported by the exchange rate anchor, produced in the short term an impressive reduction in inflation and a significant improvement in confidence in the ruble. On the strength of a virtuous circle of monetary discipline, improved confidence, and a sustained increase in the demand for domestic money, inflation was lowered to less than 50 percent in 1996 and to under 15 percent by the onset of the Asian crisis. During this period of increased confidence in monetary policy, Russia took full advantage of the surge in liquidity in international capital markets by allowing foreigners to acquire government-issued paper. The significance of the accumulating debt problem was partially obscured by a relatively strong external current account, rising gross international reserves, which added to market confidence, and an appreciating real exchange rate. During this period, the focus was on the size of the debt stock, which did not seem, compared internationally and at precrisis exchange rates, unduly high in relation to Russia's GDP. However, insufficient attention was paid to the high debtservicing cost, the short-term structure of maturities, and the impact that depreciation of the exchange rate could have on the situation. The underlying problem, however, was that Russia had signally failed to change its spots. The government was unable to come to grips with the fiscal problem. Large-scale tax evasion and huge private capital flight continued even as the government mobilized abundant external financing and high-cost domestic debt to finance its deficits. While it was generally recognized that it would be difficult to strengthen fiscal discipline in the run-up to the 1996 elections, there was an expectation that Mr. Yeltsin's election victory would bring a stronger resolve to tackling the budgetary problems. This hope was, however, frustrated by a string of factors, including the president's ill health, repeated government reshuffles, an increasingly hostile stand-off between the president and the communist-dominated Duma, and a serious weakening of the federal government's enforcement power, especially with major industrial and energy-sector taxpayers and regional governments. The failure to tackle the fundamental problem of fiscal viability was laid bare by the crisis in Asia, which—by contributing to weakening commodity (especially oil) prices—sparked a sharp and sudden deterioration in Russia's terms of trade and substantially increased the cost of its access to, and reduced inflows from, international capital markets. The cumulative fall in terms of trade amounted to about 25 percent from mid-1997 to mid-1998, an annualized cost to Russia's balance of payments of more than $20 billion, nearly one-fourth of exports. Faced with the deteriorating situation, the Central Bank of Russia had to intervene, selling dollars heavily to keep the exchange rate within the corridor. The halving of gross reserves during the year before the crisis in August, despite continued large inflows from the international financial institutions, reflected the extent to which market sentiment had deteriorated. The benefit of hindsight allows one to argue that the exchange rate anchor should have been abandoned earlier. Perhaps there was a window of opportunity for an orderly exit from the policy in the fall of 1997, ahead of the unraveling of events in Korea. Beyond that point, however, there were clearly strong negative consequences to be borne, and the counterfactual question of whether Russia could have avoided a crisis if it had adopted a floating rate at that stage is extremely difficult to answer. Those policymakers and advisors close to the situation would argue, with some justification, that there was still a good possibility of weathering the Asian crisis and avoiding a massive disruption in Russia if the government could have maintained credibility and pressed forward with the needed fiscal adjustment. Absent this fiscal adjustment, it would have made little difference if Russia had exited the peg earlier—the economy would most likely have lapsed into a cycle of depreciation, inflation, and renewed capital outflows. In the event, however, political instability intensified severely in MarchApril 1998 as a result of a further government reshuffle and a presidential clash with the Duma over the choice of prime minister. As had been the case throughout the years leading up to the crisis, the government could not reliably command a majority in the Duma in favor of key economic reform measures. This was illustrated most strikingly when the Duma rejected the key fiscal measures proposed by the government in mid-July 1998 as part of the IMF-supported economic program. Handling the Crisis A more detailed account of the circumstances of the August 1998 crisis and the striking lack of a coherent policy response during the remaining months of that year is given in Chapter 2. The Russian government approached the financial crisis differently than did other countries similarly hit by loss of investor confidence and falling international reserves. Beyond the declaration of an across-the-board suspension of debt-service payments, including on ruble-denominated debt and on private sector external payments, and the adoption of a free-floating exchange rate to preserve remaining reserves, economic policy focused mainly on keeping the payments system operational. This latter objective was achieved through liquidity injections to banks, later supplemented by the transfer of deposits from some of the larger distressed banks to the publicly owned Sberbank. Political differences between the president and the Duma made orderly budgetary revisions impossible in 1998—although, faced with a collapse in revenues, the government resorted to a strict cash management system that saw noninterest expenditures drop sharply through 1998. But it was not until February 1999 that Prime Minister Yevgeny Primakov came forward with a credible economic stabilization program, having as its centerpiece a prudent budget for 1999, which was passed by the Duma. The absence of an active macroeconomic policy response in the first six months following the Russian crisis resulted in a relatively steep nominal-exchange-rate adjustment and a much higher spike in inflation than in most of the other countries that experienced financial crises over the past decade. By February 1999, the ruble had lost some 70 percent of its value against the dollar—a much larger decline than in the other crisis countries with the exception of Indonesia (Figure 1.1). Contrary to the conventional finding that large exchange rate depreciations are generally contractionary and result in lower-than-expected inflation, Russian consumer prices rose very sharply, with inflation averaging about 90 percent in 1999 (Figure 1.2). What separates the Russian experience from other crisis countries seems to have been the delayed macroeconomic policy response and the indiscriminate use of liquidity to support the payments system. Again, Indonesia, which also expanded base money in an attempt to support its banking system, is the only outlier with Russia insofar as the inflationary impact is concerned. At the same time, the initial output collapse that followed the August 1998 crisis in Russia was not as deep as in most other crisis countries. And—counter to most observers' expectations—growth from the initial dip was both quicker and stronger than in other crisis countries. The relative importance of various factors in explaining the quick turnaround in output has been the subject of much debate (described in Chapter 2). At this stage, we would make just a few key points.

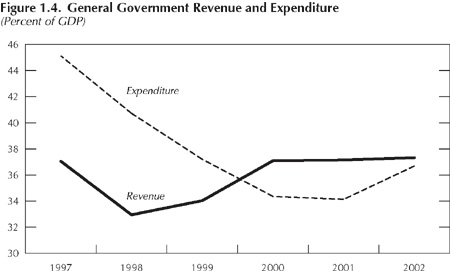

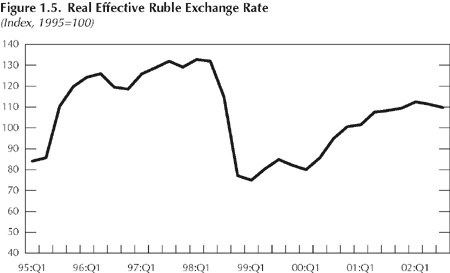

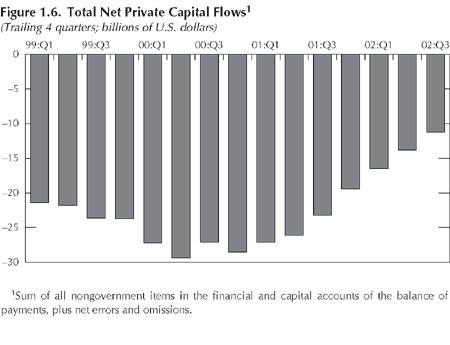

Postcrisis Macroeconomic and Structural Policies What changed most obviously in Russia as a result of the crisis was the degree of responsibility of politicians and policymakers in framing and implementing economic policies and, in particular, fiscal policy. The specter of seemingly unmanageable external debt and the threat of uncontrollable hyperinflation had a sobering impact, allowing Mr. Primakov to secure agreement from the previously intractable Duma on a tough budget for 1999. Importantly, the political consensus forged at that time in favor of budgetary prudence was maintained over the subsequent two years, producing a remarkable fiscal adjustment at the general government level amounting to 10 percentage points of GDP from 1997 to 2001. This achievement partly reflected higher oil revenues, but more than half of the adjustment was due to reductions in expenditures relative to GDP, especially at regional and local levels (Figure 1.4). While political consensus was clearly essential in the approval of tight budgets, it was also key to a striking contrast in the implementation of fiscal policy. Before the crisis, political intervention in the process of tax enforcement abounded. The inability of the government to sanction large tax delinquents made statutory obligations mostly irrelevant for large taxpayers, who independently negotiated their payments with the tax authorities. These tax collection problems were exacerbated by repeated recourse to a policy of offsetting tax arrears against expenditures, especially at regional and local levels, which encouraged politically influential enterprises to accumulate arrears as a means of forcing government demand for their goods and services, often at inflated implicit prices. In contrast, the postcrisis period, beginning with the 1999 budget, has seen a determined effort to enforce tax compliance by large enterprises and abandonment of the practice of using tax offsets at the federal level. This latter initiative has had a major beneficial impact in limiting the extent of barter transactions throughout the economy. The budget of 1999 succeeded in reducing the level of real government expenditures, but at the cost of holding social payments and wages well below inflation. This was not sustainable, and some rebound in real expenditures after the crisis was therefore inevitable. By 2000, with Mr. Putin appointed as acting president, the effects of higher oil prices were beginning to be felt, and the fiscal policy challenge changed to one of not succumbing to the strong pressures to spend all the revenue windfall or to allow energy companies to evade their tax obligations. The main success of fiscal policy during 2000 and 2001 was to resist such pressures. This result was helped at a technical level by greater central control of regional and local government finances while a larger share of tax revenues was channeled through the federal budget. Politically, expenditure restraint was justified by the argument that it was necessary to save resources to cover a spike in scheduled debt service for 2003. Thus, noninterest expenditures were allowed to increase, but not as quickly as oil revenues accumulated, and substantial fiscal surpluses were achieved. While the merits of a prudent fiscal policy is one of the more important lessons of the crisis, the jury is still out on whether this can be sustained. The 2002 and 2003 budgets have accommodated a more marked relaxation of government spending, reflecting substantial increases in real expenditures on recurrent items like wages and pensions, with very little for higher reform-related expenditures and investments. In addition, nonenergy taxes have been declining slightly as a percentage of GDP, reflecting the impact of tax reforms. There is clearly a strong appetite among politicians for further reductions in the tax burden. While fiscal policy remains under control, with a small surplus budgeted for 2003, strong political resolve will be needed to resist further slippage, in the form of either higher recurrent expenditures or further substantial reductions in the tax burden. Otherwise, the fiscal transformation of recent years could just as quickly be reversed in the face of a downturn in oil prices or a slowdown in growth. Fiscal restraint in the face of burgeoning oil revenues allowed the government to quickly rebuild international reserves while slowing the real appreciation of the ruble. By accumulating government deposits that to a significant extent offset the monetary effects of the central bank's massive purchases in the foreign exchange market, the government was, in a sense, mimicking the operations of a successful oil stabilization fund. Compared with a stabilization fund, however, the government retained full discretion over the level of savings and was, therefore, faced in each annual budget with the sensitive problem of projecting oil prices for the coming year. Fortunately, in both 2000 and 2001, oil prices exceeded projections and, with growth and inflation also higher than expected, budgetary surpluses turned out to be much larger than originally targeted. These budgetary surpluses relieved the Central Bank of Russia from having to pursue a more active monetary policy. As a result, the primary goal of the central bank during most of the postcrisis period was to accumulate reserves and prevent nominal appreciation of the ruble despite the massive current account surpluses. Guiding down inflation was an important, but secondary, objective. Monetary growth targets were usually overshot by large margins (Table 1.1). Fortunately, however, demand for money also grew much more rapidly than expected during this period, as confidence in the ruble and the banking system rebounded from the lows reached after the crisis. As a result, despite overshooting monetary growth, a gradual reduction in inflation was achieved, albeit less rapidly than targeted. The revealed preference of the central bank was therefore to err on the side of allowing real appreciation of the exchange rate—something they knew was inevitable, following the huge depreciation in 1998—to occur through relatively high inflation (compared with competitors) rather than through nominal appreciation of the ruble. They also believed that, through this choice, they could achieve a more gradual real appreciation than would have occurred had they allowed the nominal rate to appreciate. This is difficult to prove, one way or the other. However, given the difficulty of forecasting the process of remonetization and uncertainty about the sustainability of the output recovery, the central bank's support for the government's growth strategy through depreciating the ruble/dollar rate while ensuring that inflation was on a downward path was arguably appropriate—at least through 2001. Price increases, however, continued in the 1525 percent range—well in excess of trading partners' rates—leaving Russia at the end of this period still with the task of reducing inflation to single digits—a task that has proven to be difficult for many other emerging market and transition countries. Thus, despite the strong fiscal adjustment, the fundamental pressures for the ruble to appreciate in real terms could not be fully resisted in the face of the extremely strong balance of payments. By end-2002, the real effective exchange rate had appreciated to a level only about 20 percent below its precrisis level (Figure 1.5). As the initial competitive advantage from the depreciation moderated, the primary impetus and driver of economic growth changed from net exports to domestic demand and, in particular, to buoyant domestic consumption. The economy has continued to expand, but it is apparent to policymakers and observers alike that reliance on consumption is not a firm basis for generating the sustained high rates of economic growth needed to catch up to the more-advanced transition economies. Moreover, growth has been narrowly based, driven by natural resource and closely related sectors, while non-energy-related exports and investments have stagnated. Indeed, from early in the Putin presidency, it was recognized that while dramatic changes had occurred in the Russian economy compared with Soviet times, sustaining future growth would depend on productivity increases that could not be achieved without a program of wide-ranging structural reforms, needed to create a more dynamic market economy. During the precrisis period, and in the immediate aftermath of the crisis, structural reforms were largely put on hold. However, with the strengthening of proreform parties in the Duma elections at end-1999, preparations began to restructure the economy on a broad front. By 2001, the first fruits of this initiative began to appear and there was, during that year, an impressive acceleration of structural reforms—although given long implementation periods and important synergies with other reforms that have not yet been implemented, it is too soon to judge the effectiveness of these measures. As described in detail in Chapters 3 and 4, bold tax reforms, involving lowering and unifying tax rates and abolishing exemptions, overhauled the previous arbitrary and irrational tax system, giving Russia a flat 13 percent income tax, a much reduced profit tax rate, and a greatly simplified system. Legal reforms were launched, aimed at fundamentally transforming the judicial system, with the changes in the economic sphere involving a separation of criminal and commercial processes and much-improved arbitration procedures. The Soviet-era labor and land codes were replaced, putting on a sound legal basis private employment and the sale and ownership of land. Deregulation reduced the number of licensed activities, sought to limit intrusive inspections by corrupt officials, and made registration of new businesses a one-step process, while a new pension system introduced a fully funded private pillar. In the financial area, the legislative frameworks for bank supervision and for combating money laundering were strengthened, and there was some limited deregulation of the foreign exchange system. The progress on structural reforms slowed significantly in 2002. While the spring session of the Duma that year passed reform legislation in several important areas—such as a new bankruptcy law, an agricultural land law, and further pension reforms—some other scheduled reforms were postponed and opposition to reforms—particularly to World Trade Organization (WTO) accession and natural monopoly restructuring—became more vocal. The prospect of parliamentary elections in 2003 and the presidential election in 2004 appears to have dampened the political will to push forward with reform legislation, although President Putin has continued to call for structural change, particularly with respect to civil service reform, and at times has expressed impatience with government ministers over lack of ambition in the economic program and growth projections. Challenges Ahead The acceleration of reforms in 200102, against a background of prudent macroeconomic policies, translated quickly into greater confidence among financial investors. Spreads on Russian bonds have significantly narrowed and Russian equities have outperformed most other markets. International reserves—nearly $50 billion at end-2002—are viewed not only as a comfortable cushion against temporary adverse developments, but also as sufficient to provide policymakers with room for maneuver in the face of more permanent shocks. Similarly, Russia's external debt—at about 40 percent of GDP—is no longer regarded as a prime source of vulnerability, especially as rescheduling agreements have resulted in a favorable maturity structure that stretches through 2030. Although concerns are expressed that an extended period of very low oil prices would jeopardize growth prospects, the market's view is that near-term risks for Russia are for now quite modest. The clearest reflection of this judgment is that the trend of private capital flows in the balance of payments—dominated for many years by massive capital outflows—appears to have changed course in 200102, with significant reductions in outflows and a surge of inflows, including higher borrowing and asset reallocation by the large state- and private-owned Russian corporates (Figure 1.6). The balance of payments pressure for the ruble to appreciate has thus increased, reflecting both current account pressures from the relatively prolonged period of high world energy prices and, more recently, capital account pressures. The turnaround in the capital account reflects two distinct factors, both of which are underpinned by perceptions of political stability and the low likelihood of default. The first of these factors is the substantial interest rate differential between Russian and world financial assets, which, when coupled with an expectation that the exchange rate will not depreciate much, represents a highly profitable opportunity for those with access to Russian financial assets. The second, and perhaps more important, factor is the improvement in the investment climate and reassessment of growth prospects that has been brought about by recently implemented or anticipated structural reforms. At this stage, information is incomplete concerning the nature of new capital inflows, but these appear to be largely directed, in the first instance, toward financial assets. The crucial question—to which the answer is as yet unclear—is to what extent the higher private capital inflows will translate into a significant increase in productive investment. Capital flows, of course, need to be welcomed insofar as they contribute to the productive capacity of the economy. However, if they do not (and given the lack of a developed financial system, they may not), then a buildup of short-term foreign claims will ultimately be costly and simply make it more difficult to deal with future adverse shifts in the external environment. Against this background, Russian policymakers—striving to sustain healthy growth and stimulate investment and employment in the non-oil sector of the economy—are faced with a number of fundamental trade-offs. In the macroeconomic area, critical choices need to be made concerning

The resolution of these issues, along with conditions in world energy markets—in particular the risks associated with a sharp drop in oil prices—will effectively shape the direction of fiscal, monetary, and exchange rate policies over the coming years. On the first of these issues—inflation reduction—Russian policymakers do not dispute the merits of securing a low and steady rate of inflation. This is correctly viewed as a crucial element in moving toward more investment-based growth. They also recognize the risk that by delaying the reduction of inflation to low levels, inflationary expectations may become entrenched, increasing the costs, in terms of lost output, of subsequent disinflation efforts. Nonetheless, economic policymakers have in the past accorded secondary importance to this objective, fearing that too fast a disinflation would have a short-term negative impact on growth. Moreover, there has been little political concern about inflation as long as it has not exceeded 2025 percent. Monetary policy has thus tended to be passive in dealing with inflation and dominated, instead, by the objectives of accumulating reserves and preventing nominal appreciation of the ruble. Arguably, the approach followed by Russia's central bank of allowing real ruble appreciation to take place through inflation, rather than through nominal exchange rate movements, was a justifiable policy choice, given imperfect information. And, indeed, a steady decline in inflation has been achieved under this policy. Looking ahead, however, the situation will in all likelihood call for a more actively disinflationary monetary policy, particularly if balance of payments pressures from both the current and capital accounts persist. Importantly, policymakers need to take account of the fact that pressures on the ruble that arise from uncovered interest parity can be partially relieved (and vulnerability to future capital flight reduced) if inflation and nominal interest rates can be lowered nearer to world levels so as to prevent excessive capital inflows. Taking account of the current structure of the banking system and the limited domestic bond market, the capacity of the central bank to effectively sterilize its purchases of foreign exchange is limited. In addition, sterilized intervention to resist nominal appreciation is costly and ultimately becomes self-defeating, as the higher interest rates associated with sterilization tend to attract more inflows. These factors mean that if the balance of payments continues to strengthen, the central bank will at some point be confronted with a choice between accepting nominal appreciation of the ruble or accepting higher inflation. The economic arguments for taking the former course appear strong, but in practice there is a significant risk that policymakers will respond too late to inflationary pressures, particularly given the public's apparent tolerance of moderate inflation and the opposition of the powerful industrial lobby to the nominal strengthening of the ruble. Continuing with relatively high inflation will, however, over the medium term, redound to the severe detriment of the development of the non-oil sector. The focus of policymakers is rightly on the real value of the ruble. Over the long term, the real exchange rate is determined by real economic factors—typically, the rate of productivity growth in a country compared with its competitors and the world prices of major export commodities—in Russia's case, especially the prices of oil and gas.1 Monetary policy is not generally effective in influencing the real exchange rate in anything other than the short term. Fiscal policy can, however, have a more durable impact, with tight fiscal policy generally regarded as effective in helping to resist pressures for real appreciation. With a strong expectation of large balance of payments surpluses over the next few years, a trend toward real appreciation is likely, possibly at a rate far in excess of the productivity growth that can be achieved over the same period. Although this trend cannot and should not be fully resisted, the authorities can slow the real appreciation, but their ability to do so hinges fundamentally on the stance of fiscal policy and, specifically, on the generation of future budgetary surpluses. Given the loss of competitiveness already experienced since the crisis, a pragmatic approach for Russian policymakers now would be to implement policies aimed at minimizing the difference between the rate of real ruble appreciation and estimated productivity growth for the economy. This is likely, however, to imply, over a range of different assumptions, the need for continuing fiscal surpluses during the next 45 years. Only in the event of a large and sustained decline in oil prices, accompanied by a reversal of private capital flows, would a significant reduction of the fiscal surplus be justified. The major problem with such advice is that, politically, it will be very difficult to resist spending pressures if oil prices remain high—especially with the approach of the 2003 and 2004 elections. The recent practice of saving oil revenue "windfalls" has been helpful in slowing the loss of competitiveness from the 1998 depreciation, but the fiscal surpluses of 19992002 were rationalized not on these grounds but as a means of saving resources to meet a spike in debt service in 2003. This is no longer a relevant argument, and policymakers, if they wish to pursue the approach of maintaining fiscal surpluses, will need to provide a different rationale. The proposal to establish a formal oil stabilization fund is one way forward toward building a political consensus for conservative fiscal policies, which would serve Russia best in the face of strong balance of payments pressure. Such proposals should be welcomed provided the operation of such a fund is properly integrated with overall fiscal policy, managed with transparency and accountability, and the use of resources from the fund is subject to democratic scrutiny. The third critical macroeconomic policy issue for Russian policymakers is how to deal with capital inflows. Sustained capital inflows—if they are sensitive to interest rates—give rise to the policy dilemma noted above, in that nominal appreciation cannot be effectively resisted for long through sterilized intervention alone. The principal macroeconomic policy response to excessive capital inflows should be, as outlined above, fiscal tightening combined with an appreciation of the nominal exchange rate to help reduce inflation. Beyond the conduct of fiscal and exchange rate policy, however, there are some additional steps that will be important in ensuring that Russia preserves the safeguards against vulnerability that it has built up since the 1998 crisis. It will be important to implement a comprehensive monitoring system with special attention being paid to the external borrowing of local governments as well as public and quasi-public enterprises. Centralized control over the different forms of public or publicly guaranteed external borrowing, including discretionary quantitative limits as necessary, should be maintained and implemented in a strict manner. For private external borrowing, at a minimum, full information needs to be gathered and published. And, to the extent that such borrowing is intermediated through the domestic banking system, it will be important to ensure the appropriateness and effectiveness of implementation of prudential regulations covering the on- and off-balance-sheet risks of commercial banks. There are other possible policy responses to excessive capital inflows—for instance, the introduction of Chilean-style inflow restraints or other regulatory instruments. Most measures like these, though, tend to be effective only on a temporary basis and should be considered only if the problem of volatile capital inflows worsens significantly. A more important consideration at this stage is how to ensure that capital flows translate into new investment and support productivity growth. More generally, policies need to encourage broad-based growth, to reduce the dependence on oil and thus limit the downside risks associated with a future drop in the oil price. This will depend on the government's ability to sustain and widen the progress it has made on structural reforms, especially those required to reduce the formidable barriers that currently stand in the path of both foreign and domestic investment. The structural changes that have been initiated under President Putin's leadership have been well received and have improved investor sentiment, but they have pointed up three facts. First, there should not be an expectation of an immediate direct impact on growth. Legislation alone is certainly not sufficient as many structural reforms require behavioral changes—which take time—and in the initial stages there are often wide gaps between legislative intent and actual implementation. The slow progress in implementing reforms has produced some disappointment in Russia and focused attention on the need for civil service and judicial reforms to be accelerated, as prerequisites for the effectiveness of other structural changes. Both of these reforms are, however, recognized as complex and long-term tasks. Second, many of the structural reforms on the government's agenda are interrelated and complementary. Ironically, recent achievements have also drawn attention to how extensive is the list of unfinished reforms considered essential for encouraging private investment. It is common to hear the argument that to achieve significant results, there needs to be a "critical mass" of reforms. Although such a concept is difficult to define with any precision, Russia is widely regarded to be several years away from such a point. Third, gaining political consensus takes time, and the Duma has limited time for considering highly complex and technical issues. Reforms, therefore, need to be adroitly introduced in a phased manner with the political ground well prepared in advance, including at the local level where reforms are actually implemented. At the same time, the opposition to reform, particularly from industrialists with market positions to protect, has become more sophisticated, better organized, and more influential. In view of these considerations, it is not surprising then that the reforms already adopted have done relatively little to overcome the barriers to new investments. The Russian economy remains highly dependent on a few large enterprises whose main business is the extraction of natural resources. Incumbent companies in other sectors are often able to rely on monopolistic market positions to gain excessively high profits, protected from competition and pressure to develop new products. The limited expansion of nonenergy exports, even with a highly depreciated exchange rate in the wake of the crisis, points not only to lack of experience and limited knowledge of foreign markets, but also to the absence of domestic competition. Experience from other transition economies shows that an important component of achieving rapid and self-sustained growth is the emergence of new small and medium-sized enterprises. But the share of such dynamic enterprises remains very low in Russia and shows little sign of growing. The conclusion to be drawn from this is that, while a short-term payoff should not be expected, reforms need to be directed toward decisively improving what remains a very inhospitable investment climate for newcomers—domestic and foreign investors alike. The many formal and informal barriers to the establishment of new businesses and the various ways that the economic system continues to favor incumbent, often inefficient, enterprises are generally well known.2 To overcome these problems, priority must be given to civil service and administrative reforms, reform of the natural monopolies, reduction in trade barriers, and the development of the banking system and financial markets. Perhaps the biggest obstacle to new enterprises is the still exceptionally intrusive role of government in Russia, especially at regional and local levels. Despite the recent deregulation measures, a pervasive system of government licensing, inspection, and authorization requirements allows corrupt bureaucrats and politicians considerable scope for extracting exorbitant bribes from those wishing to set up new businesses or for keeping out new competitors. Deregulation must continue, but will have limited impact unless accompanied by civil service and administrative reforms. Past experience shows that without bold scaling back and rationalization of government at all levels, corrupt officials will find ways to extract high rents from the activities that, even after deregulation, will remain subject to their approval and authorization. Large layoffs, much higher salaries for those remaining on the public payroll, the abolition of overlapping government functions, and wholesale elimination of many functions should be among the key elements of such reforms. Prices charged by natural monopolies—notably in the electricity, gas, and railways sectors—entail high subsidies that keep inefficient enterprises alive. The subsidies are often provided on a discriminatory basis, favoring large incumbent enterprises at the expense of newcomers. Energy subsidies are a particularly serious problem. Russia inherited many inefficient, energy-intensive enterprises, reflecting the fact that an abundant endowment of energy resources led to an industrialization strategy in the Soviet Union that promoted such enterprises with little regard to energy prices. A gradual increase in energy prices is required to force such enterprises to restructure. While the natural monopolies themselves are wasteful, concern that higher revenues will reduce pressures on the monopolies to restructure should not delay price increases. Instead, higher revenues should be taxed away if their efficient use cannot be assured. In addition to price increases, natural monopoly reforms should involve privatization of potential competitive activities and restructuring of the naturally monopolistic functions that are to be kept under government control. Such reforms must go hand in hand with the long-delayed communal reforms, which will require substantially higher prices for most consumers in order to increase cost recovery from very low levels—especially for heating and housing—to ensure appropriate maintenance expenditures in these areas, together with well-targeted income support for those with the lowest incomes. Reduction in import barriers is a particularly effective means of forcing Russian enterprises to restructure by exposing them to competitive pressures. With WTO membership now a political priority, the challenge facing the authorities is to resist attempts by enterprises to delay such pressures by calling for unduly long transitory arrangements. A decision in late 2002 to impose prohibitively high tariffs on the import of used cars is an example of the difficulties the government is having in resisting such pressures. Calls for protection, even by white-collar sectors like insurance and finance, are getting a sympathetic hearing from some officials. Trade liberalization is an area where the authorities will have an opportunity, sector by sector, to significantly increase competitive pressures as WTO membership draws closer. The absence of a well-functioning banking and financial system that effectively intermediates between savings and efficient investment opportunities is central to the skeptic's view that Russia will be unable to convert its rich endowment of natural resources into broad-based economic growth. And broad-based growth is required if the economy is to reduce its dependence on oil. Developing a sound banking system will take a long time, dependent as it is on fundamental improvements in corporate governance and the ability to enforce legal contracts. But the government must begin by reforming the still-dominant state banks. The experience of other countries suggests that such dominance means that available resources tend to be channeled primarily to large incumbent enterprises, at the expense of new enterprises. These reforms, described in greater detail in Chapter 3, constitute a strong test of the government's determination to change the structure of the economy. To a much greater degree than has been the case for reforms adopted and implemented so far, the reforms that still lie ahead will be costly to those directly affected. Bureaucrats, corrupt officials and, not least, the companies that benefit from crony capitalism will strongly resist civil service and administrative reforms, restructuring of monopolies, and reductions in import barriers. Many sectors are already coming out against WTO membership, and local governors are busy mobilizing opposition to the reforms of the electricity sector, which will deprive them of a major mechanism for providing quasi-fiscal subsidies to favored enterprises. Communal reforms will be painful to the majority of the population, even with the provision of a social safety net for those most in need. Without progress in structural reforms, it will be difficult for Russia to achieve sustained and balanced growth over the longer term. This is not to say that the Russian economy will necessarily fall back into stagnation unless reforms are implemented fast. With steady and gradual progress in effective implementation, reasonable growth rates and a rising investment ratio can be achieved, given the cumulative impact on the investment climate of the reforms to date, continued surpluses from the oil and gas sector, and the beneficial effects of political stability. There is still substantial room for improvement in productivity, which can be achieved with moderate increases in investment. However, for Russia to achieve its full potential, deeper reforms will be essential to stimulate new small and medium-sized industries to provide the country with a new dynamism. ReferencesBroadman, Harry G., 2002, "The Regional Dimensions of Barriers to Business Transactions in Russia: An Overview," in Unleashing Russia's Business Potential: Lessons from the Regions for Building Market Institutions, World Bank Discussion Paper No. 434, ed. by Harry G. Broadman (Washington: World Bank). Claessens, Stijn, and Esen Ulgenerk, 2002, "Corporate Finance in Russia's Regions: Demand and Supply Constraints," in Unleashing Russia's Business Potential: Lessons from the Regions for Building Market Institutions, World Bank Discussion Paper No. 434, ed. by Harry G. Broadman (Washington: World Bank). Spatafora, Nikola, and Emil Stavrev, 2003, "The Equilibrium Real Exchange Rate in a Commodity Exporting Country: The Case of Russia," IMF Working Paper 03/93 (Washington: International Monetary Fund). 1See Spatafora and Stavrev, 2003. 2A catalogue of the barriers hindering investments, based on a comprehensive enterprise survey, is provided in two recent studies by World Bank staff (see Broadman, 2002, and Claessens and Ulgenerk, 2002). |