(Version in Español, Français, Português, Русский, 中文 and 日本語)

There are a trillion reasons to care about who owns emerging market debt. That’s how much money global investors have poured into in these government bonds in recent years —$1 trillion. Who owns it, for how long and why it changes over time can shed light on the risks; a sudden reversal of money flowing out of a country can hurt. Shifts in the investor base also can have implications for a government’s borrowing costs.

What investors do next is a big question for emerging markets, and our new analysis takes some of the guesswork out of who owns your debt. The more you know your investors, the better you understand the potential risks and how to deal with them.

Some of the facts

We compiled comparable and standardized estimates of the investor base of emerging markets’ government debt using the same approach we designed last year to track who owns advanced economy government debt.

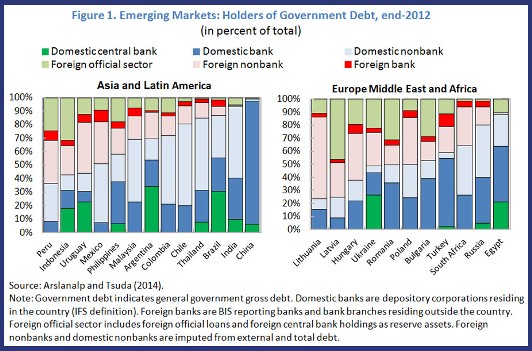

We use data from 24 emerging market countries and we’ve made it available for anyone interested in further research (Figure 1). The data covers the period from 2004 through June 2013.

By our estimates, half a trillion dollars in foreign investment poured into emerging market government bonds from 2010 until 2012 alone, most of it from foreign financial institutions that aren’t banks (large institutional investors, hedge funds, sovereign wealth funds). These investors held about $800 billion of the debt—80 percent of the total—at end-2012.

We also calculate that foreign central banks held about $40 to $80 billion of the debt, and their holdings appear to be concentrated in seven countries: Brazil, China, Indonesia, Poland, Malaysia, Mexico and South Africa.

Why this money poured in to emerging market economies over the last decade is partly related to improvements in public debt management. In particular, emerging markets have extended the maturity of their debt profile, cut down issuance of floating rate debt, and reduced foreign currency debt. This made their public balance sheet more resilient to exchange rate and interest rate shocks, and reduced risks on the supply-side of government debt. Partly as a result, foreign interest in emerging market government debt rose sharply in recent years.

Rising foreign participation in emerging market government debt markets creates opportunities and new risks, notably on the demand side. Rising foreign participation in government debt markets can help reduce borrowing costs and spread risks more broadly among investors, but it can also raise external funding risks for countries. Moreover, having a view of investors across countries is essential for understanding the dynamics of global demand for government debt. Changes in global investor’s allocations among countries are important because they can affect many countries all at once.

Before, during and after the global financial crisis

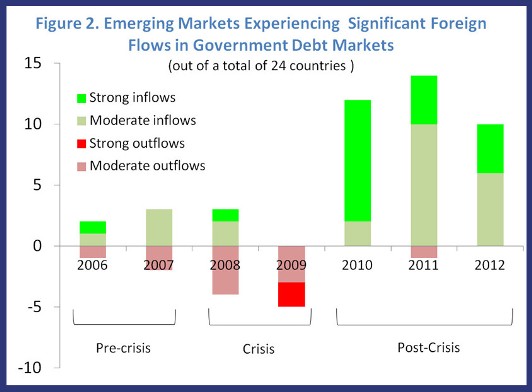

We found that foreign investors distinguished among emerging market economies in three distinct periods—before, during and after the global financial crisis. Before the crisis, they showed moderate differentiation among countries: some received inflows while others faced outflows. As it usually happens, this differentiation became much sharper during the crisis. However, during the third period (2010–12), we found that foreign flows became almost always positive and much less differentiated (Figure 2).

Part of these inflows can be explained by improving economic fundamentals in a number of emerging markets in this period. Five emerging markets reached or regained investment grade status during 2010–12: Colombia, Indonesia, Latvia, Romania, and Uruguay. Most emerging markets weathered the crisis well, with a relatively quick return to high growth. This may have raised expectations of currency appreciation in emerging markets, attracting further demand from foreign investors. At the same time, even countries whose credit ratings deteriorated or did not improve during this period continued to receive inflows against the background of near-zero interest rates in advanced economies.

Emerging markets can prepare

Last year we developed a framework to examine how potential sudden stops in foreign money may impact government debt markets. In our new analysis, we’ve run illustrative scenarios to see what might happen under different circumstances. We designed these to assess the impact of a shock, not to predict the likelihood of one.

The scenarios show that, for a given level of foreign participation in government bond markets, countries with the following characteristics would be less sensitive to external funding risks:

- lower debt-to-GDP ratio

- lower gross financing needs

- more developed domestic financial systems

- larger liquidity buffers to protect against external shocks.

So the scenarios illustrate the importance of extending the maturity of government debt, developing a local investor base, and maintaining liquidity buffers to mitigate the potential harm from a sudden outflow of foreign funding. Countries that had these mitigating measures, such as Mexico and Poland, faced less pressure on bonds yields during the summer of 2013, despite having higher foreign ownership of government debt.

For all these reasons, emerging markets need to carefully track who owns their debt and for how long. They need to beef up their communications with their investor base to understand their needs.

Understanding the benefits and risks of foreign ownership in emerging market debt is key. Is there some perfect mix of domestic and foreign investors? Stay tuned for the upcoming analysis in the next issue of the Global Financial Stability Report for more on that.