(Versions in Español)

Emerging market economies have been experiencing strong growth, with annual growth for the period 2000-12 averaging 4¾ percent per year—a full percentage point higher than in the previous two decades. In the last two to three years, however, growth in most emerging markets has been cooling off, in some cases quite rapidly.

Is the recent slowdown just a hiccup or a sign of a more chronic condition? To answer this question, we first looked at the factors behind this strong growth performance.

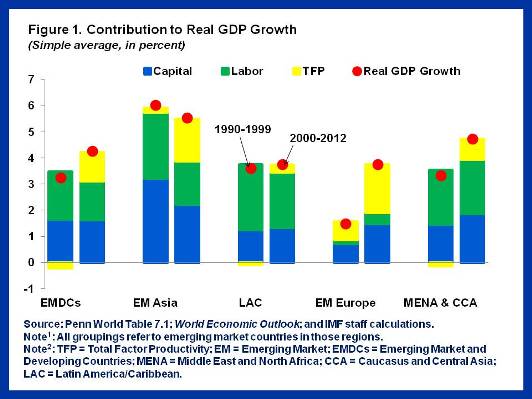

Our new study finds that increases in employment and the accumulation of capital, such as buildings and machinery, continue to be the main drivers of growth in emerging markets. Together they explain 3 percentage points of annual GDP growth in 2000–12, while improvements in the efficiency of the inputs of production—which economists call “total factor productivity”—explain 1 ¾ percentage points (Figure 1).

We also found that the pickup in economic activity in the 2000s compared to the 1990s is solely explained by higher total factor productivity. After exhibiting declines in Latin America and the Middle East and North Africa in previous decades, total factor productivity is now on the rise in emerging market economies in all regions (see our previous blog for a targeted discussion on Latin America).

This is not an unusual development during good economic times. However, the improvements in productivity also reflect some structural (permanent) factors, such as the reallocation of inputs to more productive sectors and gains from past reforms (including from deregulation as well as trade and financial liberalization). All this is good news for emerging markets.

Lower potential growth

After identifying the causes of emerging markets’ strong growth performance in the 2000s, we turned to the question of whether the slowdown warrants a “doctor’s visit” or if it’s just a case of the hiccups that will subside.

In a previous blog, we showed that external factors account for a considerable part of this slowdown, although domestic factors also play a role. Whether the slowdown will persist depends on whether it has been driven by transitory (cyclical) or more permanent (structural) factors. Our study suggests that on average, cyclical and structural factors are equally important in explaining the growth slowdown in emerging markets over the last few years (Figure 2).

Is this good or bad news for global economy? Well, it implies that some of the slowdown in emerging markets—the cyclical part—would be just a hiccup, and that stronger growth should resume once growth picks up in advanced economies.

At the same time, our results suggest that emerging markets will have more difficulty sustaining the high growth rates of the 2000s in the next 3-4 years, as some of the slowdown reflects lower potential growth and is thus more permanent in nature. Estimates of potential growth rates in emerging markets for the next 3-4 years, at 3½ percent, suggest that growth would be on average 1¼ percentage points lower than so far in the 2000s, though the magnitude of the impact varies by country (Figure 3).

Several factors explain the anticipated slowdown in potential growth. First, investment (that is, the growth of the physical capital stock) is expected to moderate, as global interest rates which earlier facilitated large capital flows to emerging markets start to rise and commodity prices stabilize. In addition, natural constraints such as population aging will likely limit the contribution of labor in the coming years. Finally, in countries where external and financial imbalances were allowed to build, growth will have to slow as economies address risks to their balance sheets.

Structural reforms to the rescue

As a result, policymakers in emerging market countries will have to place renewed emphasis on structural reforms to raise productivity, which despite recent improvements remains relatively low compared to advanced economies (see a recent IMF paper for a discussion of tailored structural reforms).

So, where does this all leave us? The slowdown in emerging markets is not just a temporary phenomenon that will correct itself with minimal policy intervention. In some countries, transitioning towards a slower potential growth rate may be desirable if this means moving to growth rates that are more sustainable and balanced.

However, in other emerging markets, this may be an opportune time to reevaluate policies and undertake structural reforms that can deliver another period of strong growth, income convergence, and rising living standards. As Winston Churchill wisely noted, “An optimist sees the opportunity in every difficulty.”