As inflation has sunk in the euro area, talk of quantitative easing (QE)—and misgivings about it—have soared. Some think QE is not needed; others that it would not work; and yet others that it only creates asset bubbles and may even be “illegal.” In its latest report on the euro area, the IMF assesses recent policy action positively but adds that “… if inflation remains too low, the ECB should consider a substantial balance sheet expansion, including through asset purchases.” Given all the reservations, would the juice be worth the squeeze?

Q1. What is QE and how would it differ from other ECB balance sheet expansions?

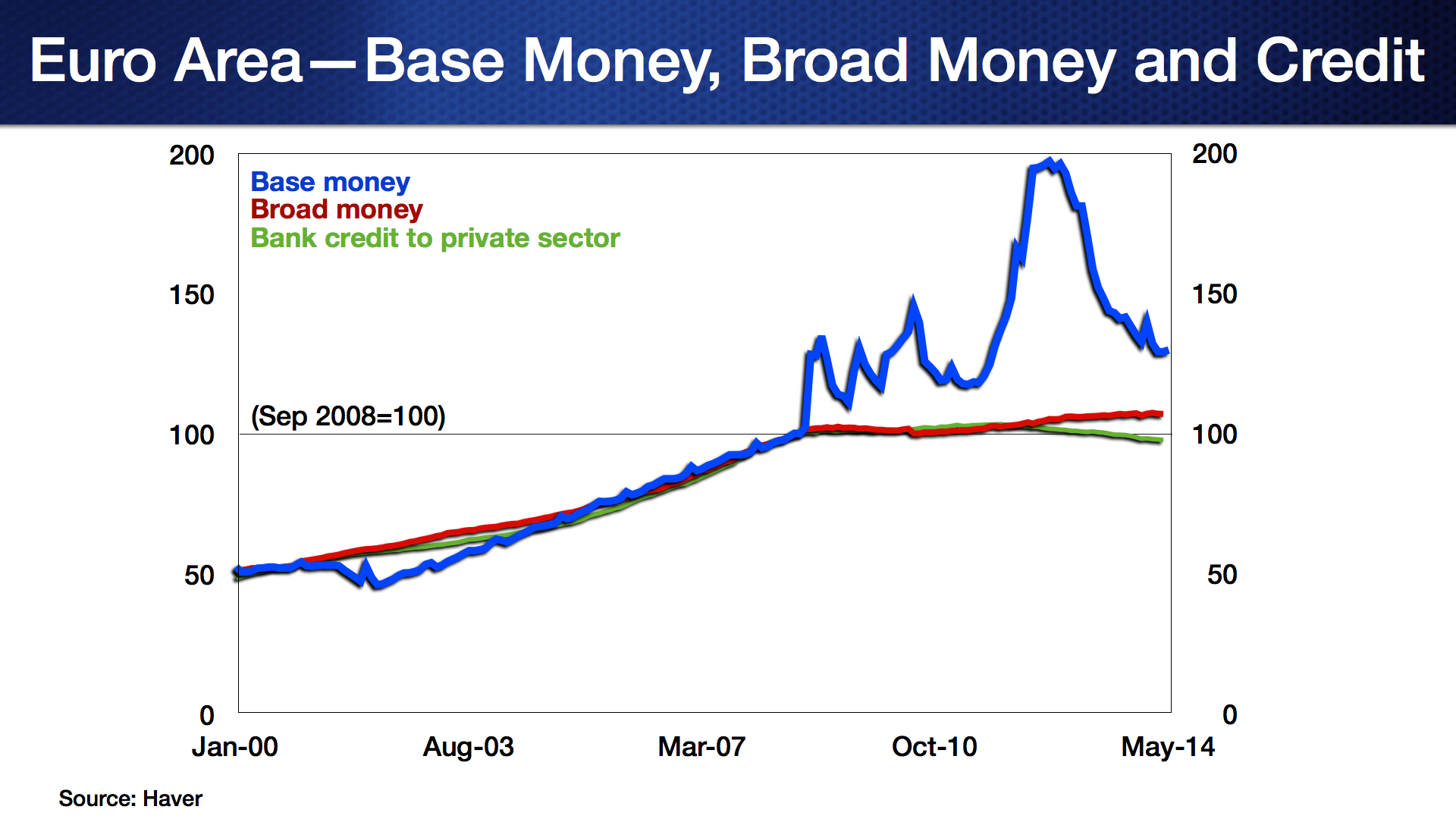

A1. QE at heart is a sustained expansion of a central bank’s balance sheet—something all major central banks have done since the onset of the crisis. Against a backdrop of reduced wholesale funding, the European Central Bank (ECB) launched 3-year Long Term Refinancing Operations (LTROs) in 2012, which significantly expanded reserve money as the ECB offered funding to banks against eligible collateral. The hope was that stable multi-year funding would encourage banks to restart lending and support activity.

While they did not vanish, concerns about stable funding and liquidity did ease—enough to prompt banks, eager to signal financial health, to start pre-paying LTROs. This undid much of the initial expansion in reserve money. Overall, LTROs prevented worse outcomes but did not actually lift private credit and broad money.

QE would differ from LTRO-type expansions in that the ECB would: (1) make outright purchases of longer-term assets (longer than 3 years), which have wider and larger effects on interest rates, asset prices and spending; (2) expand its balance sheet at its own discretion (not that of banks or others); and (3) sustain those purchases until inflation goals are met.

Q2. What assets would the ECB buy—public or private, core or periphery?

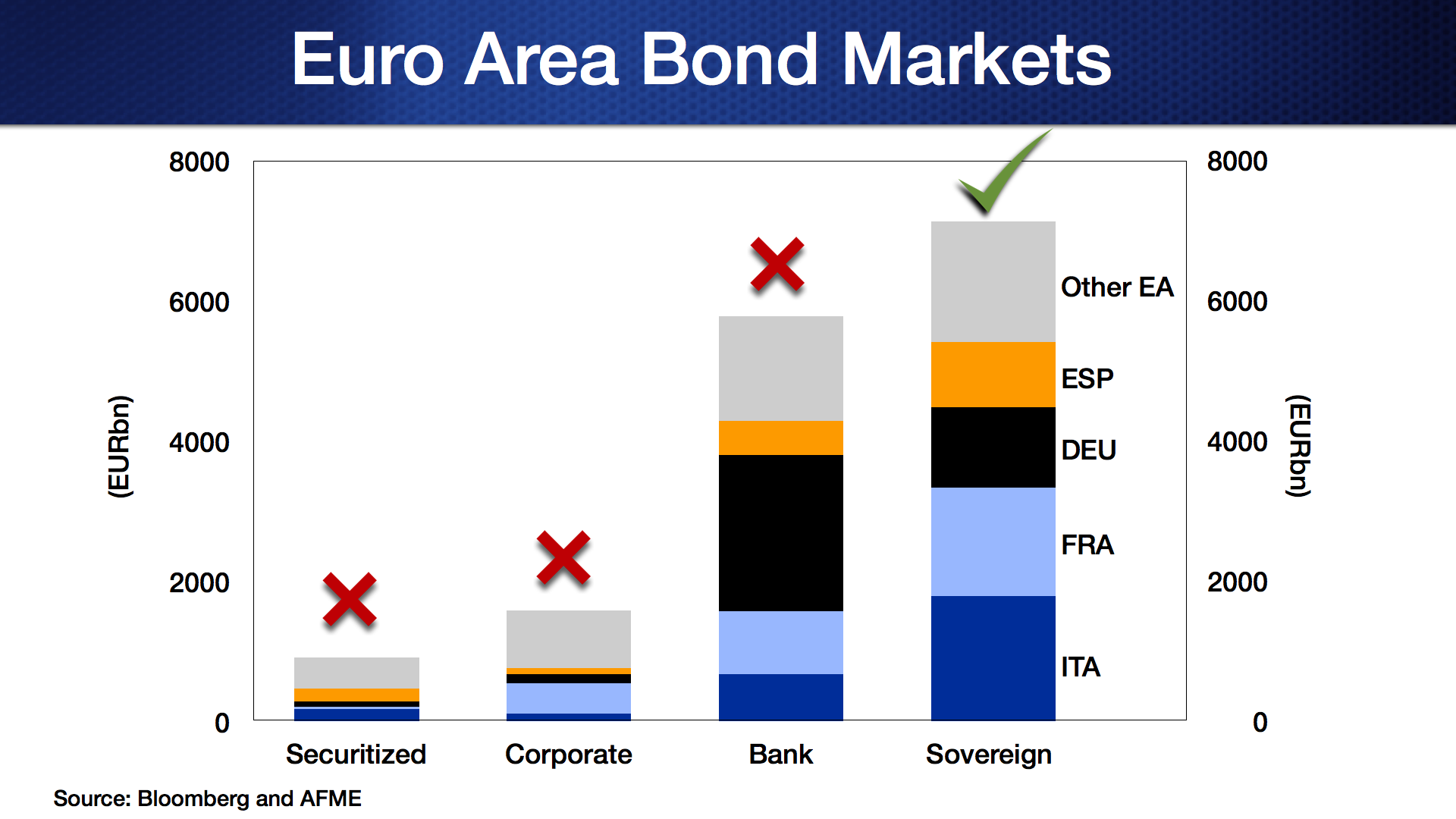

A2. For now, there are too few liquid private assets to sustain QE. The market for securitized bank assets is small, as is the one for corporate bonds. Bank bonds are plentiful and liquid but concentrated. Central banks rarely venture into equities. That leaves sovereign bonds the only viable option. (It would be desirable to further develop markets for securitized assets like mortgages and loans to small and medium-size enterprises; the mere fact of QE can give the needed impetus.)

ECB purchases should be across the board, not just core or periphery, because the problem of low inflation is across the board. So long as the ECB buys sovereign bonds in pursuit of its mandate and in a way that has nothing to do with fiscal outcomes (e.g., neutrally buying the bonds of all countries according to their share in ECB capital), it can rebut the oft-heard charge that QE violates the prohibition against “monetary financing of fiscal deficits.”

Q3. How would QE work?

A3. QE is not a panacea or substitute for reforms. But it can push up inflation by raising consumption and investment across the euro area, and support that trend by reviving the supply and demand for bank credit. How?

For starters, growth and inflation expectations would rise as the ECB signals resolve to achieve its inflation objective. The ECB’s Outright Monetary Transaction announcement has demonstrated the potency of whatever-it-takes signaling. Current demand and asset prices also would be lifted by the prospect of lower real interest rates (as QE reduces nominal interest rates and raises inflation expectations).

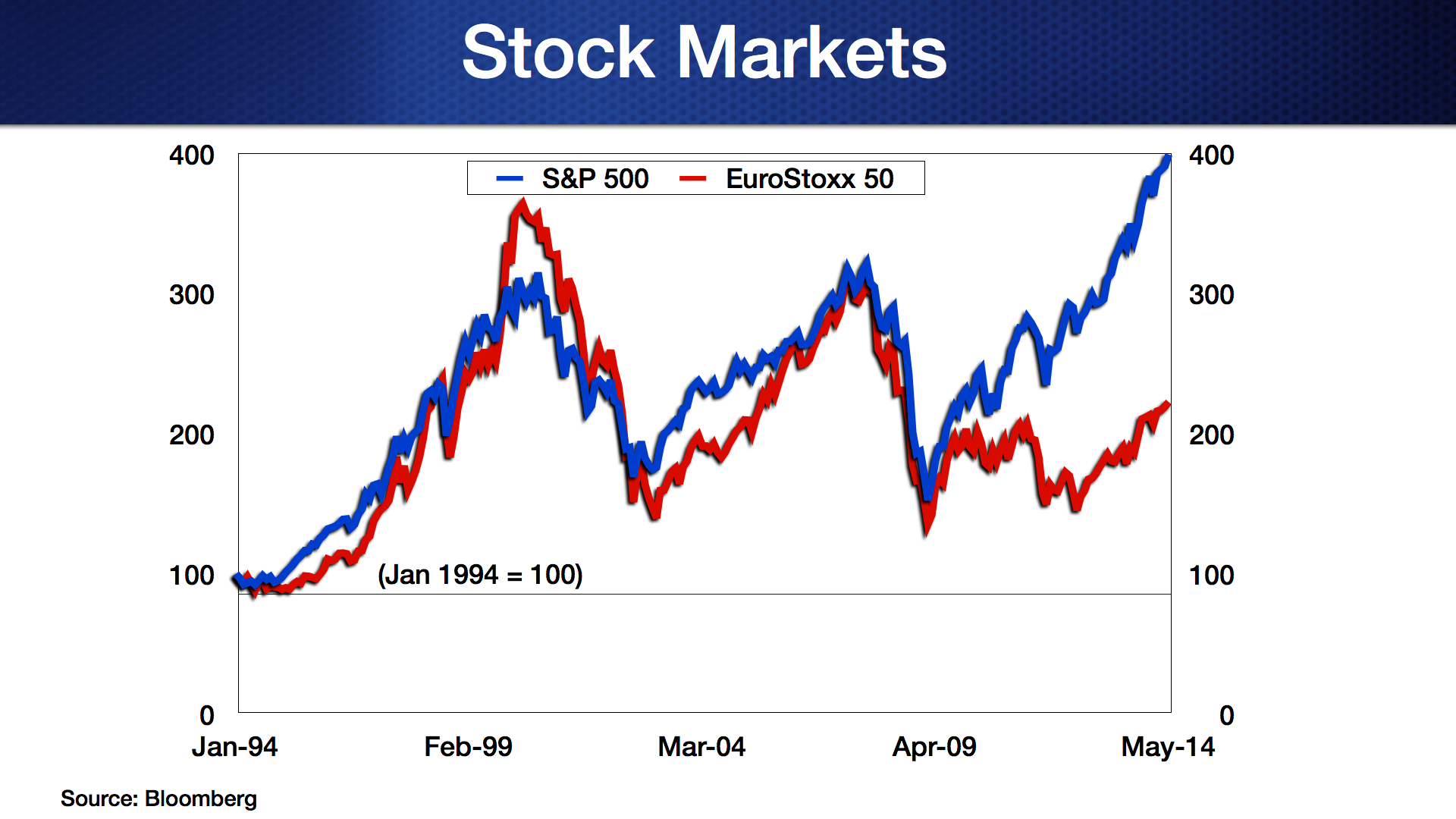

QE would also trigger important valuation effects. ECB sovereign bond purchases directly raise their prices. The sellers of sovereign bonds—banks, pension funds, asset managers—would need to reconstitute their portfolios with other long-term assets, over time raising asset prices more widely. European equity prices, for one, remain well below pre-crisis levels.

The significance of higher asset valuations would extend beyond the usual wealth effects:

Q4. Can QE be effective if interest rates are already low and the system bank-based?

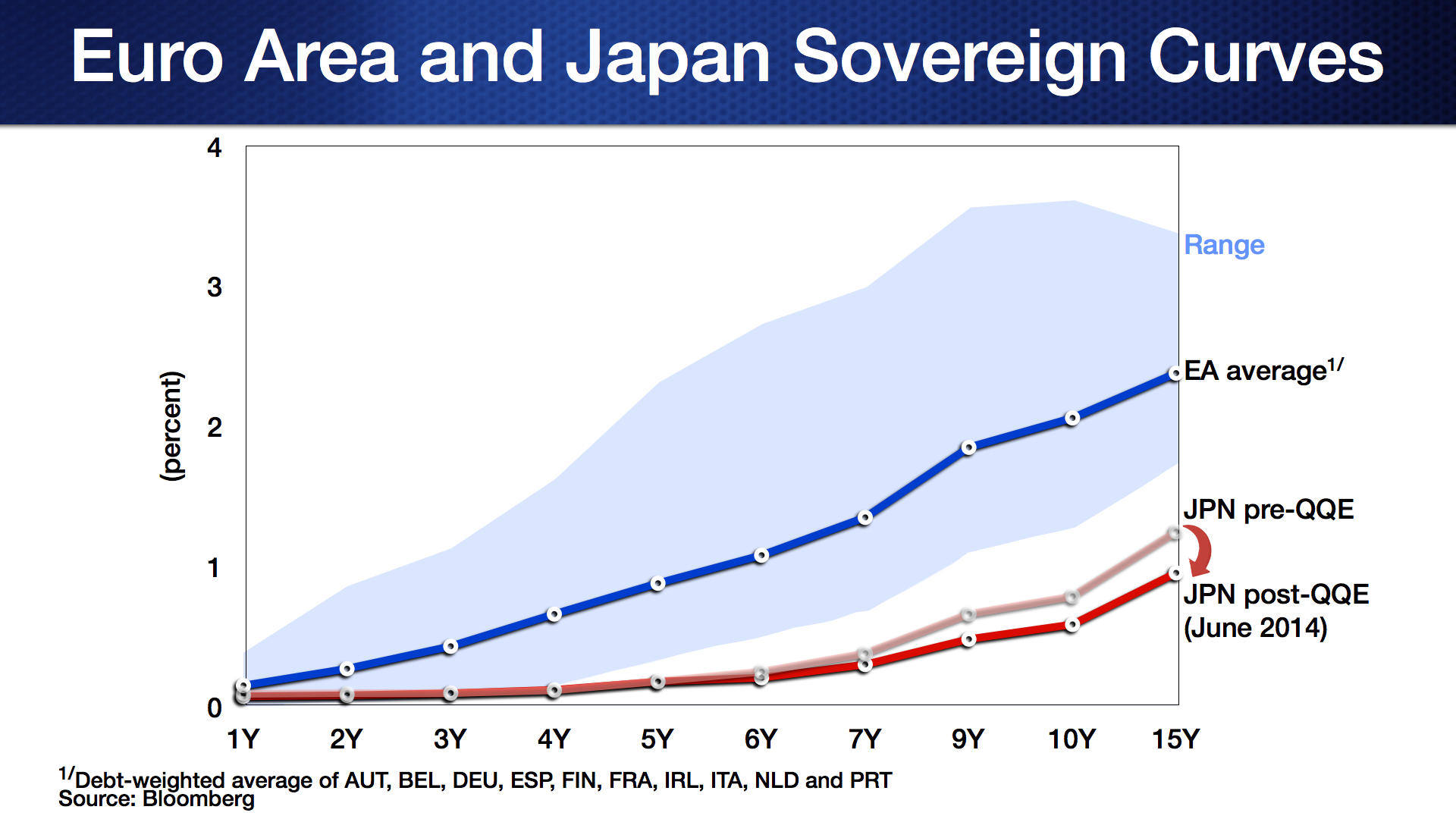

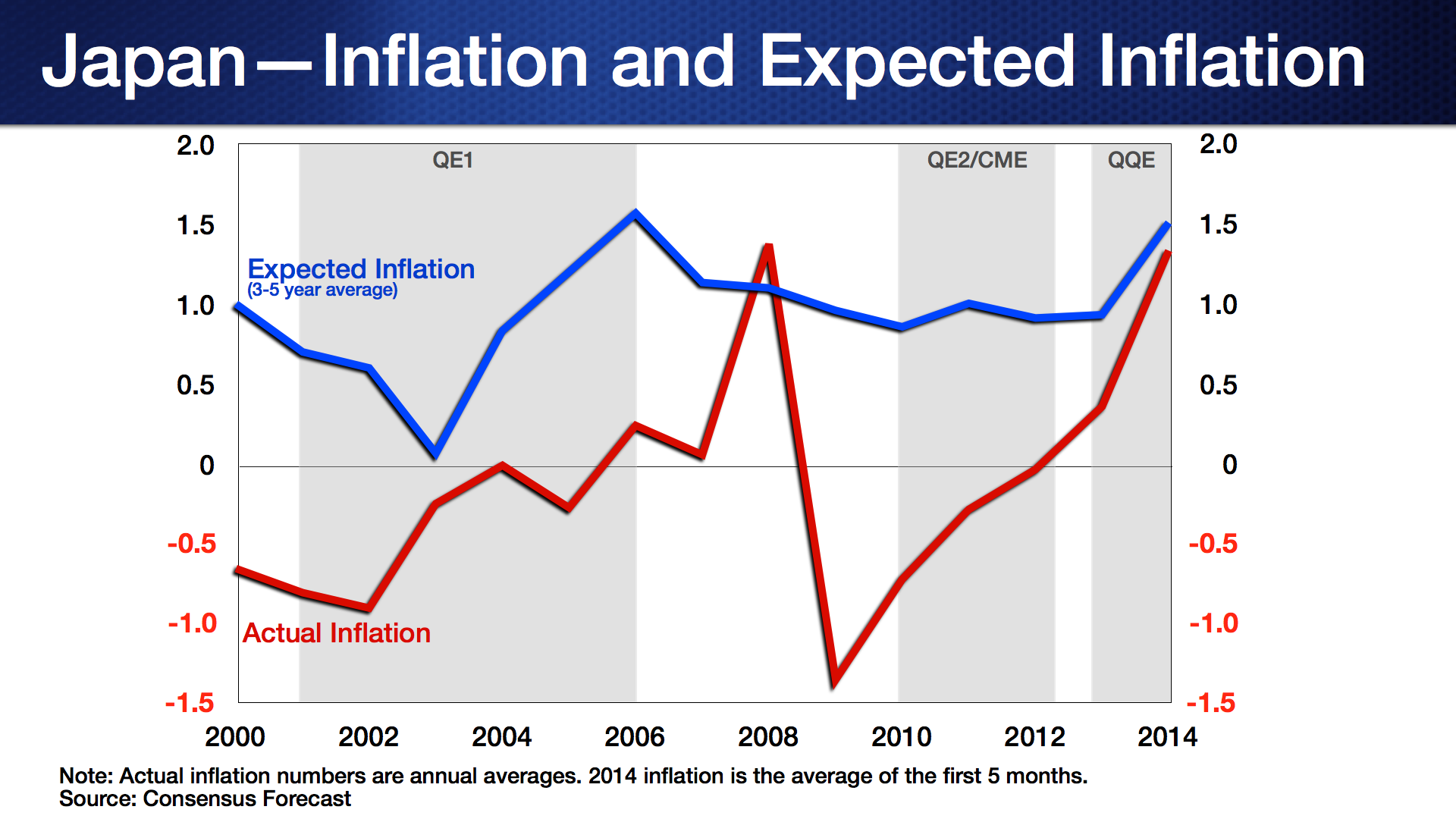

A4. As noted above, QE works via banks too. It worked in Japan even though Japanese finance is almost as bank-based as in Europe (83% and 89% respectively). And Japan had even lower interest rates when the Bank of Japan (BOJ) launched its successful qualitative and quantitative monetary easing (QQE) program last year. There is much more space for the yield curve to fall in Europe than there was in Japan. A decline in European yields of 50 basis points at mid-maturities, and more at the longer end, is entirely plausible.

Q5. So why did the ECB stop short of QE?

Q5. So why did the ECB stop short of QE?

A5. The ECB has been clear that it is open to unconventional measures but also that circumstances do not as yet justify QE. And indeed it would not help if the ECB went for QE with anything less than full conviction. The BOJ’s QE program in the early 2000s ended prematurely (before inflation and inflation expectations were durably raised), while that in 2010-12 was too guardedly implemented (in small steps and no clear link to the inflation goal). By contrast, its QQE since 2013 has been whatever-it-takes on size, pointed on goals and timeframe, and has yielded a strong response in inflation expectations.

Q6. What about side effects—asset bubbles and currency depreciation?

Q6. What about side effects—asset bubbles and currency depreciation?

A6. QE will push banks and others out of safe government bonds to lending to the rest of the economy. That is riskier but it is also the point. While risk-taking and credit growth may grow excessive, this is not an immediate risk, certainly not next to that of too low inflation. So far, credit is still contracting in the euro area (barely positive even in Germany) and there is no evidence of housing/asset bubbles (not even in Germany). If bubbles are blown, targeted macro-prudential measures, which need further development, can be deployed.

On the currency, QE would likely weaken the euro. Insofar as this raises demand and traded goods prices, it helps tackle the threat from low inflation. This could be an important channel. But depreciation is not inevitable: rising asset prices/economic prospects due to QE may draw capital and appreciate the euro.

With thanks to Petya Koeva Brooks, Pelin Berkmen and Ali Al-Eyd for their contribution to this blog post.