By

Evan Papageorgiou

When the U.S. Federal Reserve first mentioned in 2013 the prospect of a cutback in its bond buying program, markets had a “taper tantrum.” Many emerging markets saw large increases in volatility, even though outflows from their domestic markets were small and short-lived. Now the Fed has ended its bond buying and is looking ahead to rate hikes, and portfolio flows continue to arrive at the shores of emerging market economies. So everything’s fine, right? Not quite.

In our latest

Global Financial Stability Report, we show that the large concentration of advanced economy capital invested in emerging markets acts as a conduit of shocks from the former to the latter.

Emerging market economies can have financial stability problems even if they don’t have portfolio outflows. Declines in market liquidity

arising from changes in the structure of financial markets and volatility are policymakers and investors’ main rival.

Keep an eye on the ebb and flow of portfolio investment, and on the size as well

Despite retail portfolio outflows following 2013’s “taper tantrum,” total portfolio flows into emerging market bonds and equities have continued largely uninterrupted.

The allocation of

emerging market assets in the portfolios of developed market investors has increased by 2.5 times over the last decade—from 5% in 2002 to 13% in 2012.

Low interest rates in advanced economies have sent investors looking elsewhere for higher returns. And even though this increase in portfolio investment outpaced nominal GDP growth in emerging markets, what makes the risk systemic is the concentration of the $4.1 trillion of allocations in a few source economies and the concentration of allocations to the major recipient emerging market economies.

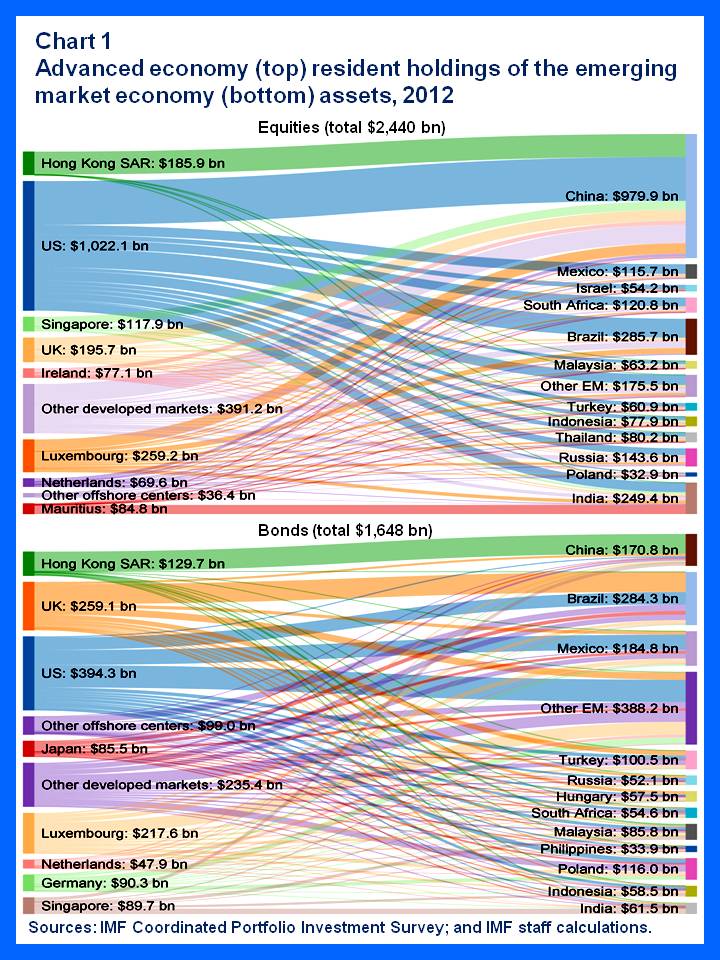

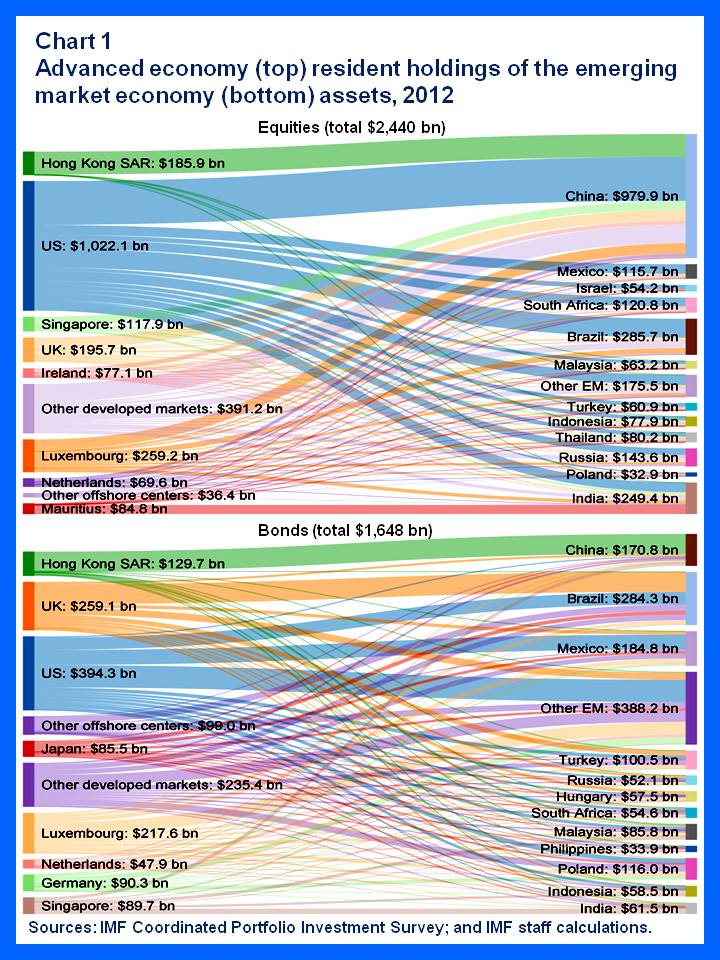

We found that 12 out of 190 emerging market economies receive 80% of all portfolio flows from advanced economies. And portfolio equity allocations from U.S. residents alone, account for more than a third of the total for each major emerging market economy (see Chart 1).

This is happening at the same time as other changes are taking place across financial markets, which can mean a decline in the price of emerging market assets and associated financial stability concerns.

Indeed, in our latest

Global Financial Stability Report we estimate the largest increases in volatility between the low (normal) and the high (risk averse) states to be for emerging market assets such as bonds, currencies, and equities in addition to high-yield bonds (see Chart 2 for bonds).

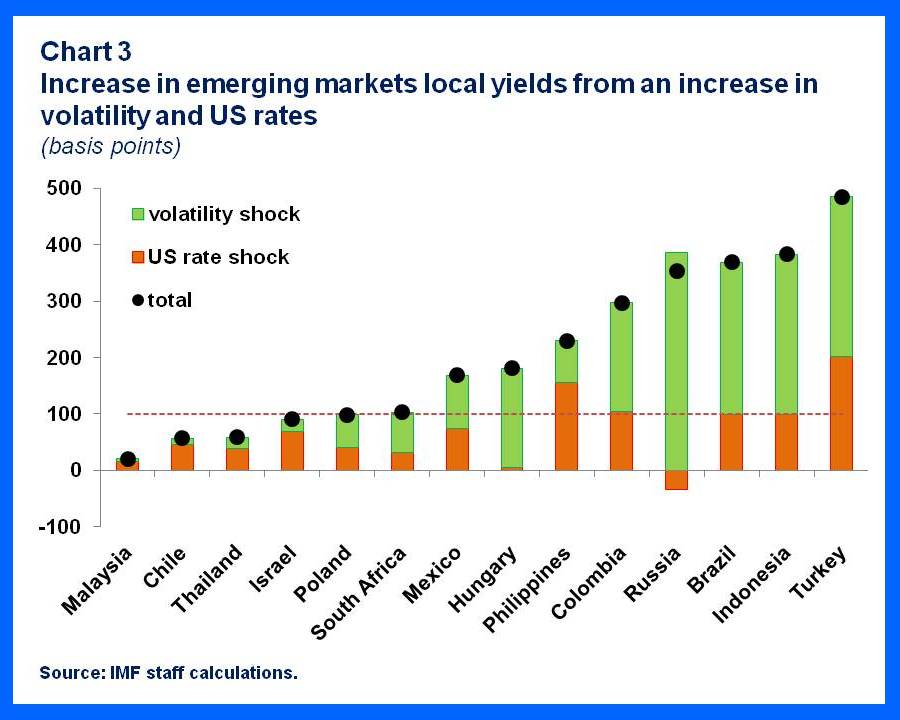

In fact, rather than interest rates, volatility may be the biggest worry for policymakers and emerging market investors, as the estimated sensitivity of emerging market local currency government bonds tends to be higher for a volatility shock than a commensurate U.S. interest rate shock across the major emerging market economies (Chart 3).

Policymakers need to recognize the latent risks arising from this synchronized relationship between advanced and emerging market economies financial systems, and put in place policies to ensure smooth market functioning and financial stability.

This is happening at the same time as other changes are taking place across financial markets, which can mean a decline in the price of emerging market assets and associated financial stability concerns.

Indeed, in our latest Global Financial Stability Report we estimate the largest increases in volatility between the low (normal) and the high (risk averse) states to be for emerging market assets such as bonds, currencies, and equities in addition to high-yield bonds (see Chart 2 for bonds).

This is happening at the same time as other changes are taking place across financial markets, which can mean a decline in the price of emerging market assets and associated financial stability concerns.

Indeed, in our latest Global Financial Stability Report we estimate the largest increases in volatility between the low (normal) and the high (risk averse) states to be for emerging market assets such as bonds, currencies, and equities in addition to high-yield bonds (see Chart 2 for bonds).

In fact, rather than interest rates, volatility may be the biggest worry for policymakers and emerging market investors, as the estimated sensitivity of emerging market local currency government bonds tends to be higher for a volatility shock than a commensurate U.S. interest rate shock across the major emerging market economies (Chart 3).

In fact, rather than interest rates, volatility may be the biggest worry for policymakers and emerging market investors, as the estimated sensitivity of emerging market local currency government bonds tends to be higher for a volatility shock than a commensurate U.S. interest rate shock across the major emerging market economies (Chart 3).

Policymakers need to recognize the latent risks arising from this synchronized relationship between advanced and emerging market economies financial systems, and put in place policies to ensure smooth market functioning and financial stability.

Policymakers need to recognize the latent risks arising from this synchronized relationship between advanced and emerging market economies financial systems, and put in place policies to ensure smooth market functioning and financial stability.