(version in Español and Português)

The turn of the year usually brings a fresh dose of optimism. Yet, worries dominate across much of Latin America and the Caribbean today, as 2015 marks yet another year of reduced growth expectations. Regional growth is projected at just 1¼ percent, about the same low rate as in 2014 and almost 1 percentage point below our previous forecast. Challenging external conditions are an important drag for many countries. Still, it’s not too late for some good New Year’s resolutions to address domestic weaknesses and improve growth prospects.

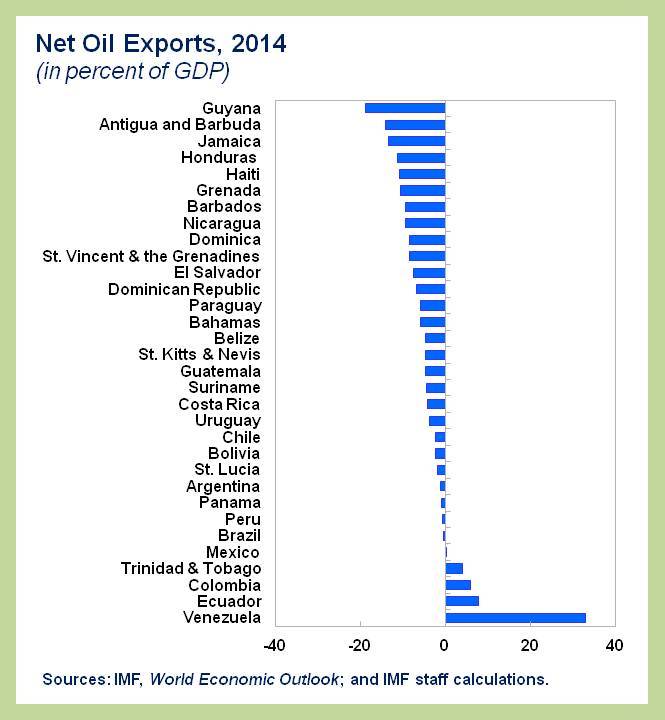

Winners and losers from cheaper oil

Commodity prices have continued to decline, reflecting unexpected demand weakness in several major economies, including China. The most notable mover recently has been oil, where increased supply has also played an important role in depressing prices.

In this environment, our forecast for global growth has come down again, and now stands at just 3½ percent for 2015. Prospects for U.S. growth have improved, but weaker dynamics in the euro area, China, and Japan are weighing down global activity.

The drop in oil prices is expected to be broadly neutral for Latin America and the Caribbean at large, but has very different effects across individual countries.

- Venezuela’s economy will take the largest hit, and is now forecast to contract by 7 percent in 2015. Indeed, each $10 decline in oil prices worsens Venezuela’s trade balance by 3½ percent of GDP, a bigger effect by far than for any other country in the region. The loss in export revenue causes mounting fiscal problems and a sharper economic downturn.

- To a more moderate extent, lower oil prices are also dampening growth prospects for Bolivia(whose large exports of natural gas are linked to oil prices), Colombia, and Ecuador. In all three countries, fiscal balances will suffer from falling oil revenue, but initial positions are strong enough to weather the impact. Mexico, in turn, has protected its 2015 oil revenue through financial hedging, and the petroleum sector plays a relatively modest role in the economy, so the overall impact is limited.

- The rest of the region should generally benefit from cheaper oil. The biggest beneficiaries are countries with high oil import bills, notably in Central America and the Caribbean. However, some caution is warranted, as several of these countries have been relying on subsidized oil deliveries from Venezuela under the Petrocaribe arrangement. With growing economic strains in Venezuela, its Petrocaribe support has started to diminish. For most recipients, the lower market price of oil should outweigh a potential loss of favorable financing terms from Venezuela, but some countries could face short-term cash flow pressures in the public sector.

Over the longer run, persistent weakness in oil prices would also limit the potential from developing untapped hydrocarbon resources in countries including Argentina, Brazil, and Mexico.

Dimmed prospects in South America

Even if lower oil prices, on balance, do not change the near-term regional outlook much, the story doesn’t stop there. South America, in particular, is facing stiff headwinds from disappointing global growth and the continued decline in the prices of metals and agricultural commodities. At the same time, it benefits little from the stronger U.S. recovery. As a consequence, exports are now expected to grow by only 1 percent on average this year.

The economic challenges facing South America are even more apparent from investment, which has slowed every single year since 2010 and is forecast to decline in 2015. Beyond the impact of worsening external conditions, a variety of domestic issues are also at play:

- A leading example is Brazil, where private sector confidence has remained stubbornly weak even after the election-related uncertainty dissipated. Economic activity is anemic, with output projected to expand only 0.3 percent this year. On the upside, the authorities’ renewed commitment to rein in the fiscal deficit and reduce inflation should help to shore up confidence in Brazil’s macroeconomic policy framework.

- Growth expectations in Chile and Peru are comparatively favorable but have also been pared back further since October. In Chile, uncertainty over the impact of policy reforms seems to be weighing on investment. In the case of Peru, weak exports and investment have driven a sharp recent slowdown, though concerted policy action and new mining operations are expected to support a significant rebound this year.

- Despite some easing of exchange rate pressures and a better-than-expected growth outturn in 2014, Argentina continues to struggle with large macroeconomic imbalances. We expect the economy to contract in 2015.

Brighter conditions up North

Mexico, in turn, is projected to grow by 3.2 percent this year—a solid prospect, though less than previously expected, as lingering sluggishness in domestic demand offsets the positive spillovers from stronger U.S. growth.

On the bright side, the outlook for Central America has improved as a result of lower oil prices and the robust U.S. recovery. Remittances grew 9 percent (year-on-year) in the first three quarters of 2014 and, together with stronger exports, will continue to underpin domestic activity. Similarly, the tourism-dependent economies of the Caribbean have started to see a long-awaited recovery in tourist arrivals.

Turning to policies…

Lower oil prices will alleviate external and fiscal vulnerabilities in some countries. They also provide a great opportunity to phase out costly and poorly targeted energy subsidies, which are common across the region.

In much of South America, meanwhile, the broad weakness of commodity prices has widened current account deficits further. Flexible exchange rates can help cushion this external shock. However, fiscal policy will also need to adjust to the reality that earlier forecasts for commodity revenue and output growth are no longer realistic.

Beyond such adjustments, the difficult current outlook underscores the urgency of supply-side reforms outlined in our recent Regional Economic Outlook reports. Boosting growth prospects and sustaining poverty reduction in a more challenging external environment will require determined efforts to improve the business environment, raise productivity, and increase saving and investment. It’s not too late yet for good New Year’s resolutions.