Versions in عربي (Arabic), Français (French), Русский (Russian), and Español (Spanish)

In November 2014, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain output despite a perceived global glut of oil. The result was a steep decline in price.

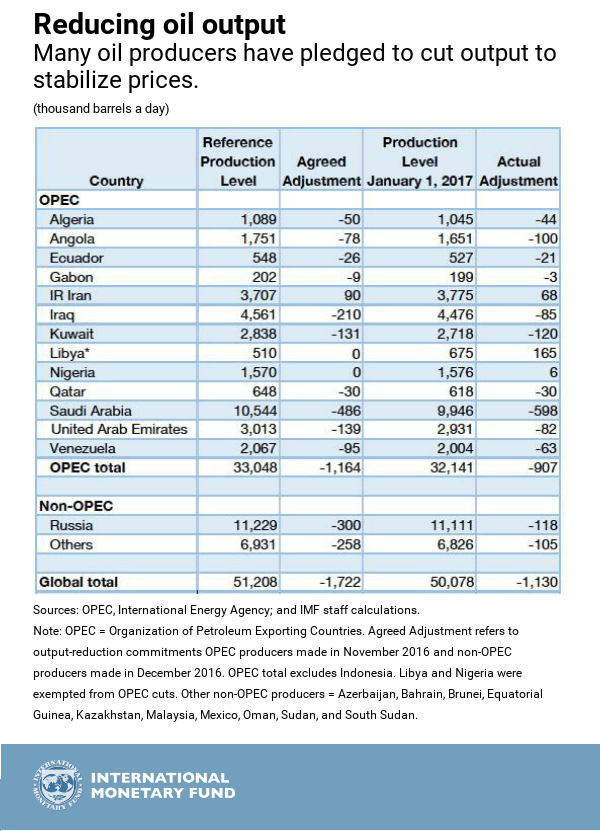

Two years later, on November 30, 2016, the organization took a different tack and committed to a six-month, 1.2 million barrel a day (3.5 percent) reduction in OPEC crude oil output to 32.5 million barrels per day, effective in January 2017. The result was a small price increase and some price stability.

But the respite may be temporary, because the price increase is likely to stimulate other oil production that can come on line quickly. A recent sharp decline in prices because of higher than expected oil inventories in the United States underlines the temporary nature of the respite the OPEC agreement provides.

The OPEC agreement

Saudi Arabia, Iraq, the United Arab Emirates, and Kuwait are bearing the brunt of the OPEC cuts, which could be extended another six months, while some member countries such as Nigeria and Libya have been exempted. Moreover, non-OPEC producers joined in and agreed to cut about 600,000 barrels a day. Russia committed to cut 300,000 barrels, and 10 other non-OPEC oil producing countries agreed to cut the remaining 300,00 barrels a day.

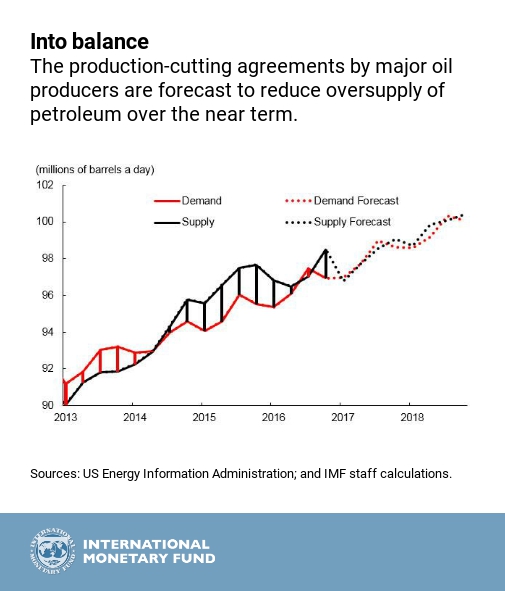

These agreements appear to have brought supply and demand into balance at a price just above $50 a barrel—largely because of the high degree of compliance by OPEC members with the level of production agreed to last November. OPEC reported that compliance was close to 90 percent in January—a level that would be in sharp contrast with the typically low adherence by OPEC members to those set in earlier production agreements. There are some reports that compliance is lower, but Saudi Arabia has signaled it will do whatever it takes to enhance the credibility of the agreement and has cut its production more than required.

That said, there are several threats to the effectiveness of the agreement, even in the short term. Some OPEC members—Iraq, Libya, and Nigeria—have increased their production since October. Furthermore, not only did non-OPEC producers make smaller reductions than OPEC, they also do not have to reach their production targets as soon. For example, Russia has so far cut only 120,000 of the 300,000 barrels a day it promised. And some analysts believe that some of the targeted reductions are phantom, reflecting a natural decline from historically high production levels rather than active cuts.

Shale oil threat

But perhaps the biggest threat to the attempt to achieve price stability comes from shale oil producers. The $6-a-barrel increase in spot oil prices that followed the hints last September of an OPEC production agreement is expected to stimulate investment in oil production in 2017, after significant declines in the previous two years. An increase in shale oil output in the United States could quickly offset much or all of the OPEC and non-OPEC production cuts, because shale wells can begin production within a year of the initial investment, unlike conventional oil investments, which take a number of years to come to fruition.

The shale effect has happened before. In early 2014, even though excess supply was building up, oil prices remained at around $100 a barrel because market participants expected OPEC to cut production to support prices—creating a floor price that stimulated non-OPEC production of not only shale oil, but oil from relatively high-cost sources as well. The floor price did not last long because oversupply built up—and oil prices began to fall, precipitously after the OPEC meeting in November 2014.

Despite OPEC’s greater ability to sustain the recent production agreement, a somewhat similar sequence of events is likely to occur now because of shale oil’s fast responsiveness to price changes. US shale oil investment declined very sharply following the drop in oil prices that started in 2014 and within a few months, production declined. The oil price rebound in 2016 helped boost investment, which was further enhanced by the announcement in September 2016 in Algeria that OPEC intended to cut production levels. By February 2017, US oil investment, as measured by the number of drilling rigs in operation, reached its highest level since November 2015.

Moreover, the shale oil threat is greater because producers in the United States have become more efficient thanks to improved operations and increased selectivity in the wells they exploit. Although the ultimate capacity of shale oil production is uncertain, its behavior is now a central feature of the new oil market and will help lead to more limited and shorter production and price cycles.

Bottom line

The OPEC agreement has hastened the rebalancing of the oil market—that is, when the supply of oil is in line with demand and accompanied by stable prices. The OPEC production agreement should reduce excess supply—at least temporarily. But the futures market in oil prices suggests that expectations are firmly anchored at around $50 a barrel. The forces unleashed by the OPEC agreement will limit its effectiveness over the next few years.