The 2008 global financial crisis and its aftermath have tested the European Union’s (EU) fiscal governance framework—the rules, regulations, and procedures that influence how budgetary policy is planned, approved, carried out, and monitored. Given the distinctive nature of EU integration, the framework aims to discipline national fiscal policies to prevent adverse spillovers to other countries and distortions to the conduct of the euro area’s common monetary policy.

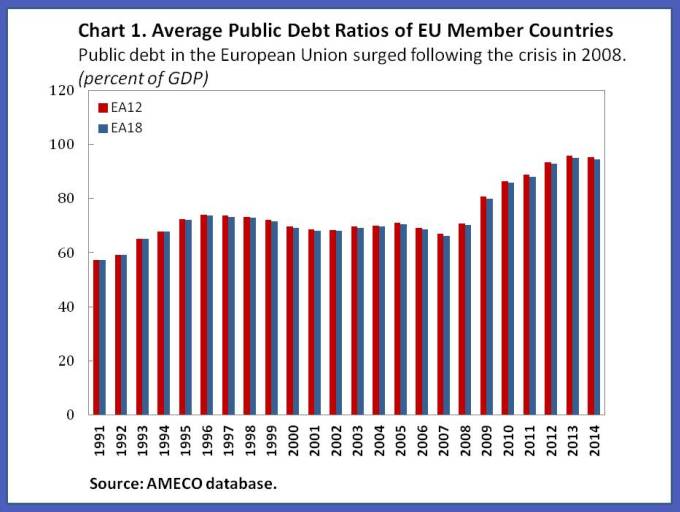

The build-up of fiscal imbalances, however, revealed gaps in the framework. Public debt in the European Union soared following the crisis in 2008 to an average of around 95 percent in 2014—almost 30 percentage points above its average pre-crisis level (Chart 1).

Rooted in the EU treaties and the 1997 Stability and Growth Pact (SGP), successive reforms to the fiscal framework—including the 2005 reforms, the 2011 Six Pack, the 2012 Fiscal Compact, and the 2013 Two Pack—have brought many positive elements, including a stronger economic underpinning to the rules-based system, better alignment of fiscal targets with debt objectives, and improved coordination and conduct of fiscal policy.

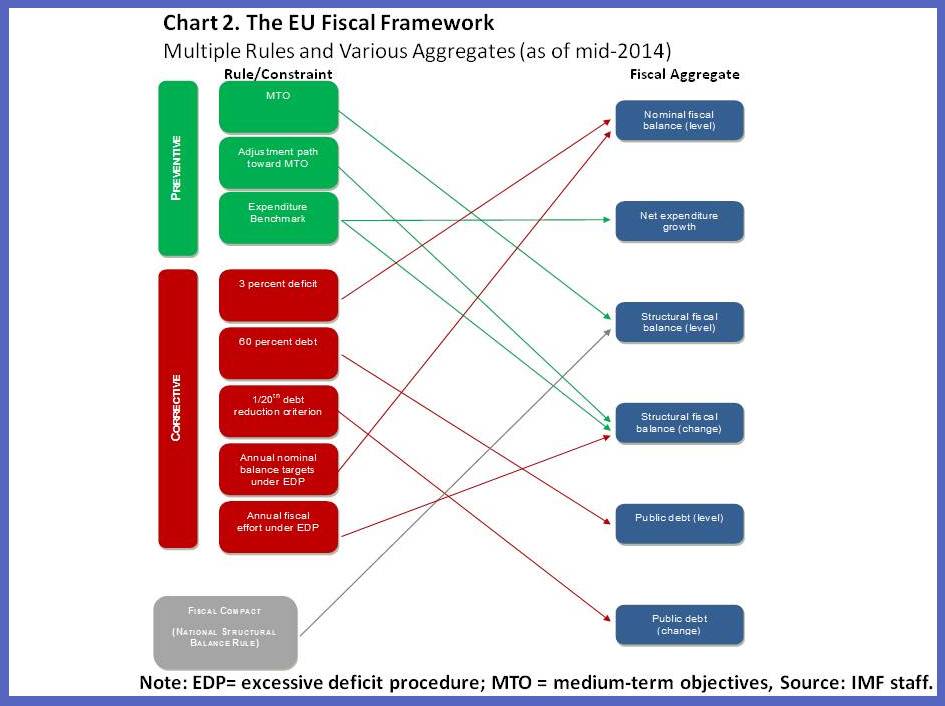

But they have also increased its complexity. The current framework involves multiple intricate rules that hamper effective monitoring and public communication (Chart 2). Compliance with the framework could also be improved.

In our new paper, we discuss medium-term reform options to simplify the framework and enhance compliance.

A single fiscal anchor and a single operational rule

The dual objectives of safeguarding fiscal sustainability and maintaining simplicity suggest a two-pillar approach to the design of the fiscal framework, with a single fiscal anchor and a single operational rule that acts as the lever that moves the anchor.

- Debt as the anchor. The ultimate objective of the fiscal governance framework should be to ensure fiscal sustainability in the form of public debt sustainability. Public debt-to-GDP ratio is considered a natural anchor for capturing repeated (cumulative) fiscal slippages that flow variables, like the budget deficit, would not capture. While public debt can be affected by factors other than fiscal actions, like financing operations that are unrelated to budget deficits (like financial sector bailouts or valuation effects), there is no good alternative to using the public debt-to-GDP ratio as the fiscal anchor.

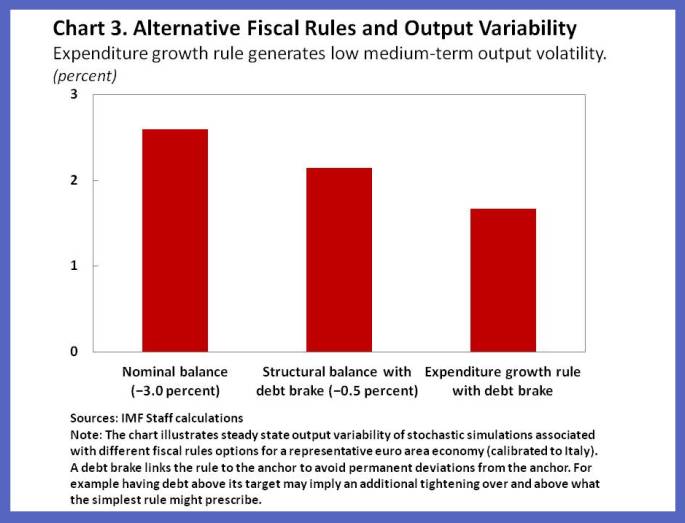

- An expenditure growth rule as the operational rule. A good operational rule should support countercyclical fiscal policy (economic stabilization) and provide a strong link to the fiscal anchor. Moreover, the rule should provide operational guidance (by being under the control of policymakers and having a direct link to discretionary budgetary measures) and be transparent (that is, easy to communicate to the public). An expenditure growth rule (possibly with an explicit debt correction mechanism or debt brake) as the operational rule linked to the anchor does a good job of satisfying these requirements. It generates low medium-term variability of output (Chart 3), has a clear link to budgetary actions (by constraining real expenditures), and is more straightforward to communicate.

Improving compliance

Beyond such simplification, additional reforms could help improve implementation of the fiscal framework and support compliance. The preventive and corrective arms of the Stability and Growth Pact could be merged or at the least, the rules in the two arms could be more harmonized. Making the gradual step-up of monitoring and constraints more automatic could improve enforcement. Corrective actions and sanctions could also be formulated to better reflect economic realities (monetary fines in a downturn are not credible).

The transition towards a reformed fiscal framework would take time. Some reforms may face legal obstacles, and in some cases, wholesale treaty changes may be needed. However, working for a simpler and more robust fiscal framework may be the best response to recent skepticism about the European project.