Dealing with problem banks in a prompt, efficient, and even-handed manner is essential for the European banking union. Much progress has been made, but more needs to be done to strengthen both institutions and practices. We outline the recommendations in this area proposed as part of the IMF’s recent assessment of the euro area financial sector.

Having in place a sound framework and the operational capacity to handle problem banks is critical to “leveling the playing field” in the banking union and to reducing risks. A truly common system is needed to ensure that banks compete on their own merits and are not advantaged or disadvantaged by the jurisdiction where they incorporate. Good supervision—as we’ve seen under the Single Supervisory Mechanism—may reduce the probability of a bank failing abruptly. Yet from time to time banks do fail, so the crisis preparedness and management system needs to be ready to address what might otherwise be costly episodes for governments and economies alike.

Evolving sector

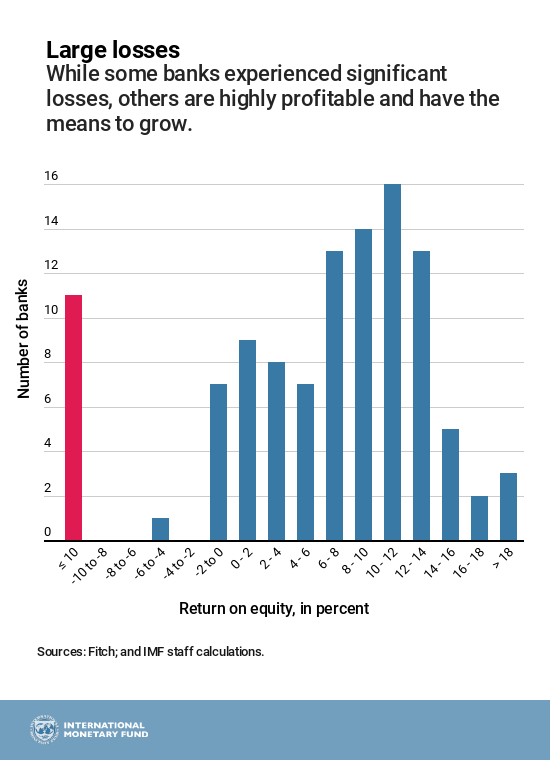

The euro area banking sector constantly evolves, and more consolidation can be expected. In our report, we show that a subset of banks display chronically low profitability, even in good times. In 2016, for example, roughly one in 10 large banks posted very large losses. The weak performers are under pressure to restructure, merge, downsize, or exit—pressure that can only grow with advancing digitalization and competition from nonbanks. Hence, there is going to be a need for a bank recovery and resolution framework that helps make this process as smooth as possible.

Action needed

The Bank Recovery and Resolution Directive and the Single Resolution Mechanism Regulation provide a solid foundation to deal with problem banks. But the framework remains fragmented and contains incentives for member states to resort to national solutions. Therefore, the banking union needs to focus on 5 main areas to be adequately prepared:

- The legal regime for early intervention and the ability to make early preparations should be strengthened. Relevant agencies need to be able to pre-schedule when a problem bank is intervened and resolved.

- Financial support must be in place for an intervened bank, so it does not suffer a fire sale or the collapse of essential services. A newly resolved bank needs to be able to count on adequate liquidity buffers. Fear of a collapse may spread uncertainty and even paralyze decision making. In the near term, the euro area needs:

- A well-funded resolution fund, with a backstop;

- Well-funded national deposit insurance systems;

- The establishment of the European Deposit Insurance Scheme to underpin national deposit insurance systems;

- Building up of loss-absorbing capacity in banks (so-called Minimum Requirement for Own Funds and Eligible Liabilities, or MREL), so that each bank has enough equity and subordinated debt that can credibly be bailed in. Having sufficient “internal” MREL prepositioned in material subsidiaries of cross-border groups will reduce potential conflicts among national interests.

- Banking resolution must be undertaken in a coherent framework. The triggers for action (e.g., what counts as the “public interest”) need to be streamlined, and the hierarchy of creditor claims in bank insolvency need to be more consistent across countries.

- More is needed in times of widespread crisis, when the risk of contagion is strong. Too strict rules—particularly the bail-in requirement—may lead to increased uncertainty and flight from potentially endangered banks.

- The Single Resolution Board itself should be able to appoint a liquidator and initiate proceedings. This ability would be especially useful in dealing with larger and cross-border banks that do not merit full-scale resolution.

Nobody likes a bank failure, but the banking union authorities would be well advised to step up preparations for what, sooner or later, is almost inevitable.