The global spread of the coronavirus is a human tragedy unfolding across the world. Quantifying the economic impact is complex, giving rise to significant uncertainty about the economic outlook and the associated downside risks. Such an abrupt rise in uncertainty can put both economic growth and financial stability at risk. In addition to targeted economic policies and fiscal measures, the right monetary and financial stability policies will be vital to help buttress the global economy.

Global cooperation to synchronize monetary policy must be high on the agenda.

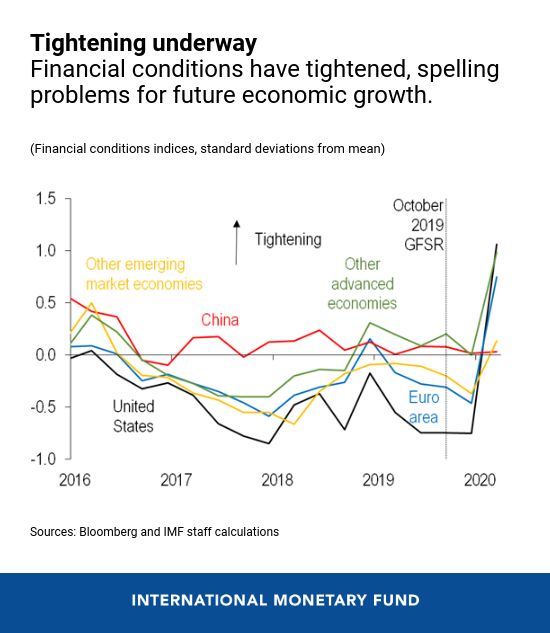

Higher uncertainty and tighter financial conditions

Measures of economic uncertainty such as equity market volatility increased sharply in countries around the world. Stock markets in major economies, such as the United States, the Euro area, and Japan, all fell sharply and witnessed a surge in implied volatility as skittish investors tried to factor in the latest risks posed by the new virus.

As a result of this sharp increase of uncertainty, credit spreads have widened broadly across markets as investors are reallocating from relatively risky to safer assets. High-yield and emerging-market bonds are hit particularly hard by these reallocations. As a result, the spreads of emerging- and frontier-market bonds denominated in U.S. dollars have widened sharply.

Financial conditions have tightened significantly in recent weeks, which means that companies are facing higher funding costs when they tap equity and bond markets. Such a sudden, sharp tightening in financial conditions acts as a drag on the economy, because firms postpone investment decisions and because individuals delay consumption as they feel less financially secure.

Monetary policy response

The sharp tightening in financial conditions, along with expectations of low inflation, means that monetary policy has a role to play at the current juncture. Central banks can act quickly to help ease the tightening of financial conditions by injecting liquidity and cutting interest rates, thus preventing a possible credit crunch. In fact, markets have been anticipating aggressive easing by central banks, as reflected in the sharp fall in sovereign bond yields in many countries around the world.

Synchronized actions across countries increase the power of monetary policy. Therefore, global cooperation to synchronize monetary policy must be high on the agenda. Ample liquidity within countries, and across borders, is the prerequisite to the successful reversal of the rapid tightening in financial conditions. In these unusual circumstances, if liquidity pressures threaten market functioning, central banks may need to step in and provide emergency liquidity.

If economic and financial conditions were to deteriorate further, policymakers could revert to the broader toolkit that was developed during the financial crisis. For example, the Federal Reserve launched the Term Asset-Backed Securities Loan Facility in 2009, which provided targeted funding. The Bank of England and U.K. Treasury introduced the Funding for Lending Scheme, where a funding subsidy was provided to incentivize the expansion of lending to households, small and mid-sized enterprises and non-financial corporates. Other authorities, too, have deployed variants of such lending schemes that aim at lowering the costs of borrowing in certain sectors.

Financial stability policies

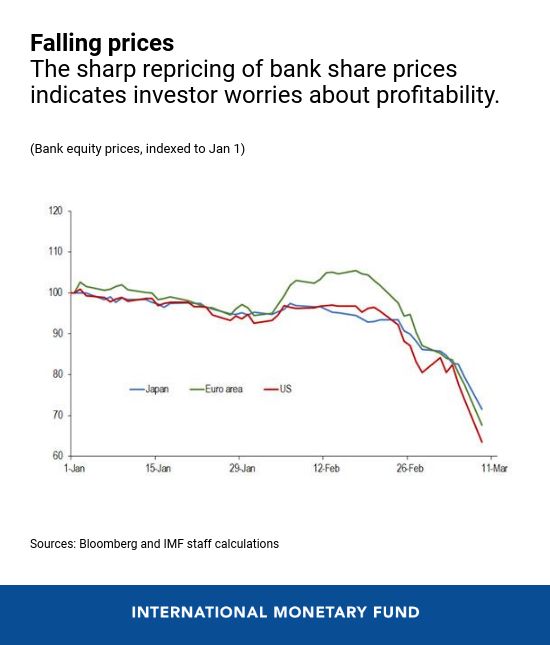

The sharp decline in interest rates, combined with growing anxiety about the economic outlook, have also raised investor concerns about the health of banks. Banks’ share prices have fallen sharply, and bond prices of banks have also come under some pressure—likely reflecting fear of potential losses.

The good news is that banks are generally more resilient than before the 2008 financial crisis, because they have greater capital and liquidity cushions. This means the risks to financial stability stemming from the banking sector are much lower, despite declining share prices.

Supervisory authorities should, however, monitor developments at banks very closely. Given the temporary nature of the virus outbreak, banks could consider a temporary restructuring of loan terms for the most-affected borrowers. Supervisors should work closely with banks to ensure that such actions are both transparent and temporary. The goal must be to preserve banks’ financial strength and overall transparency across the financial sector.

Authorities should also be alert to possible financial stability threats from outside the banking system. This requires an increased focus on asset managers and exchange-traded funds, where investors might liquidate risky investments suddenly.

Large swings in asset prices can quickly put markets and institutions under pressure. While market functioning has been able to withstand large swings in asset prices so far, anecdotal evidence suggests that liquidity has been tightening in many markets. And there are strains in U.S. dollar funding markets, where non-U.S. banks and corporates borrow in U.S. dollars.

Overall, policymakers must act decisively and cooperate at the global level to preserve monetary and financial stability during this time of extraordinary challenges. The mantra of “hoping for the best, preparing for the worst” has long been successfully deployed. The IMF will act as needed to help its members face this extraordinary, but hopefully temporary, crisis.