The Sydney Opera resumed live performances and the city of Melbourne recently hosted the Australian Open tennis tournament with fans (mostly) in attendance. Japan is back to planning the delayed 2020 Summer Olympics, while China focuses on the Beijing 2022 Winter Games. Having been hit by COVID-19 first, Asia is also recovering first. At the pandemic’s first anniversary, is the region back to full health?

Asia must remain agile and innovative to exit the crisis in a durable, greener, and more equitable way.

The best answer is that it is too early to know for sure. The pandemic exacerbated existing long-term issues: slowing productivity growth, growing indebtedness, aging population, rising inequality, and managing climate change. A new IMF staff paper looks into how the region can navigate these multiple challenges.

Long-lasting effects

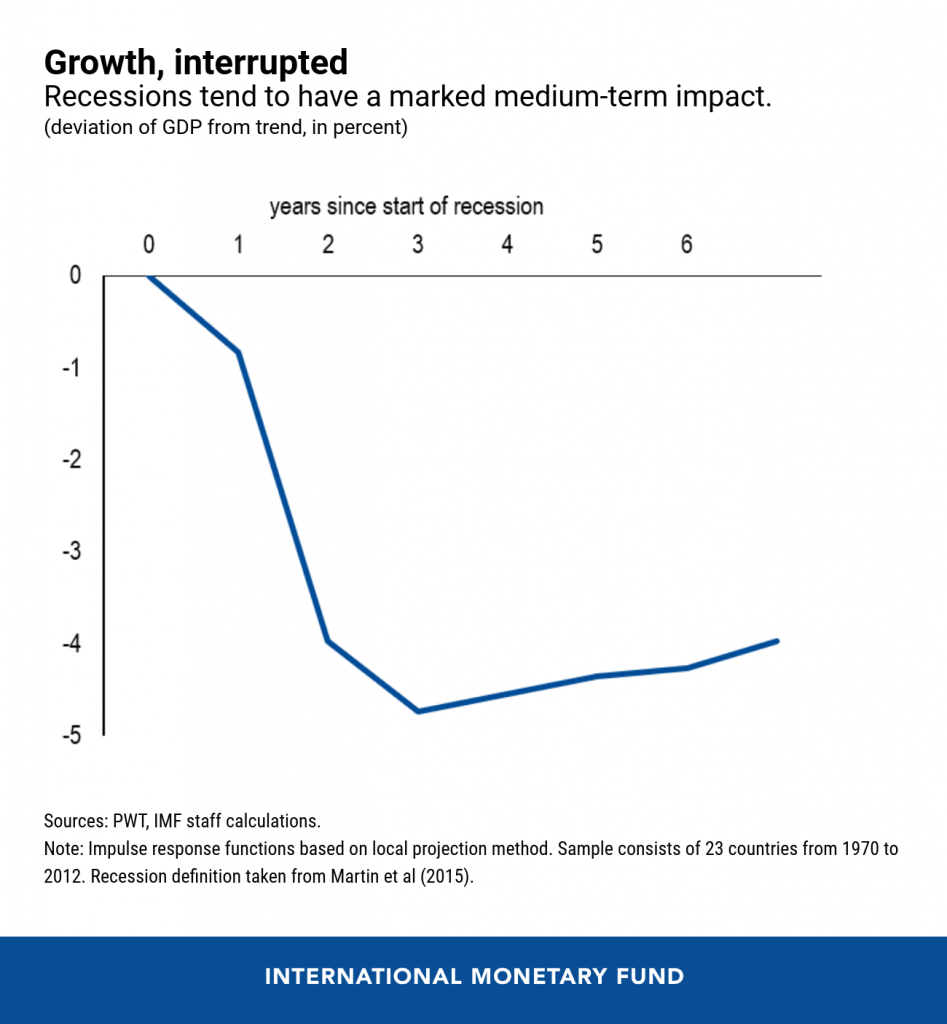

If past experience is any guide, this pandemic will have long-lasting effects. A look at past recessions in advanced economies reveals that on average, five years after the start of a recession, output is still almost 5 percent below its precrisis trend and unlikely to ever catch up.

The COVID-19 pandemic has been a perfect storm, destroying jobs, worsening poverty and inequality, and creating a public and private debt problem—especially for countries and firms already in fragile financial health beforehand. This unprecedented economic disruption has the potential to leave lasting scars for years to come, arising from persistent declines in the capital stock, employment, and productivity.

Asia’s labor markets suffered, with unemployment surging, labor force participation plunging, and job losses concentrated in industries with lower wages and among women and youth. The poorest and most vulnerable were disproportionately hit, exposing severe gaps in social protection and exacerbating already high inequality in advanced and emerging Asia.

Public and private debt hangover

In the pandemic’s aftermath, many countries will have to contend with high public and private debt burdens—possibly too large for some to manage. Sovereign debt is an issue in small states. Tackling this issue will require extra focus on revenue mobilization, public finances, and debt management, with support from multilateral partners and debt relief providing some breathing space.

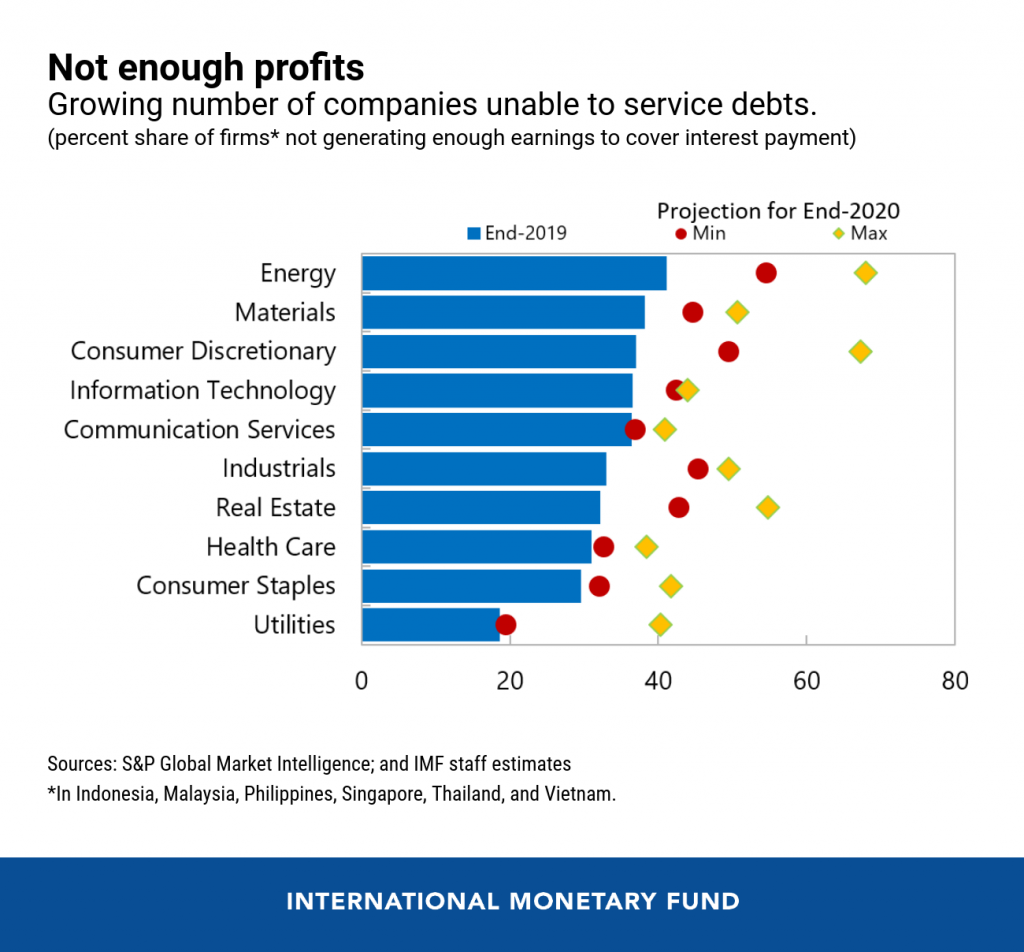

In larger emerging markets, the main problem might be record-high private debt. More and more companies are not generating enough earnings to service their debts. Government support is helping them to keep afloat, but a large wave of corporate bankruptcies could follow when that support is withdrawn, and in the absence of other interventions. This vulnerability can be especially acute in Asia, if global financial market conditions tighten in the process of recovery, leading to capital outflows and additional pressure on the corporate sector.

To address this vulnerability, countries would need to reinforce private debt resolution frameworks, ensure the availability of adequate financing, and facilitate access to risk capital to speed up the reallocation of resources towards growing sectors.

Measures for unconventional times

Most countries provided significant fiscal and monetary policy support to cushion the blow. Many—especially emerging and developing economies—are resorting more to unconventional monetary policies to ease the pressure on banks and borrowers.

India, Sri Lanka and Nepal announced debt service moratoria and targeted lending schemes to provide relief to households and firms. Financial regulation requirements related to capital and liquidity coverage were loosened. Malaysia and Thailand provided extra liquidity to firms through central bank lending operations, while Indonesia and the Philippines used large-scale asset purchases.

While warranted, these more aggressive policies inevitably entail risks, which will increase the longer they are used. Policymakers would be wise to focus on minimizing distortions and developing clear exit strategies for the unconventional measures adopted.

Healing the scars

To prevent longer-term economic “scarring,” Asia needs to expedite economic reforms to boost productivity growth and investment, allow for adequate reallocation of resources across sectors, and support workers affected by the transition. The package could include well-targeted hiring subsidies and worker retraining schemes; infrastructure upgrades; simplifying business processes; and reducing the regulatory and tax burden.

These actions need to be combined with a broader push for upgrading social safety nets to bring workers into formal systems, while supporting the vulnerable with targeted conditional cash transfers.

Greener future

Paradoxically, the COVID-19 shock also provided a glimpse of what a better future could hold for Asia. The temporary re-allocation from energy-intensive sectors, such as airlines and transportation, provides an opportunity for job creation in more productive and cleaner sectors. A well-designed carbon tax package and complementary product and labor market policies could support capital re-allocation and labor reskilling.

This would benefit the global fight against climate change, as Asia-Pacific has some of the largest carbon dioxide emitters and polluters, and could lead to improved health conditions for local populations, better jobs, and more resources to meet developmental needs.

Reforms in healthcare, social safety nets, labor markets, and the corporate sector will help to mitigate the pandemic’s effects and to address the pre-existing longer-term issues the region faces. Asia must remain agile and innovative to exit the crisis in a durable, greener, and more equitable way.