Credit IMF

Credit IMF

The world confronts the weakest medium-term growth outlook in three decades amid high debt levels, fragmented trade, and the prospect of higher-for-longer interest rates. In this environment, the IMF is redoubling its efforts to promote stability and growth.

All countries grapple with uncertainty from shocks related to the pandemic, war in Ukraine, and transformational challenges such as climate change and digitalization. Several emerging market and developing countries have shown remarkable resilience. But many—especially low-income countries—are increasingly vulnerable amid tighter financial conditions, limited policy room for maneuver, and dwindling buffers.

These countries also face a funding squeeze, heightened food insecurity, and a slower convergence toward higher living standards. High debt burdens and a sharp increase in debt servicing costs—exceeding 40 percent of revenues in several highly indebted countries—leave little space for social spending and growth-enhancing investment. This adversely impacts debt sustainability and social stability.

The IMF is responding to calls to play an even greater role to support our member countries during these very challenging times, importantly through the provision of balance of payments financing and policy advice.

Crises and channeling

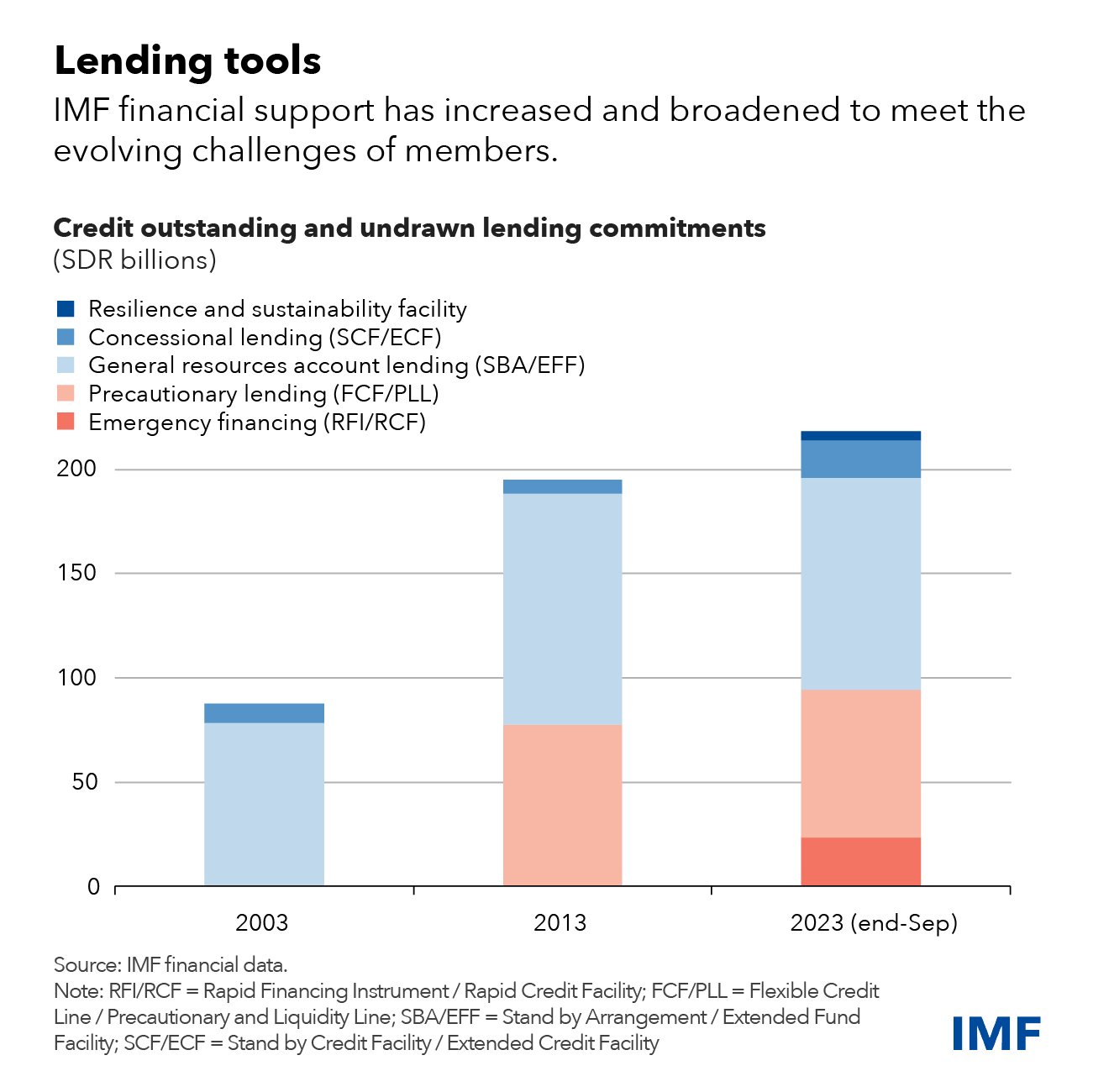

To be sure, the Fund acted to help members address balance-of-payments needs from recent shocks. This includes providing emergency financing and temporarily increasing access limits for Fund arrangements. We approved precautionary financing arrangements and established a Short-term Liquidity Line that serves as a backstop for members with very strong fundamentals. We responded to the global food crisis stemming from Russia’s war in Ukraine by introducing a Food Shock Window in September 2022 to help countries facing urgent balance of payments needs related to food insecurity.

Since the pandemic, we have deployed $1 trillion in global liquidity and reserves through our lending and the 2021 allocation of $650 billion in special drawing rights, or SDRs. We have provided around $320 billion in financing to 96 countries. We have increased five-fold our interest-free financing to 56 low-income countries through our Poverty Reduction and Growth Trust. And we have worked with economically stronger members to channel a significant share of their SDRs to more vulnerable countries, generating around $100 billion in new financing through IMF trusts such as the PRGT and the Resilience and Sustainability Trust introduced last year.

We continuously assess and improve our lending toolkit to ensure that can address today’s and tomorrow’s challenges:

Looking ahead

The IMF is committed to continue supporting member countries through policy advice, capacity development, and lending. The challenge is to support vulnerable countries that have limited fiscal space to implement politically costly reforms. Yet when financing is front-loaded but adjustment and reforms are backloaded, credibility is harder to establish. Securing additional external financing becomes difficult. All this puts at risk the completion of program reviews and the achievement of macroeconomic stabilization.

To help countries undertake and sustain adjustment, reforms and financing are needed that pay off sooner in terms of growth. Where debt concerns are acute, debt restructuring, and more grant financing may also be needed. The Fund is deepening collaboration with the World Bank and other multilateral institutions with expertise in structural reform areas, to suitably calibrate and sequence reforms under their core areas of work.

We need to ensure that the IMF has the resources to effectively exercise its lending function. The successful completion of the ongoing 16th General Review of Quotas will be essential to secure the Fund’s general resources, together with closing remaining fundraising gaps for the PRGT and RST. These will ensure that lending to vulnerable countries can continue in adequate volume and on favorable terms.

—See our factsheet on IMF lending instruments.