Regional Highlights

Voyage to Indonesia

Working together toward a common goal

The IMF-World Bank Annual Meetings are taking place in Bali in October 2018. The meetings will be a unique opportunity for Indonesia and Asia to share their achievements and provide lessons for other countries. Indonesia and its ASEAN partners have been successful in creating vibrant middle classes, opening the doors to higher living standards for millions of people. By generating strong growth over the past two decades, they have also become key drivers of the global economy.

Asia and the Pacific

Exploring Connections and Cooperation in the Region

20th Anniversary of the Regional Office for Asia and the Pacific

More than 400 people including the central bank governors of Mongolia and Nepal attended the events celebrating the 20th anniversary of the Regional Office for Asia and the Pacific (OAP), which was cohosted by the IMF and the Ministry of Finance in November in Tokyo.

The reception was like a reunion of OAP, attended by former directors including Mr. Kunio Saito, the first director, and staff flying in from overseas, people who used to work at the IMF, and who worked hard to open the Office in Tokyo in 1997. Mr. Taro Also, Deputy Prime Minister, and Mr. Haruhiko Kuroda, Governor of the Bank of Japan, delivered the speeches celebrating the occasion.

In the keynote speech, IMF Managing Director Christine Lagarde talked about Japan’s Gakuensai, the immensely popular university festivals organized by students, saying they are “forward-looking” and “firmly grounded in shared experiences,” and that is a fitting description of the partnership between Japan and the IMF. At a townhall meeting with the Managing Director, more than 60 scholars of the Japan-IMF Scholarship Program for Asia (JISPA) attended and put forward questions on the IMF’s views on the risks to economic growth in Asia. JISPA is funded by the Ministry of Finance and administered by OAP.

OAP will increase the footprint of the IMF in the region by continuing to manage JISPA and by organizing capacity building seminars and policy conferences in the region, as well as by handling the IMF’s on-the-ground relations with the regional fora, including the Asia Pacific Economic Cooperation (APEC) forum and the Association of Southeast Asian Nations (ASEAN).

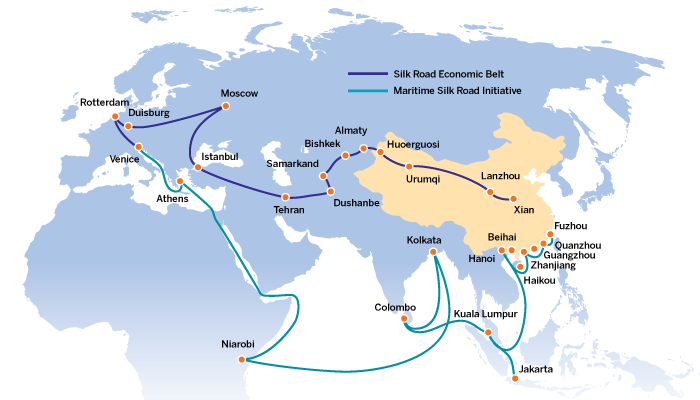

Belt and Road Initiative

China’s Belt and Road Initiative, launched in 2013, aims to promote connectivity and cooperation in infrastructure, trade, finance, and people-to-people exchanges by connecting Asia with Europe and Africa through the Middle East and across the Pacific to Latin American countries. The high-profile Belt and Road Forum for International Cooperation, in May 2017, was hosted by China and outlined a roadmap for the initiative. The initiative is expected to raise significant resources from China and various other sources, including the private sector, to support development and improve growth prospects.

A High-Level Conference on Macroeconomic and Financial Frameworks for the Successful Implementation of the Belt and Road Initiative, in April 2018, focused on how to realize the initiative’s potential and maximize its benefits while ensuring debt sustainability and proper project selection. In her speech, Managing Director Lagarde noted that higher infrastructure investment can help achieve more inclusive growth, attract more foreign direct investment, and create more jobs. At the same time, she emphasized the need to carefully manage the financing terms in countries with high public debt to avoid agreements that may lead to financial difficulties for both China and partner governments. She also emphasized ensuring transparent decision making.

At the event, Managing Director Lagarde and Governor Yi Gang of the People’s Bank of China inaugurated the China-IMF Capacity Development Center (CICDC), which aims to work with countries by organizing training courses, workshops, and peer-learning events that support sustainable and inclusive economic growth. CICDC will be anchored in Beijing and will support activities both inside and outside China, such as in countries associated with the Belt and Road Initiative.

Sub-Saharan Africa

Making an Investment in Sustainable Development

SSA Tax revenue to GDP

Source: IMF, Africa Department.

Sub-Saharan Africa’s Untapped Revenue Potential

The overarching policy challenge in sub-Saharan Africa is to improve living standards by achieving the Sustainable Development Goals. The most reliable source of development financing is domestically generated revenues. With the IMF capacity development and loans support, the region has made substantial progress over the past two decades (Figure 1.5) but still has significant potential to improve domestic revenue collection.

A recent IMF study estimates that sub-Saharan Africa could mobilize up to 5 percent of GDP in additional tax revenues—markedly more than what it receives each year from international aid. To tap this potential, countries must continue efforts to modernize tax administration systems and broaden the tax base.

Private Investment to Rejuvenate Growth

Private investment in sub-Saharan Africa has lagged other regions (Figure 1.6). More private domestic and foreign investment is critical for sustainable and inclusive growth. Empirical analysis suggests that current and prospective economic activity is the main driver of private firms’ decisions to invest. Moreover, growth’s impact on private investment decisions is strengthened by improved regulatory and insolvency frameworks, deeper financial markets, and trade liberalization.

Peer Learning in Sub-Saharan Africa

A network of six regional centers, covering all of sub-Saharan Africa, coordinates much of the IMF’s capacity development efforts on the ground, supporting economic institution building and good governance in the region. These centers ensure close coordination with member country officials and other development partners and are financed by development partners, member countries, and the IMF. Hands-on advice, regional training, and policy-oriented workshops are complemented by peer-learning activities so countries can share best practices and boost regional integration. In 2018, these events have included: a workshop hosted jointly with the government of Senegal and G20 Compact with Africa on economic diversification and growth, a conference hosted with the African Center for Economic Transformation and the Ghanaian government on mobilizing domestic revenue to overcome aid dependence, and a conference cohosted with the Rwandan government and UN Women on how to promote gender equality. Another prominent theme has been harnessing digital technologies to support taxation.

Private investment to GDP in developing countries, 2000–16

Source: IMF, World Economic Outlook database.

Note: EUR = Europe; LAC = Latin America and the Caribbean; MENA = Middle East and North Africa; SSA = Sub-Saharan Africa.

Europe

Stabilizing and Strengthening the European Economy

Centralized Fiscal Capacity for the Euro Area

The euro area crisis exposed shortcomings in the functioning of the currency union, and IMF staff have argued that further integration would make the euro area more resilient to shocks. An IMF paper outlines a proposal for a centralized fiscal capacity for the euro area that could help smooth both country-specific and common shocks. In particular, it suggests a macroeconomic stabilization fund financed by annual contributions from countries, used to build up assets in good times and make transfers to countries in bad, as well as a borrowing capacity in case large shocks exhaust the fund’s assets.

Simulations show that, even with relatively modest contributions, such a scheme would provide meaningful macroeconomic stabilization in a downturn. The centralized fiscal capacity involves risk-sharing across countries; therefore, to avoid moral hazard problems, transfers would need to be conditional on strict compliance with European Union fiscal rules. The note also discusses several features aimed at avoiding permanent transfers between countries and making the centralized fiscal capacity function as automatically as possible—to limit the scope for disputes over its operation—both of which are important points to make it politically acceptable.

Transforming France’s Economy

A conference on “Transforming France’s Economy and Completing the Integration of the Eurozone” in Paris, France, in February 2018, brought together leading policymakers, economists, and private sector representatives to discuss how to strengthen the resilience and growth potential of France and the euro area. The conference was cohosted by the IMF and the French Treasury.

In a conversation with French Minister of Finance Bruno Le Maire, IMF Managing Director Christine Lagarde stressed the importance of using the current recovery to push an ambitious reform agenda, both nationally and at the European level, to boost employment and productivity.

Policy Debates in Germany

High-ranking economists and policymakers from Germany and other countries met in January 2018 at a conference cohosted by the IMF and Deutsche Bundesbank to debate economic policy. The conference focused on areas in which the debate has been particularly intense: developments in wages and inflation, the appropriate fiscal policy stance, Germany’s current account surplus, and the post crisis agenda for the euro area and Germany. IMF Managing Director Christine Lagarde and Deutsche Bundesbank President Jens Weidmann gave keynote addresses, and the event featured a lively exchange of views and an opportunity for the IMF to deepen its engagement with Germany.

Sustaining Recovery in Spain

Spain’s successful responses to the financial crisis were the focus of the conference “Spain—From Recovery to Resilience,” cohosted by the IMF and Banco de España in Madrid in April 2018. The conference attendees shared lessons learned and policy options to ensure a sustained and inclusive economic path forward. IMF First Deputy Managing Director David Lipton delivered a keynote speech. Primary challenges discussed for the Spanish economy discussed related to elevated public debt, unfinished business in labor market reform, and weak medium-term productivity and growth prospects. The conference also debated how the European architecture can be strengthened further, in particular by completing the banking union.

Middle East and North Africa

Supporting Inclusive Growth through Government Reforms

How Governments in the Middle East Can “ACT NOW”

Seven years after the Arab Spring, people in the region still aspire to greater economic opportunity and prosperity. With 60 percent of the region’s people younger than 30 and 27 million youth joining the workplace in the next five years, policymakers must “ACT NOW” to create opportunities. The January 2018 “Opportunity for All” conference in Marrakesh, Morocco, organized by the IMF, the Arab Fund for Economic and Social Development, the Arab Monetary Fund, and the government of Morocco, called on governments to prioritize reforms to promote higher inclusive growth through greater:

Accountability: increase transparency, strengthen institutions, tackle corruption.

Competition: foster the private sector through better access to finance and regulation.

Technology and trade: leverage to generate new sources of growth.

No one left behind: build strong safety nets and strengthen rights of youth, women, rural populations, and refugees.

Opportunity: improve social and investment spending and pursue fairer taxation.

Work: invest in people and reform education to equip workers for the new economy.

Egypt Reform Program Helps Stabilize the Economy

The prolonged political transition and regional instability in Egypt after 2011 exacerbated longstanding structural challenges. This in turn resulted in slow growth, high public debt, and depleted official reserves. In 2016, to restore macroeconomic stability, the authorities developed a program of policies and structural reforms, supported by a three-year extended arrangement under the IMF’s Extended Fund Facility, to improve external competitiveness, decrease public debt, and promote inclusive growth.

A key part of the program was to improve revenue mobilization. A Tax Administration Diagnostic Assessment determined areas for improvement, including in tax return filing and payment. The Egyptian Tax Administration worked with METAC (the IMF’s regional capacity development center based in Beirut), to introduce new procedures in pilot offices. The pilots have produced encouraging results. Collection and filing rates in pilot offices have been, on average, twice that in nonpilot offices. The Egyptian government is looking to expand these reforms to help them reduce tax evasion and corruption.

After one year under the program, external and fiscal deficits have narrowed and growth accelerated. The authorities’ reform program has played a key role in stabilizing conditions, including alleviating foreign exchange shortages, strengthening social assistance, and expanding private investment and growth.

Financial Sector Repair in Caucasus and Central Asia

External shocks since 2014, including lower commodity prices and slower growth in main trading partners, have put banking sectors in the eight Caucasus and Central Asia (CCA) countries under stress. These shocks exacerbated financial vulnerabilities, including weak asset quality, high dollarization, connected lending, and shortcomings in financial regulation and supervision. All CCA countries have taken policy actions in response to the shocks, but more needs to be done to restore the health of CCA banking sectors.

The exact strategy will depend on banks’ financial health and will require prioritizing objectives. Countries where risks to financial stability remain elevated should focus on accurately assessing banks’ health and resolving those that are not viable. Efforts should also be devoted to strengthening the regulatory and supervisory frameworks in all CCA countries, which should include the following reforms: a strong governance structure that establishes independent risk management, compliance, and internal controls; effective risk-based and consolidated supervision; macroprudential frameworks; and an improved credit risk valuation. Implemented with a strong commitment from the authorities, these actions would allow the banking sector to contribute fully to higher and inclusive economic growth.

Western Hemisphere

Tackling Economic Challenges

Caribbean Forum: Unleashing Growth While Strengthening Resilience

The High-Level Caribbean Forum held in Kingston, Jamaica, in November 2017 was timely, as the region is facing multiple challenges—fiscal and financial vulnerabilities, youth unemployment, and exposure to frequent and costly natural disasters that collectively hinder the region’s growth. Participants discussed how to balance debt and growth in the current economic and political cycle juncture.

Following the forum, IMF Managing Director Christine Lagarde joined the town hall with students at the University of the West Indies, where IMF staff launched a book: Unleashing Growth and Strengthening Resilience in the Caribbean. The book brings together the latest research on the Caribbean economies conducted at the IMF. It analyzes the region’s macroeconomic imbalances and examines structural impediments affecting competitiveness and growth in its tourism-intensive economies.

Jamaica works closely with the IMF to build strong economic institutions to tackle some of these challenges. Much of the work is coordinated by the CARTAC (the IMF’s regional capacity development center based in Barbados).

Paraguay’s Macroeconomic Stability

In March 2018, the Managing Director visited Asunción to meet with President Horacio Cartes and other senior officials, visit social projects, and participate in several outreach events. After 24 years since an IMF Managing Director last visited the country, Lagarde noted Paraguay’s remarkable economic growth and social progress. Discussions focused on the importance of strengthening Paraguay’s macroeconomic stability, ensuring inclusive growth, and taking advantage of the country’s “demographic dividend” with a relatively youthful population. Paraguay’s National Development Plan prioritizes investment in the areas of infrastructure, health, and education.