What’s In and Out in Global Money

Finance & Development, September 2009, Volume 46, Number 3

Things are hot, then they are not, in the world of international money

IN international monetary economics our exam questions remain the same. Only the answers change, from decade to decade. I nominate five concepts, which were virtually conventional wisdom a short time ago, for my list of what is now “out.” I also nominate five concepts, which might have been described as “out” a few years ago, for my list of what is now “in.”

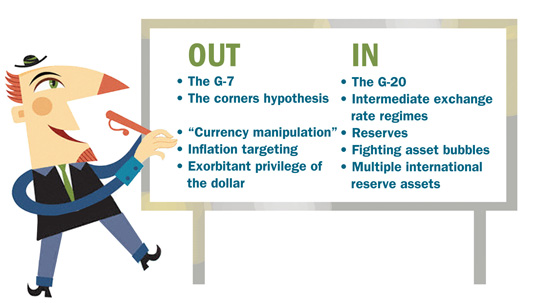

1. Out: The G-7

In: The G-20

Out: The G-7 (Group of Seven) world leaders first met in France in 1975, to ratify the de facto move to floating rates, following the demise of the Bretton Woods world. G-7 finance ministers cooperated to bring down a stratospheric dollar in 1985 and then again to halt the dollar’s depreciation in 1987, in the Plaza and Louvre agreements, respectively. The G-7—Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States—was the most important steering group of the world monetary system. But the membership became increasingly anachronistic. Russia’s addition in 1997, making it the G-8, was much too little, and too late. The exclusion of China and other major developing or emerging market countries rendered the group out of date. What can finance ministers accomplish by discussing a currency that is not represented at the table?

In: The G-20 adds 12 major economies and the European Union to the G-7—Argentina, Australia, Brazil, China, India, Indonesia, Mexico, Russia, Saudi Arabia, South Africa, South Korea, and Turkey. The G-20’s London meeting in April 2009 had some substantive successes and some failures. Regardless, the meeting was a turning point in that the G-20, more than the G-8, is making substantive decisions—finally giving major emerging countries representation.

2. Out: The corners hypothesis

In: Intermediate exchange rate regimes

Out: The corners hypothesis postulated that countries are—or should be—moving to one or another corner in their choice of exchange rate regimes: either full flexibility or rigid institutional commitments to fixed exchange rates in the form of currency board, dollarization, or monetary union. According to the hypothesis, anything in between the two extremes was no longer feasible.

The corners hypothesis arose (Eichengreen, 1994) in the context of the European exchange rate mechanism (ERM) crisis of 1992–93. The ERM had permitted the exchange rates of European currencies to fluctuate within a narrow band. But, under pressure, Italy, the United Kingdom, and others had to devalue or drop out—and only because the band was widened could France stay in. The crisis suggested to many that there was no middle ground between floating and fixing (a judgment seemingly borne out when the leap from wide bands to full monetary union proved successful in 1998–99). After the east Asia crises of 1997–98, the hypothesis was applied to emerging markets too. In efforts to reform the financial architecture to minimize the frequency and severity of future crises, the “fix or float” proposition rapidly became the conventional wisdom (Obstfeld and Rogoff, 1995; Summers, 1999; Meltzer, 2000).

Trouble was, the proposition was never properly demonstrated, either theoretically or empirically. The collapse in 2001 of Argentina’s convertibility plan, which had rigidly linked the peso to the dollar, marked the beginning of the end. Today, it is clear that most countries continue to occupy the vast expanse between floating and rigid institutional pegs, and it is uncommon to hear that intermediate regimes are a bad choice generically.

In: Intermediate exchange rate regimes. If the corners hypothesis is “out,” then intermediate regimes are “in.” Intermediate regimes include target zones (bands), crawls, basket pegs, adjustable pegs, and various combinations of them. The IMF classifies more than half of its members as following regimes somewhere in between free float and hard peg. Economists’ attempts to classify the regimes that countries actually follow (such as Frankel and Wei, 2008), sometimes in contrast to what they claim to follow, generally find an even higher proportion with intermediate regimes.

3. Out: “Currency manipulation”

In: Reserves

Out: “Currency manipulation.” In 2007, the IMF was supposedly given responsibility for surveillance over members’ exchange rates, which the United States believed meant telling China that the value of its currency was lower than it should be. The phrase “unfair currency manipulation” has had official status in U.S. law for 20 years and in the IMF Articles of Agreement for longer, despite its protectionist ring. In practice, the supposed injunction on surplus countries to revalue upward has almost never been enforced—in contrast to the pressure on deficit countries to devalue. Some would say it is time to rectify the asymmetry (Goldstein and Lardy, 2009). My view is that it is time to recognize two realities: first, it is normally not possible to identify with confidence the correct value of a currency—still less its “fair” value—and second, creditors are, and will always be, in a stronger position than debtors. It is time to retire the language of unfair currency manipulation.

U.S. legislators have argued that the Chinese renminbi is undervalued and that increased flexibility in China’s currency regime would be beneficial. These are both reasonable propositions. Politicians have overestimated their importance, however. Continued demands that China stop intervening in the foreign exchange market to keep the renminbi fixed against the dollar could be counterproductive.

In 2007, China moved further in the direction that outsiders had demanded: abandoning the dollar peg and effectively placing a substantial weight on the euro. But in the spring of 2008, China jettisoned the 2007 policy and returned to a dollar target. The reversion evidently was a response to Chinese exporters, who complained they had lost competitiveness in 2007, when the euro appreciated against the dollar. The expectation in 2008 was that the reversal would help Chinese export competitiveness at the expense of the United States. But the euro (surprisingly) depreciated against the dollar in 2008. Had China kept the 2007 policy instead of switching back to the dollar peg, the value of the renminbi would be lower today, not higher. Dollar-based producers would be at a greater competitive disadvantage.

The fundamental question, however, is longer term. The United States is dependent on China to fund its deficits. Although the U.S. current account deficit is now down by half, domestic debt is still rising alarmingly. If China and other Asian and commodity-exporting countries were to stop buying U.S. treasury bills, the result would be a fall in the value of the dollar together with a sharp increase in U.S. interest rates. U.S. legislators should be careful what they ask for, because they might get it.

In: Reserves. If intervention to dampen appreciation is no longer a sin, then reserves are a new virtue.

The number of floating and managed floating currencies has steadily increased since 1973. For many emerging markets, the increase in exchange rate flexibility was a response to the currency crises of 1994–2001.

In theory, countries that float need not hold reserves, let alone use them. Yet developing and emerging market countries took advantage of the boom of 2003–07 to build up their reserves to unheard heights. Instead of choosing between greater exchange rate flexibility and higher reserves, they chose both. Western economists delivered some persuasive-sounding arguments suggesting that many countries were holding far more reserves than they needed ($2 trillion now, in the case of China). They pointed out that most of these reserves were held in the form of low-yielding U.S. treasury bills (Summers, 2006; and Jeanne, 2007).

Emerging market countries perhaps knew their business better than economists. Foreign exchange reserves have provided self-insurance during the global liquidity crisis. Those countries that built up precautionary reserve holdings were able to avoid large depreciations in the “Panic of 2008” (Obstfeld, Shambaugh, and Taylor, 2009).

4. Out: Inflation targeting (narrowly defined)

In: Fighting asset bubbles

Out: Inflation targeting. The past 10 years have been the decade of inflation targeting (Svensson, 1995; Bernanke and others, 1999). Narrowly defined, inflation targeting commits central banks to annual inflation goals, invariably measured by the consumer price index (CPI), and to being judged on their ability to hit those targets. Flexible inflation targeting allows central banks to aim at both output and inflation, as enshrined in the famous Taylor Rule. The orthodoxy says that central banks should essentially pay no attention to asset prices, the exchange rate, or export prices, except to the extent that they are harbingers of inflation.

I believe that inflation targeting—at least the narrow definition—has already seen its best days.

First, the injunction to pay no attention to the exchange rate is one that perhaps only a dozen committed floaters—if any—can live by. Most countries that say they float don’t. Instead, they have a “fear of floating” and feel the need to intervene to moderate fluctuations in the demand for their currencies (Calvo and Reinhart, 2002).

Second, and most important for large advanced economies, is the issue of asset prices. A decade ago, most monetary economists went along with former Federal Reserve Board Chairman Alan Greenspan’s doctrine that it is hopeless to try to identify and prick speculative bubbles in stock markets and real estate markets while they are in progress—and that cutting interest rates after they crash is enough to protect the economy. Recent experience has changed minds.

Third, choosing the CPI as the price index of interest is needlessly destabilizing to the international accounts for countries where trade shocks are important. An alternative price index such as the producer price index or an index of export prices would more appropriately accommodate fluctuations in the terms of trade (Frankel, 2005).

In: Fighting asset bubbles. For 30 years, excessive monetary expansion was believed synonymous with inflation getting out of control, eventually necessitating monetary contraction and, usually, a recession, to return to price stability. This description did fit the recessions of 1974, 1980, 1981–82, and 1990–91. But the 20th century is replete with examples of big asset booms that ended in devastating crashes, where monetary policy, in retrospect, was too easy during the boom phase and yet where inflation did not show up at any stage. The 1920s real estate boom in Florida and stock market boom in New York, followed by the 1929 crash and Great Depression; the 1986–89 stock market and real estate bubbles in Japan, followed by its decade of stagnation; the Asia boom and bust in the 1990s; and the U.S. experience of the past decade all fit this pattern well. (Borio, 2005, pointed this out before the current financial crisis began in 2007.)

Greenspan’s doctrine can be answered with four points. First, identifying bubbles is no harder than identifying inflationary pressures 18 months ahead of time. Second, monetary authorities do have tools to prick speculative bubbles. Third, the policy of coming to the rescue of the markets after the crash created a moral hazard problem that exacerbated the bubbles. Fourth, the cost in terms of lost output can be enormous even when the central bank eases aggressively, as we have recently learned.

5. Out: Exorbitant privilege of the dollar

In: Multiple international reserve assets

Out: Exorbitant privilege of the dollar. Can the U.S. current account deficit be sustained without a major depreciation of the dollar? Will the United States continue to enjoy the unique privilege of being able to borrow virtually unlimited amounts in its own currency? If so, does this privilege warrant the label “exorbitant”—meaning that the benefit traces solely to attributes such as size and history rather than to virtuous behavior such as budget discipline, price stability, and a stable exchange rate? Since 1980, the United States has racked up $10 trillion in debt. Between January 1973 and May 2009, the dollar depreciated 30 percent against the Federal Reserve’s Major Currency Index. It seems unlikely that macroeconomic policy discipline is what has enabled the United States to keep its privilege.

Some argue that the United States maintains the privilege to incur dollar liabilities by exploiting its comparative advantage in supplying high-quality assets to the rest of the world (Caballero, Farhi, and Gourinchas, 2008; Forbes, 2008; Gourinchas and Rey, 2007; Ju and Wei, 2008; and Mendoza, Quadrini, and Rios-Rull, 2007).

Under that interpretation, the fundamental cause of the current account imbalances is a glut of savings in Asia and other countries looking for good investments. That reasoning would seem to be undermined by the low quality of American assets that was suddenly revealed in 2007 and the loss of credibility of U.S. financial institutions in the subsequent crisis.

Although the more exotic arguments about the uniquely high quality of U.S. private assets have been tarnished, the basic idea of American exorbitant privilege is still alive: the dollar is the world’s reserve currency, by virtue of U.S. size and history. The question then becomes whether the dollar’s unique role is eternal, or whether a sufficiently long record of deficits and depreciation could induce investors to turn elsewhere. (See “The Future of Reserve Currencies” in this issue.)

In: Multiple international reserve assets. Does the dollar have credible rivals for the position of sole leading international reserve currency? The two putative challengers of the 1970s and 1980s, the yen and the deutsche mark, had limited heft. The euro, however, is a plausible alternative. There are also some new or revived reserve assets—including the IMF’s Special Drawing Right (SDR). Most likely is a system with several international reserve assets, rather than one that relies overwhelmingly on the dollar.

What determines reserve currency status? Economic size, depth of financial markets, rate of return, and the inertia of history. Euroland is approximately the size of the United States. For the first time, the credibility of U.S. financial markets as limitless, deep, liquid, and trustworthy has been impaired by the crisis. Moreover, the dollar has shown a poor ability to keep its value over time, whether measured by the level or volatility of the exchange rate.

Yes, the current era resembles the Bretton Woods system of the 1960s, with foreign central banks buying up surplus dollars to prevent their own currencies from appreciating. But we are closer to the end than the beginning. Conditions resemble those of 1971, when expansionary U.S. monetary and fiscal policies produced a declining trade balance and overall balance of payments, causing the collapse of the system. There is no reason to expect a different outcome this time. The United States cannot necessarily rely on support of foreign creditor governments.

Changes in reserve currencies come slowly, but eventually a tipping point is reached. The best precedent is the British pound sterling, which was overtaken by the dollar sometime between 1931 and 1945. Menzie Chinn and I (2008) estimated that a similar tipping point could be reached between the dollar and the euro, with the euro pulling ahead by 2022. This two-currency simulation should not be taken too literally. A more likely successor to the era of unipolar dollar domination is a multiple reserve system.

This year, other international assets have begun to show up in central bank reserve acquisitions as well as the euro. First is the SDR. It was born at the end of the 1960s as a medicine prescribed too late for the rapidly deteriorating Bretton Woods patient. The SDRs issued in the early 1970s established their claim as an international reserve asset, but the quantities were far too small to matter. By the 1990s the unit had all but disappeared from the world monetary system (Eichengreen and Frankel, 1996).

The SDR accomplished a stunning return from the dead at the G-20 meeting in April, when leaders decided not only to triple the size of the IMF but also to issue a new batch for the first time in years. Subsequently China suggested replacing the dollar as international currency with the SDR. Without a major region or country using the SDR as its home currency it does not stand much chance of competing with the euro or the yen, let alone the dollar. Nevertheless, it seems likely that the SDR will now rejoin the list of serious alternative assets in a multiple reserve currency system, especially if the IMF were to adopt “substitution account” proposals to allow members to swap unwanted dollars for SDRs.

Second, after decades when the conventional wisdom considered large holdings of dusty piles of gold bars anachronistic, to be gradually sold off by central banks, the yellow metal is also back in fashion. It was reported this year that the People’s Bank of China has sharply increased its gold holdings, as an alternative to unlimited dollar acquisition.

Third, the yen has acquired some safe haven status recently.

Then there is the renminbi. Although it would take substantial development and opening of China’s financial markets, the renminbi could become an international currency within a decade and possibly one of the most important in 30 years. But it would be part of a system of multiple reserve currencies—one that would also include the dollar, the euro, the yen, pound, Swiss franc, and SDR, and perhaps even gold as well.

A multiple reserve currency system is inefficient, in the same sense that a barter economy is inefficient. But the existence of competitor currencies gives the rest of the world protection against the leader exploiting its position by running up too much debt and then inflating or depreciating it away.

References:

Bernanke, B., T. Laubach, F. Mishkin, and A. Posen, 1999, Inflation Targeting: Lessons from the International Experience (Princeton, New Jersey: Princeton University Press).

Borio, Claudio, 2005, “Monetary and Financial Stability: So Close and Yet So Far?” National Institute Economic Review, Vol. 192, No. 1, pp. 84–101.

Caballero, R., E. Farhi, and P. Gourinchas, 2008, “An Equilibrium Model of ‘Global Imbalances’ and Low Interest Rates,” American Economic Review, Vol. 98, No. 1, pp. 358–93.

Calvo, Guillermo, and Carmen Reinhart, 2002, “Fear of Floating,” Quarterly Journal of Economics, Vol. 117, No. 2, pp. 379–408.

Chinn, Menzie, 2005, “Getting Serious About the Twin Deficits,” Council Special Report No. 10 (New York: Council on Foreign

Relations).

———, and Jeffrey Frankel, 2008, “Why the Euro Will Rival the Dollar,” International Finance, Vol. 11, No. 1, pp. 49–73.

Eichengreen, Barry, 1994, International Monetary Arrangements for the 21st Century (Washington: Brookings Institution).

———, and Jeffrey Frankel, 1996, “The SDR, Reserve Currencies, and the Future of the International Monetary System,” in The Future of the SDR in Light of Changes in the International Financial System, ed. by M. Mussa, J. Boughton, and P. Isard (Washington: International Monetary Fund).

Forbes, Kristin, 2008, “Why Do Foreigners Invest in the United States?” NBER Working Paper 13908 (Cambridge, Massachusetts: National Bureau for Economic Research).

Frankel, Jeffrey, 2005, “Peg the Export Price Index: A Proposed Monetary Regime for Small Countries,” Journal of Policy Modeling, Vol. 27, No. 4, pp. 495–508.

———, and Shang-Jin Wei, 2008, “Estimation of De Facto Exchange Rate Regimes: Synthesis of The Techniques for Inferring Flexibility and Basket Weights,” IMF Staff Papers, Vol. 55, pp. 384–416.

Goldstein, Morris, and Nicholas Lardy, 2009, The Future of China’s Exchange Rate Policy (Washington: Peterson Institute for International Economics).

Gourinchas, Pierre-Olivier, and Hélène Rey, 2007, “From World Banker to World Venture Capitalist: U.S. External Adjustment and the Exorbitant Privilege,” in G7 Current Account Imbalances, ed. by R. Clarida, (Chicago: University of Chicago Press), pp. 11–66.

Jeanne, Olivier, 2007, “International Reserves in Emerging Market Countries: Too Much of a Good Thing?” Brookings Papers on Economic Activity: 1, Brookings Institution, pp. 1–55.

Ju, Jiandong, and Shang-Jin Wei, 2008, “When Is Quality of Financial System a Source of Comparative Advantage?” NBER Working Paper 13984 (Cambridge, Massachusetts: National Bureau for Economic Research).

Meltzer, Allan, 2000, Report of the International Financial Institution Advisory Commission, Submitted to the U.S. Congress, March.

Mendoza, E., V. Quadrini, and J. Rios-Rull, 2007, “Financial Integration, Financial Deepness and Global Imbalances,” NBER Working Paper 12909 (Cambridge, Massachusetts: National Bureau for Economic Research).

Obstfeld, Maurice, and Kenneth Rogoff, 1995, “The Mirage of Fixed Exchange Rates,” Journal of Economic Perspectives, Vol. 9, No. 4, pp. 73–96.

Obstfeld, M., J. Shambaugh, and A. Taylor, 2009, “Financial Instability, Reserves, and Central Bank Swap Lines in the Panic of 2008,” American Economic Review, Vol. 99, No. 2, pp. 480–86.

Summers, Lawrence, 1999, Testimony before the Senate Foreign Relations Subcommittee on International Economic Policy and Export/Trade Promotion, January.

———, 2006, “Reflections on Global Account Imbalances and Emerging Markets Reserve Accumulation,” L.K. Jha Memorial Lecture, Reserve Bank of India, March 24.

Svensson, Lars, 1995, “The Swedish Experience of an Inflation Target,” in Inflation Targets, ed. by L. Liederman and L. Svensson (London: Centre for Economic Policy Research).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org