Searching for Stability

Finance & Development, June 2010, Volume 47, Number 2

Bas B. Bakker and Anne-Marie Gulde

Eastern Europe rode a decade-long boom into a serious bust and now must figure out how to restart growth on a more even keel

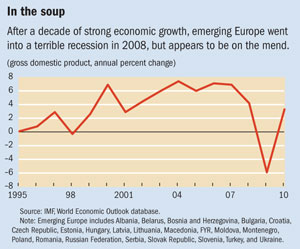

EASTERN Europe grew very rapidly in the decade and a half that preceded the global economic and financial crisis (see chart). As the region completed its transition from central planning to successful market economies, most countries sharply narrowed the gap with income levels in western Europe. There were bumps in the transition, but most were managed well.

That is, until now. In 2009, the region’s rapid growth abruptly halted and most countries went into a deep recession. Gross domestic product (GDP) for the region contracted by 6 percent—compared with growth of almost 7 percent in 2007, the last full year before the crisis. But not all countries were hit equally hard. In two countries, Albania and Poland, there was no recession, whereas in Latvia GDP fell 18 percent and Lithuania and Ukraine registered 15 percent declines.

The recession seems to be ending. Exports are rebounding, and domestic demand is showing signs of stabilization. Most countries will see positive GDP growth this year. Now policymakers must answer two important questions: what drove the boom-bust cycle and how can the region restart more sustainable growth?

Was the boom always doomed?

Economic theory predicts that capital should flow from richer to poorer countries. That’s what happened in eastern Europe. With low wages, low capital-labor ratios, and well-educated populations, eastern Europe was an attractive destination for outside investors. Low interest rates in western Europe enhanced that attraction. Starting in 2003, western European banks began to invest vigorously in eastern Europe’s growing markets—and in the ensuing competition, credit conditions loosened and growth became unbalanced. Capital inflows went largely to sectors such as real estate, construction, and banking that did not produce tradable goods—boosting domestic demand but not supply. That led to a surge in imports, unprecedented current account deficits, and overheating economies.

Moreover, much lending was done in foreign currency, which generated large balance sheet risks for borrowers that earned income in domestic currency and owed money in another. In most cases, subsidiaries of foreign banks, funded by the parent, were the primary source of rapid credit growth.

By 2008, a number of countries had very large current account deficits (in Bulgaria and Latvia peaking at about 25 percent of GDP), high external debt, rapidly rising wages, and accelerating inflation. There was also a boom in asset prices, especially in housing.

Unbalanced growth was not an issue in all countries. In countries such as the Czech and Slovak Republics—which started their transition earlier, were richer, and had flexible exchange rates—credit growth was more modest; there was also little foreign currency lending, the economies did not overheat much, and wage growth was restrained. In Poland, there were fewer imbalances because the credit boom started later.

In the fall of 2008, the capital inflows came to a sudden stop. In the global financial turmoil that followed the demise of the investment bank Lehman Brothers, global risk aversion rose sharply, stock prices fell precipitously, and interbank markets dried up. Banks in advanced economies came under severe liquidity pressure and virtually stopped new lending or even shed assets. Parent banks continued to roll over outstanding credit lines to their subsidiaries, but they no longer provided additional funds, limiting new credit to what could be financed from increases in local deposits. Other capital inflows to the region declined as well, although not as sharply.

The decline in capital inflows caused a sharp drop in domestic demand. In many cases, new credit came to a virtual halt. Domestic demand contracted most in countries that previously had the biggest increases in domestic demand, the largest current account deficits, and the highest rises in credit-to-GDP ratios. In countries without large imbalances, domestic demand held up better.

The recession was exacerbated by a drop in exports. Emerging Europe’s principal trading partners were also in recession. With domestic demand and exports shrinking, the GDP decline in many countries far exceeded that in previous crises.

Stabilization

Still, the total financial and economic meltdown some had feared was averted. There were no banking panics, and—unlike in many advanced economies—governments did not have to step in to save entire banking systems. Nor was there a collapse of any fixed exchange rate regimes—which often happened in earlier crises in emerging economies.

Much of this was due to decisive domestic policy actions, but international support played an important stabilizing role. In several countries, the IMF stepped in—joined by the European Union (EU) in EU member countries. Other international financial institutions such as the World Bank and the European Bank for Reconstruction and Development were part of the program, and in some cases there were also financing commitments by other European countries. The private sector also contributed. Agreements with western European banks ensured continued lending to eastern European countries.

The way ahead

Eastern Europe seems poised for recovery. Exports are rebounding and domestic demand is showing signs of stabilizing. The IMF predicts the region will grow by 3.3 percent in 2010.

Still, emerging Europe cannot return to business as usual. Future growth—especially in countries that had built up large imbalances during the boom—must rely more on capital flows into the tradables sector and less on flows into the nontradables sector. In these countries, exports are recovering, but domestic demand will likely stay weak as consumers continue to rein in spending to pay off debt.

Private sectors in countries that experienced the boom must develop new markets for exports of manufactured goods and services, which will require restructuring of their economies. That is no mean task, but it is achievable. Restructuring will be helped by market signals that will change as profits in the nontradables sector shrink and investments seek more promising venues. But the process may be difficult. Even in the tradables sector, new projects may have to fight for much scarcer financing. Inflows will remain reduced as western banks struggle to rebuild their balance sheets and risk-adjusted returns in emerging Europe seem less attractive.

But public policies can play a role as well in steering eastern Europe toward a more sustainable growth path. More balanced macroeconomic policies and wage restraint can help prevent the overheating that pulls resources from the tradables to the nontradables sector. Fiscal policy in particular could play a much more active role—saving money when revenues are growing instead of increasing spending and boosting public wages. This may mean that during boom times small fiscal surpluses are not sufficient—that large surpluses are needed. Policymakers may prefer to spend in boom times, but the payoff of saving is that a large fiscal buffer will reduce the need to cut expenditure sharply during a recession—as several countries had to do during this crisis.

Preventing overheating is important, because manufacturing competitiveness in many emerging European economies deteriorated during the boom. For example, according to EU data, Latvia’s unit labor costs in manufacturing rose 90 percent relative to its trading partners between 2003 and 2008. Some other countries—notably Bulgaria, Estonia, and Romania—also experienced a sharp appreciation of their real exchange rate.

Tighter fiscal policy will help moderate wage growth. Over time, wages will catch up with those in western Europe. But if the catch-up goes hand in hand with productivity increases in manufacturing, it need not impede competitiveness nor discourage investors.

Increasing quality

But emerging Europe should not compete on low wages alone—and will find it difficult to do so. Other emerging markets have even lower wages now and, as workers emigrate to western Europe, wages will rise in emerging Europe. Instead, the region should aim to produce increasingly sophisticated products. Structural reforms, including those that bolster the business climate, could help, as would improving education and, in some nations, fighting corruption.

Foreign capital inflows can also play an important role, if they are aimed at enhancing supply, especially in the external trade–oriented sector. Such investment would support growth, transfer technology, and help contribute to an improvement of labor force skills.

Some countries in the region are already following this model. In the Czech and Slovak Republics, growth during the boom was much more balanced, credit growth more restrained, and current account deficits small—and exports played an important role. Although this strategy produced growth more muted than in some of their neighbors before the crisis, their recessions were much less deep. As a result, over a longer horizon, these two countries have grown faster than countries that had a domestic demand boom.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org