Serving Up Growth

Finance & Development, June 2010, Volume 47, Number 2

Promoting the services sector in Asia is another way to restore balance and boost growth

ARCHANA NANANCHERLA attributes India’s economic success to her compatriots’ appetite for hard work. “We work harder than others . . . it is a trait of Indians,” she declares. But perhaps it is Nanancherla herself and people like her—educated, working in the service sector, with growing disposable income—who are the real secret behind India’s domestic-led growth.

Nanancherla was recruited straight out of college by Tata Consultancy Services, the largest information technology and business process outsourcing services firm in India. She is now a project manager with responsibility for up to 120 people and a salary of about $5,000 a month. Nanancherla’s way of life offers valuable lessons for other Asian economies seeking to maintain their growth momentum.

Maintaining Asia’s growth

India differs from the many Asian economies that have relied on manufactured exports to power growth. This was evident during the 2008–09 global recession, when the slump in demand from the United States and Europe hit the region disproportionately hard (see “Asia Leading the Way,” in this issue of F&D). A key medium-term challenge for Asia will be to reduce that dependency on exports and strengthen domestic sources of growth—a pattern already set by India.

Many observers blame weak private consumption—often referred to as the Asian “savings glut”—or investment for Asia’s unbalanced growth. But, on the supply side, increasing production by developing Asia’s service sector would restore that balance and boost growth.

Some Asian economies’ consumption or investment may be too low, but they cannot all be characterized as weak. Ratios of consumption and investment to gross domestic product (GDP) vary widely across the region. Factoring in country-specific differences and long-term historical norms adds another level of nuance. The empirical evidence on domestic demand-side imbalances is mixed.

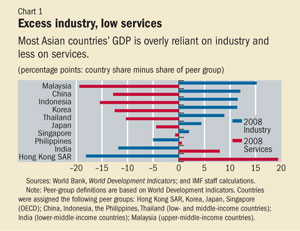

However, it’s easy to overlook the supply-side counterpart of high dependence on exports. Asia’s external dependence has led to an unbalanced production structure, with overreliance on tradable, or manufactured, goods, which broadly corresponds to the industrial sector (IMF, 2010). For example, at about 50 percent, industry’s contribution to GDP in China is nearly twice the Organization for Economic Cooperation and Development average and more than 10 percentage points of GDP above the world average for low- and middle-income countries. This overreliance on industry also characterizes other emerging Asian economies, such as the Association of Southeast Asian Nations (ASEAN)-4—and even advanced economies such as Japan and Korea (see Chart 1). In all these cases, industry’s contribution to GDP is high, often 5 to 10 percentage points above that for comparator countries.

Overreliance on the industrial sector has increased over the past decade, and global economic studies confirm that industry’s share of GDP is above the norm, especially in China and the ASEAN-4 economies.

Service with a smile

Given Asia’s dependence on exports, it is no surprise that services’ share in GDP is generally low by international standards. For example, in 2008 China’s service sector GDP share was nearly 13 percentage points below the low- and middle-income country average. The same holds true even for Singapore, which as a financial center is a service-based economy. Employment patterns—the distribution of the labor force across agriculture, industry, and the service sector—confirm Asian economies’ overexposure to industry and underexposure to services.

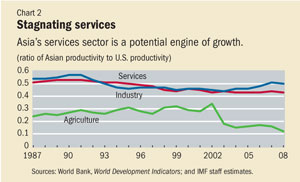

The dominance of industry has been an important factor in Asian economies’ strong growth performance and rapid rise in living standards. Rapid industrialization allowed hundreds of millions of workers to move out of low-paying jobs, particularly in agriculture, where Asian productivity levels have remained very low (see Chart 2). But future growth will depend on the service sector. As Asian economies, starting with Japan and Korea, move into a postindustrial world, the service sector must create jobs and catch up with productivity levels in advanced economies. Until now, productivity growth in Asia’s service sector has stagnated compared with that of the United States in recent years.

How then can the service sector help Asian economies achieve greater and more balanced growth?

Perhaps India has the answer. The service sector has been one of the most dynamic parts of its economy, leading GDP growth for the past two decades. Unlike in other Asian economies, India’s service sector productivity growth has tended to be higher than that in industry, thanks to:

- advances in communications technology, which gave India’s ample supply of trained, English-speaking workers access to growing domestic and global markets;

- successful deregulation of services;

- privatization;

- foreign direct investment; and

- financial sector reforms.

Unlocking growth potential

Broad empirical studies suggest that deregulation and exposure to foreign competition could unlock the service sector’s growth potential; improved access to financial services—especially for smaller firms, which often dominate key areas of the service sector, such as retail trade—could help alleviate resource constraints on growth. In Korea, for example, small and medium-sized enterprises account for 80 percent of service sector output.

In some cases, exchange rate appreciation would help shift resources to the nontradables sector by allowing a rise in their relative price. This in turn would reduce profit margins in the tradables sector and increase profit margins in the nontradables sector. Similarly, labor market reforms to facilitate hiring and firing workers as well as retraining incentives could help achieve smooth reallocation of resources. In many Asian economies, policies are already aimed at increasing competition in infrastructure-related services, opening up the retail and financial sectors, and lifting restrictions on foreign providers’ entry into social services, such as health and education.

These reforms would benefit the service sector but also strengthen domestic demand. Since the Asian crisis, firm-level investment in the ASEAN economies has become more sensitive to the availability of internal funds. Firms find it hard to access bank loans and other external funds to finance investment. This problem is especially acute for small, domestically orientated firms operating in the service sector.

Warming the investment climate

Smaller and more service-oriented firms’ access to financing could be strengthened by a shift toward more lending on risk-based terms; reforming collateral laws to allow businesses to secure loans with a wider range of assets than real estate and similar fixed assets); and widening the pool of venture capital funding through targeted tax breaks, as Malaysia has done. Deepening credit information and extending the coverage of credit registries (as introduced in the Philippines) through the 2008 establishment of the Credit Information Corporation has helped by improving banks’ ability to assess credit risk. Reducing credit risk through a modernized corporate restructuring framework for small and medium-sized enterprises would also enhance access to financing.

The Korea Asset Management Corporation, for example, successfully created a market for distressed Korean corporate debt by purchasing nonperforming loans from banks and repackaging them for sale to investors. Similar companies could specialize in restructuring small firms’ distressed debt.

Improvements in the overall investment or business climate are paving the way for more service sector–based growth in Asia. But even though the structural reforms implemented since the Asian crisis have made a substantive difference, perceptions have not yet caught up with the new reality. For example, indicators based on investor perceptions, such as governance—which worsened with the Asian financial crisis—still tend to lag those in advanced economies and exert a drag on investment activity. Asian economies need to continue increasing the competitiveness of their product and labor markets, as Hong Kong SAR has done with the adoption of a competition law; leveling the playing field for foreign investors, as Malaysia did recently when it lowered restrictions on foreign investment in the service sector; and ensuring contract enforcement and reducing administrative bottlenecks—a step taken in Indonesia and Malaysia with their one-stop shops for foreign investors. Only with such measures will Asia be able to unlock its full growth potential—and will Asians like Nanancherla be able to put their faith in more than their people’s capacity for hard work.

Olaf Unteroberdoerster is a Senior Economist in the IMF’s Asia and Pacific Department.

This article is based on the author’s 2010 study with Adil Mohommad and Papa N’Diaye “Does Asia Need Rebalancing?” Chapter 3, Regional Economic Outlook: Asia and Pacific (April).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org