Trusting the Government

Finance & Development, December 2010, Vol. 47, No. 4

Marc Quintyn and Geneviève Verdier

Confidence in government is the key to financial developmen

THE epicenter of the recent financial crisis was in countries with the most developed financial systems, raising questions about the advantages of such systems. But there is still broad consensus that financial development—the creation of a financial system that ensures effective intermediation between saving and investment via banking, insurance, and stock and bond markets—contributes to economic growth and a better standard of living.

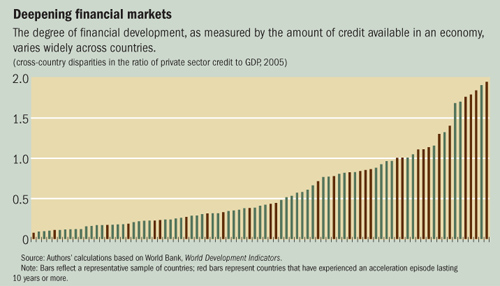

To reap the benefits of deep and well-functioning financial markets, many countries liberalized their financial systems in the hope of jump-starting financial development. Industrialized countries led the reform efforts in the 1970s, followed by many middle- and low-income countries. However, efforts to stimulate the financial sector have had uneven results: liberalization has fostered financial development in a number of countries, but financial systems in a majority of countries have remained small and underdeveloped by most standards. In some cases, short-term surges in financial development even led to severe financial crises following liberalization. These varied outcomes (see chart) prompted a decades-long search for policies and institutional features conducive to financial development.

We have found that financial liberalization is a necessary but not sufficient condition for financial development (Quintyn and Verdier, 2010). Our research concludes that financial development depends not only on the prevailing macroeconomic environment, policy design, and principles such as property rights and contract enforcement, but especially on the quality of the political systems that uphold these principles. Political institutions that keep politicians’ actions in check reassure savers, investors, and borrowers that their property rights will be protected.

From repression to liberalization

Post–World War II attempts to use the financial system as an engine for economic growth were characterized by direct state intervention to channel funds to sectors designated as crucial for development. This strategy was popular in low- and middle-income countries and was employed to some degree even in several advanced economies. In its extreme form, such government-led strategy relied on state-owned banks and a host of administrative controls on financial institutions (including interest rate controls, credit ceilings, directed credit, and strict limits on entry into the sector). Far from yielding the expected economic growth and development outcomes, it had perverse effects, including suboptimal allocation of capital and widespread corruption, and it discouraged saving.

This strategy, baptized “financial repression” by authors such as McKinnon (1973) and Shaw (1973), was gradually abandoned by the early 1970s. It was replaced by financial liberalization: elimination of administrative controls on financial institutions (including on interest rates); privatization of state-owned banks and authorization of more private banks; entrance of foreign banks into the domestic sector; and (later in the process) capital account openness. The ultimate goal of these measures was a competitive financial system that could allocate financial resources to the economy based on risk and return. Financial liberalization required a new approach to prudential supervision, to ensure that the financial institutions’ risk management was on a sound footing.

Many countries have since embarked on this type of liberalization, with mixed results. In fact, if anything, the gap between countries with developed financial systems—as measured by bank credit to the private sector as a share of gross domestic product (GDP), a common yardstick of financial development—and “laggards” has been growing since the 1990s. For a better indication of banks’ role as intermediaries of financial resources, we prefer to use private sector credit as a measure rather than other criteria, such as bank deposits to GDP. Admittedly, private sector credit does not take into account other features of financial sector development, such as the quality of financial services or stock market development. However, since most financial systems are dominated by banks, and private sector credit data are readily available for a wide range of countries, we opted for this variable, which, we believe, captures broad developments in most of the world.

Keeping a promise

Faced with these disappointing outcomes, one strand of research points to the prevailing legal system among institutional factors crucial to financial development. For example, common law supports financial development, because it protects individuals from the state more than other legal traditions do (La Porta and others, 1998).

Other researchers have looked at the degree to which countries effectively protect property rights (Acemoglu and Johnson, 2005). Inherent in each financial transaction is the promise of future repayment. Economic agents willingly engage in financial transactions if this promise is backed by a credible enforcement mechanism—that is, if their property rights are effectively protected. Hence, the argument goes, sustained financial development will take place only if all parties involved believe that promises will be honored.

This finding, however important, raises the question of the ultimate source of effective protection of property rights. A number of authors argue that political institutions are crucial: essentially, only governments can ensure that protection is not simply written into law, but is carried out effectively. Economic agents must trust that the political system will give those in power the incentive to enforce property rights. Financial development may be best served if governments are strong enough to effectively protect property rights and willing to keep their own power in check to prevent abuse (Haber, North, and Weingast, 2008; and Keefer, 2008). This delicate equilibrium rests on political actors’ willingness to submit to a system of checks and balances. Trust in government will result in increased financial activity. According to this view, the quality of a country’s political institutions is the ultimate determinant of financial development. We found that most long-lasting episodes of financial deepening have indeed occurred in countries with high-quality and stable political institutions.

Accelerating financial development

To test the hypothesis, we analyzed developments in the ratio of private sector credit to GDP. We looked at a sample of 160 high-, middle-, and low-income countries during 1960–2005 and identified 209 periods of accelerated financial development—defined as annual growth in the ratio of private sector credit to GDP of more than 2 percent for at least five years. We applied a centered three-year moving average that allowed us to avoid “accidents” or random one-year changes.

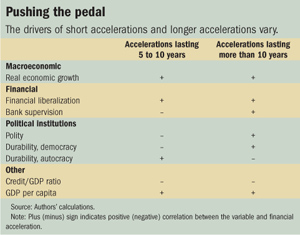

The episodes of financial acceleration ranged in length from 5 years (the imposed minimum) to as long as 22 years. Based on criteria established in the literature, we divided the acceleration periods into short ones (lasting between 5 and 10 years) and long, sustained ones (longer than 10 years). Of the 209 episodes, only 48—just over one-fifth—were long. Most countries that now have highly developed financial systems experienced a sustained acceleration at some point during the past 50 years. But that by itself is no guarantee of success; reversals occurred in a number of countries.

To test our political institutions hypothesis, we compared the prevailing economic and institutional conditions at the start of short-term accelerations and sustained accelerations. We examined whether, and how, a given set of factors—macroeconomic variables, financial liberalization, and types of political institutions—affect acceleration. Macroeconomic variables include GDP growth and inflation. Financial liberalization is captured by an index. The quality of political institutions is reflected in a polity index (Polity IV Project)that ranges from –10 (autocratic regimes) to +10 (democratic regimes).

We found that the determinants of financial acceleration vary between short and long episodes. Favorable macroeconomic conditions increase the likelihood of all types of acceleration. The same is true for financial liberalization. When a country takes measures to liberalize its financial system, it has a significant and large impact on the probability of all types of acceleration.

The big difference is in the impact of the political institutions variable. Our results strongly support the view that political institutions matter, suggesting that countries with checks and balances in their political system—that is, more democratic regimes—are more likely to experience sustained financial development. In contrast, we find that the polity variable has a significant and negative effect on the probability of a short acceleration period. This suggests that countries with political systems with high democratic content are also less likely to experience short-lived financial development.

To further investigate the impact of political stability on financial development, we also considered the effect of the durability (length in years) of the political regime. The results show that the durability of a democratic regime—a combination of stability and high-quality political institutions—greatly increases the probability of a sustained period of financial development.

Fertile ground

We found that countries with weaker political institutions are more likely to experience temporary surges in financial development. In contrast, countries with political institutions that include checks and balances are more likely to experience genuine long-lasting financial deepening following financial liberalization. Durable democratic regimes—those that offer a combination of stability and high-quality political institutions with players subject to checks and balances—offer the most fertile ground for financial deepening.

Financial liberalization is a strong impetus for financial acceleration, but it is not enough for sustained deepening of the financial sector. This requires financial liberalization measures supported by a political environment that instills trust—trust that financial promises will be enforced and that the government will not overrule property rights. Such trust stems from the quality of the political institutions and their durability. ■

Marc Quintyn is a Division Chief in the IMF Institute, and Geneviève Verdier is an Economist in the IMF’s African Department.

References:

Acemoglu, Daron, and Simon Johnson, 2005, “Unbundling Institutions,” Journal of Political Economy, Vol. 113, No. 5, pp. 949–95.

Haber, Stephen, Douglass North, and Barry Weingast, 2008, “Political Institutions and Financial Development,” in Political Institutions and Financial Development, ed. by Stephen Haber, Douglass North, and Barry Weingast (Stanford, California: Stanford University Press), pp. 1–9.

Keefer, Philip, 2008, “Beyond Legal Origin and Checks and Balances: Political Credibility, Citizen Information, and Financial Sector Development,” in Political Institutions and Financial Development, ed. by Stephen Haber, Douglass North, and Barry Weingast (Stanford, California: Stanford University Press), pp. 125–55.

La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny, 1998, “Law and Finance,” Journal of Political Economy, Vol. 106, No. 6, pp. 1113–55.

McKinnon, Ronald I., 1973, Money and Capital in Economic Development (Washington: Brookings Institution).

Polity IV Project, available at www.systemicpeace.org/polity/polity4.htm

Quintyn, Marc, and Geneviève Verdier, 2010, “‘Mother, Can I Trust the Government?’ Sustained Financial Deepening—A Political Institutions View,” IMF Working Paper 10/210 (Washington: International Monetary Fund).

Shaw, Edward S., 1973, Financial Deepening in Economic Development (New York: Oxford University Press).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org